What is an Operating Budget, And How To Create One?

Operating Budget

An operating budget is a comprehensive financial plan that maps out a company’s projected revenues and expenses over a defined period — typically a fiscal year. It tells you exactly where money will come from, where it will go, and whether the business can sustain and grow its operations without running into a cash crisis.

Think of it as the financial backbone of day-to-day decision-making. Unlike a capital budget that funds long-term assets, the operating budget governs what happens inside your business every single month: payroll, rent, materials, marketing spend, and everything in between.

For business owners, CFOs, and financial managers, getting the operating budget right isn’t optional — it’s the difference between controlled growth and reactive firefighting.

Operating Budget vs. Capital Budget: Knowing the Difference

Before building one, it’s worth clarifying what an operating budget is not.

A capital budget plans for long-term investments — machinery, facilities, acquisitions, technology infrastructure. These are assets expected to generate value over multiple years.

An operating budget, by contrast, covers the short-term costs of running the business: the recurring, day-to-day expenditures that keep operations alive. The two are not substitutes — they serve fundamentally different purposes and should be built in parallel to give you a complete financial picture.

Many businesses also confuse an operating budget with a financial model. A financial model is typically more dynamic and multi-scenario in nature, used for investment decisions and long-term forecasting. The operating budget is the operational execution layer — grounded in the current fiscal year, tied to actual departments and cost centers, and reviewed monthly against real results.

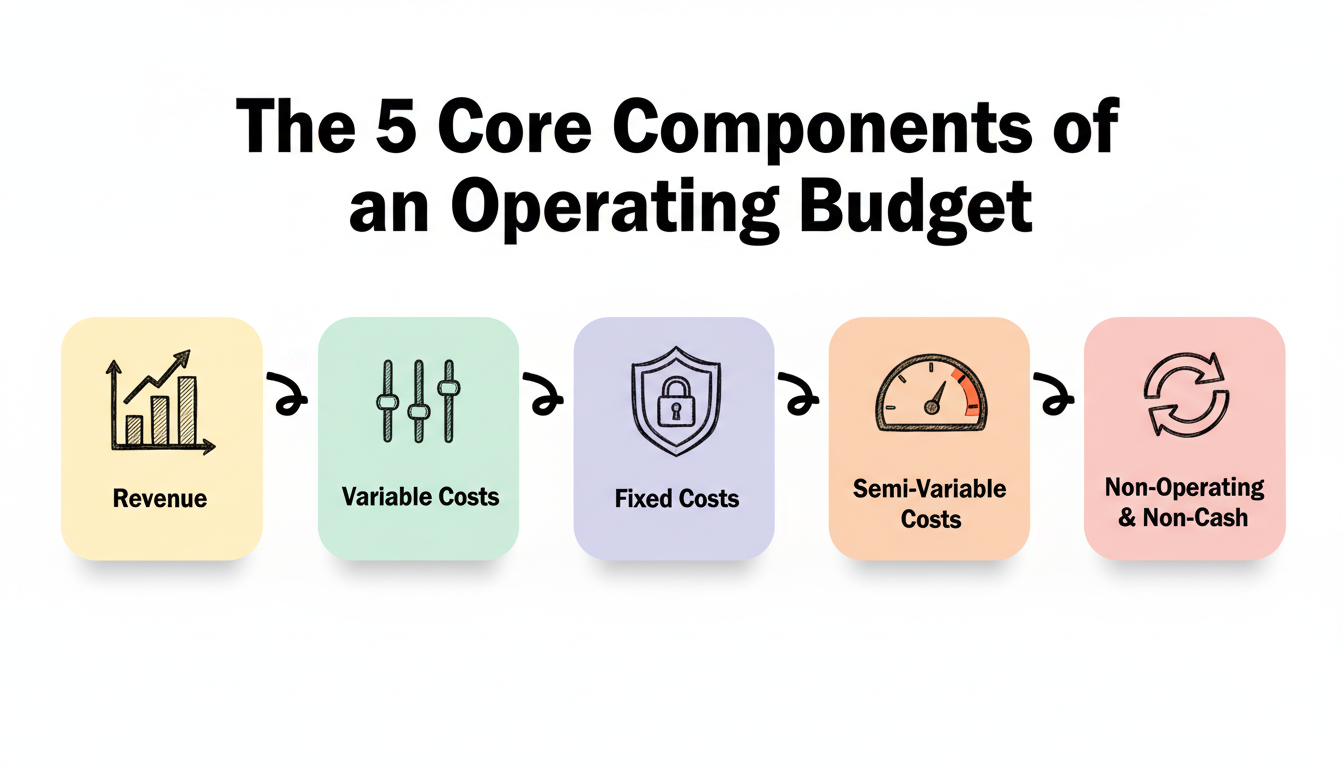

The Five Core Components of an Operating Budget

Every operating budget, regardless of industry or company size, is built from five foundational components. Mastering each one is essential before you can put together a reliable plan.

1. Revenue

Revenue is where the budget begins. Every other figure flows from your expected income. This isn’t just about writing down last year’s sales and adding a percentage. Solid revenue forecasting pulls from:

- Historical sales data broken down by product, service line, or geography

- Market conditions and industry growth trends

- Seasonal patterns and demand cycles

- Current pipeline and signed contracts

- Pricing changes or new product launches

The more granular the revenue breakdown, the more useful the budget becomes. A SaaS company should separate recurring subscription revenue from one-time implementation fees. A product business should separate units by SKU and region. Lumping everything together creates blind spots.

2. Variable Costs (Cost of Goods Sold and Direct Expenses)

Variable costs move in proportion to your output. When revenue goes up, these costs typically go up too. They include:

- Raw materials and direct supplies

- Manufacturing labor tied to production volume

- Sales commissions and merchant processing fees

- Shipping, packaging, and fulfillment costs

- Direct marketing spend tied to customer acquisition

Because variable costs fluctuate, they require regular monitoring against actual sales performance. A sharp revenue increase without planning for proportional variable cost growth is one of the most common cash flow surprises businesses face. Understanding cash vs. profit is critical here — strong revenue growth can mask an underlying squeeze on margins if variable costs aren’t tightly tracked.

3. Fixed Costs

Fixed costs are predictable and stable — they don’t change meaningfully based on what you produce or sell. They include:

- Office and facility rent

- Salaried employee compensation

- Insurance premiums

- Equipment lease payments

- Software subscriptions and SaaS tools

- Loan repayments and debt service

Fixed costs form the “floor” of your operating expenses. Your minimum projected revenue must cover these costs entirely, or the business is structurally loss-making before it generates a single sale. Understanding your fixed cost base is the first step in calculating your break-even point.

4. Semi-Variable Costs

Often overlooked, semi-variable costs contain both a fixed and variable component. Examples include:

- Utility bills (a base charge plus usage-based costs)

- Overtime pay (salary is fixed; overtime fluctuates with demand)

- Equipment maintenance (scheduled maintenance is fixed; repairs are variable)

- Customer support staffing (a core team is fixed; seasonal scaling is variable)

Proper bookkeeping and accounting practices help you correctly classify these costs so they’re neither overstated nor missed in your planning.

5. Non-Operating and Non-Cash Expenses

A complete operating budget also captures:

- Non-cash expenses such as depreciation and amortization — these reduce reported income but don’t affect cash outflow in the period

- Non-operating expenses such as interest payments on debt, corporate income taxes, and investment losses

Including these gives leadership and investors a more honest picture of financial performance. A budget that ignores depreciation, for example, overstates profitability in businesses with significant fixed assets.

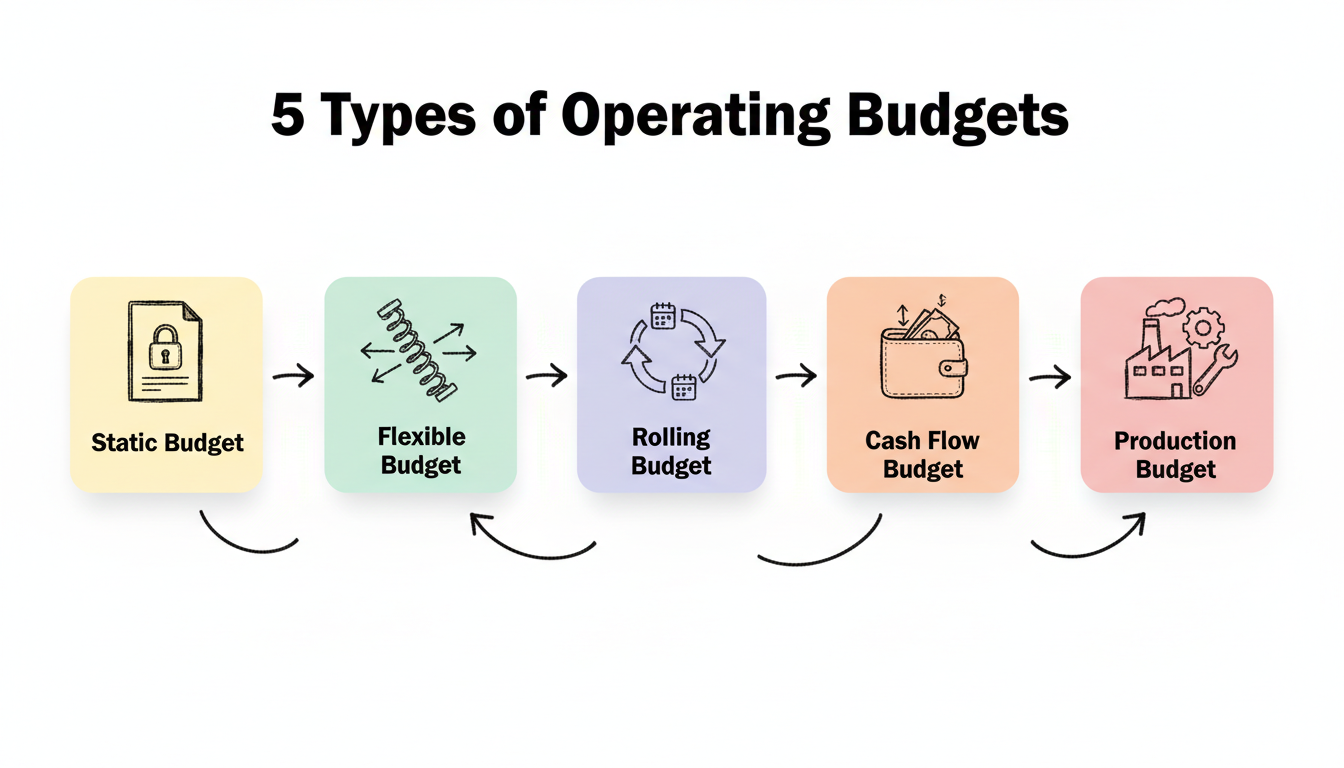

Types of Operating Budgets

Not every business builds its operating budget the same way. The right structure depends on how predictable your revenue is, how fast your environment changes, and what you need the budget to do.

Static Budget

A static budget is set at the start of the period and doesn’t change — regardless of what actually happens in the business. It’s the traditional approach and works well for companies with highly predictable, stable operations.

The downside is inflexibility. In a dynamic business environment, a static budget can quickly become irrelevant. Departments that over- or underperform are measured against figures that may no longer reflect reality.

Flexible Budget

A flexible budget adjusts based on actual activity levels. It builds in adjustment mechanisms so that if revenue comes in 20% above projection, the variable cost benchmarks automatically scale accordingly.

This approach is far more useful for performance evaluation. It separates the impact of volume variance from operational efficiency variance — two very different problems that a static budget would conflate.

Rolling Budget

A rolling (or continuous) budget is updated monthly or quarterly, always extending the budget horizon by one period as each period closes. Instead of a fixed annual budget that ages throughout the year, you always have a current forward-looking 12-month view.

Rolling budgets are increasingly standard practice among growth-stage companies and organizations with a strong fractional CFO guiding financial operations.

Cash Flow Budget

A cash flow budget zooms in specifically on the timing of cash inflows and outflows, independent of accrual-based revenue and expense recognition. It answers the critical question: “Will we have the cash to pay our bills next month?”

A business can be profitable on paper and still run out of cash. The cash flow budget prevents this by surfacing liquidity gaps before they become emergencies.

Production Budget

Specific to manufacturing businesses, a production budget translates sales targets into required production volumes and associated costs — materials, direct labor, and manufacturing overhead. It ensures production capacity aligns with demand forecasts and that inventory levels remain efficient.

A Real-World Operating Budget Example

The following simplified example illustrates how an operating budget comes together for a mid-sized professional services firm targeting $2M in annual revenue.

| Budget Category | Annual Projection |

| Revenue | |

| Consulting Services Revenue | $1,600,000 |

| Retainer Contracts | $320,000 |

| Training & Workshops | $80,000 |

| Total Revenue | $2,000,000 |

| Variable Costs | |

| Direct Consultant Labor (billable) | $480,000 |

| Subcontractor Fees | $120,000 |

| Travel & Client Expenses | $60,000 |

| Total Variable Costs | $660,000 |

| Gross Profit | $1,340,000 |

| Fixed Operating Expenses | |

| Office Rent & Utilities | $96,000 |

| Salaried Staff (non-billable) | $340,000 |

| Software & Tools | $42,000 |

| Marketing & Business Development | $80,000 |

| Insurance | $18,000 |

| Total Fixed Costs | $576,000 |

| Non-Cash Expenses | |

| Depreciation | $24,000 |

| Non-Operating Expenses | |

| Loan Interest | $16,000 |

| Corporate Taxes (estimated) | $112,000 |

| Total All Expenses | $1,388,000 |

| Net Operating Income | $612,000 |

This structure gives leadership a clear line of sight from top-line revenue to bottom-line operating income — and a benchmark against which every month’s actual results can be measured.

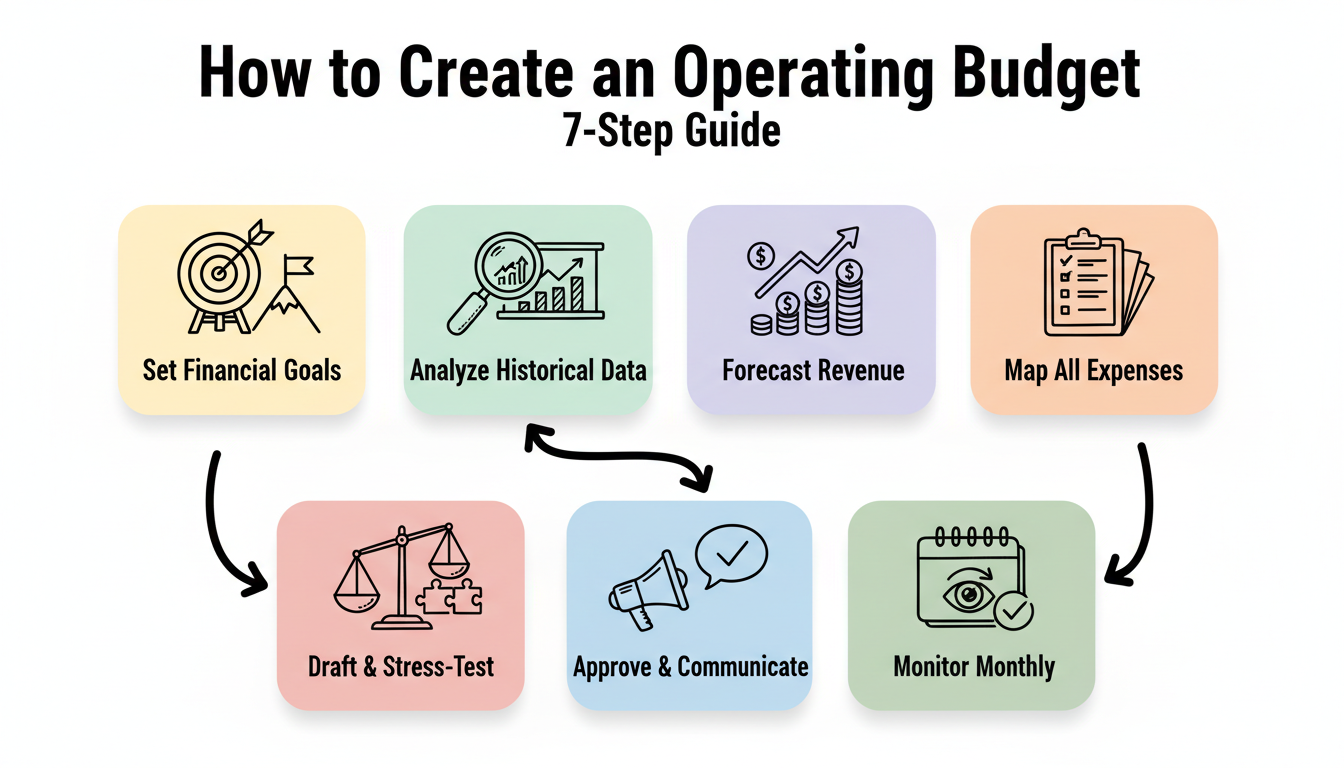

How to Create an Operating Budget: A Step-by-Step Guide

Step 1: Define Your Financial Goals for the Period

An operating budget without clear objectives is just a spreadsheet. Before crunching numbers, define what the business needs to achieve: a target profit margin, a revenue growth rate, a cost reduction percentage, or a specific net income figure.

These goals should align with the broader financial model and strategic plan. If the company is targeting a fundraising round, investor covenants may set minimum cash reserves or EBITDA thresholds that must be reflected in the budget.

Goals also force prioritization. When departments submit expense requests, leadership can evaluate them against stated objectives rather than approving costs in isolation.

Step 2: Gather and Analyze Historical Financial Data

Pull together at least two to three years of income statements, cash flow statements, and expense reports. Look for:

- Revenue trends by product or service line

- Seasonal patterns in both revenue and costs

- One-time items that should not be projected forward

- Expense categories that have drifted upward without clear justification

- Any significant variance between prior budgets and actual results

This historical analysis is not just data collection — it’s diagnostic. It tells you where your previous budgets were accurate and where they consistently missed. Building on flawed assumptions produces a flawed budget.

Step 3: Forecast Revenue — Conservatively and by Segment

Revenue is always the hardest line to get right. The temptation is to be optimistic; the discipline is to be realistic.

Build revenue projections from the bottom up where possible — by product, geography, customer segment, or sales rep — rather than applying a blanket growth percentage to last year’s total. Validate top-down assumptions against bottom-up projections.

Run multiple scenarios: a base case, a conservative downside, and an upside. Understanding the budget under different revenue outcomes prepares the business for volatility and avoids the trap of planning only for the best case.

Step 4: Map and Categorize All Expenses

List every expense the business expects to incur, organized by category: fixed, variable, semi-variable, non-cash, and non-operating. Involve department heads. Finance rarely has full visibility into operational costs without input from the people running each function.

Key areas that are often underbudgeted:

- Technology and software renewals

- Recruitment and onboarding costs

- Training and professional development

- Legal and compliance fees

- Contingency and emergency reserves

Building a contingency line — typically 3–5% of total operating expenses — is not pessimism. It’s professional financial management. Unexpected costs are not exceptional events; they are certainties.

Step 5: Draft, Balance, and Stress-Test the Budget

Compile all inputs into a structured format with revenue at the top, followed by COGS, gross profit, operating expenses, and net income. A balanced budget does not require projected revenue to equal projected expenses — it requires that projected income is sufficient to achieve the stated financial goals.

Run sensitivity analyses: What happens to net income if revenue comes in 10% below forecast? What if a key supplier increases prices? What if you need to hire ahead of a new contract? Stress-testing surfaces fragility before it becomes a problem. This process overlaps with formal financial risk modeling and should be part of any serious budgeting exercise.

Step 6: Obtain Approval and Communicate the Budget

An operating budget that sits in a finance folder serves no one. Present the approved budget to department leaders, tie it to their performance objectives, and make it part of ongoing management conversations.

The clearest budgets define ownership by cost center. Each manager knows which line items they’re responsible for and is measured against them. This accountability structure is what transforms a budget from a document into a management tool.

Step 7: Monitor, Track, and Adjust Monthly

The budget cycle doesn’t end when the document is approved. Monthly budget-versus-actual (BvA) reviews are essential to identify variances early and course-correct before small misses compound into large problems.

Track key performance indicators alongside financial metrics — not just whether revenue hit target, but whether the leading indicators (pipeline value, conversion rates, customer retention) are tracking in the right direction. Use this monitoring cadence to update rolling forecasts and flag any structural changes to the budget for leadership review.

Common Mistakes That Undermine Operating Budgets

Using last year’s numbers as a default. Zero-based budgeting — where every expense must be justified from scratch each cycle — is more rigorous than simply rolling forward prior year figures. Even if you don’t go fully zero-based, challenge every major line item rather than accepting inertia.

Budgeting revenue too optimistically. Overconfident revenue projections create a cascade of problems: overstaffing, overinvestment in growth, and a budget that provides false comfort until actual results arrive.

Ignoring cash timing. Accrual-based revenue and profit don’t tell you when cash will arrive. A business can post strong profits in Q1 but face a cash crisis in Q3 if collections are slow. Always pair the operating budget with a cash flow projection.

Building the budget in a silo. Finance-only budgets miss critical operational context. The best budgets are built collaboratively, with sales, operations, HR, and marketing all contributing their forward-looking plans.

Treating the budget as fixed. Market conditions change. Key hires join or leave. A major customer churns. Budgets must be living documents, reviewed and adjusted as reality evolves — not filed away after January and revisited at year end.

Best Practices for Effective Operating Budgets

Involve stakeholders early. Department heads who contribute to the budget are more likely to manage their costs against it. Buy-in at the planning stage reduces friction during review conversations.

Build scenario layers. Every operating budget should have at minimum a base case and a downside scenario. Organizations with a strong financial planning function build three or more scenarios, each with a defined set of assumptions and corresponding response actions.

Align the budget to strategy. If the company is investing in market expansion this year, the budget should reflect that — even if it temporarily compresses margins. A budget that contradicts the strategic plan creates organizational confusion.

Use purpose-built tools. Spreadsheets work at small scale, but they break down quickly as businesses grow. Finance platforms that integrate with your accounting system provide real-time BvA tracking and reduce manual errors. If your team lacks the bandwidth to implement this, professional financial services can close the gap.

Review operating expenses for efficiency annually. Not every fixed cost is truly necessary. An annual vendor review, software audit, and headcount assessment often surface meaningful savings that would otherwise persist indefinitely.

Frequently Asked Questions

What is the difference between an operating budget and a master budget?

The master budget is the complete set of all budgets for an organization, including the operating budget, capital budget, and financial statements (income statement, balance sheet, and cash flow statement). The operating budget is a component of the master budget, specifically covering revenues and day-to-day operating expenses.

Can a small business benefit from an operating budget?

Absolutely — in fact, small businesses often benefit more than large enterprises because they have less financial buffer to absorb errors. A simple operating budget clarifies the revenue needed to cover fixed costs, highlights where variable costs are eating into margins, and forces realistic planning rather than optimistic guesswork.

What is the difference between an operating budget and a cash flow budget?

An operating budget forecasts revenues and expenses on an accrual basis — it shows whether the business is profitable. A cash flow budget tracks the timing of actual cash inflows and outflows. A business can be profitable but cash-poor if collections are slow or significant payments cluster in specific months. Both are necessary.

Who is responsible for preparing the operating budget?

Typically, the CFO or Head of Finance leads the process, with department managers contributing cost and revenue inputs for their areas. In smaller businesses without a full-time CFO, a fractional CFO can own the budget process, ensuring professional rigor without the overhead of a full-time hire.

What is an ideal operating profit margin to target in a budget?

It depends heavily on industry. Professional services firms often target 20–40% operating margins. SaaS businesses at scale typically aim for 20–30%. Retail and manufacturing businesses may operate with 5–15% margins. The right target for your budget is one that sustains operations, funds growth, and delivers adequate returns for equity holders.

Conclusion

An operating budget is not a bureaucratic exercise — it’s one of the most powerful management tools a business has. Done well, it connects financial objectives to operational decisions, gives every team a clear cost framework, and creates the accountability structures that separate disciplined businesses from those constantly reacting to financial surprises.

The key is building it correctly from the start: bottom-up revenue forecasting, rigorous expense categorization, scenario testing, and monthly review discipline. A budget that gets reviewed once a year and forgotten in between is not a budget — it’s a wish list.

For businesses that want to establish professional-grade financial planning without the cost of a full internal team, Oak Business Consultant’s financial modeling and CFO advisory services provide the expertise to build, monitor, and optimize operating budgets that reflect where your business is actually going — not just where it’s been. Contact us now for a free consultation.

{kind=link}