How to Finance Business Expansion?

Best Ways to Finance Your Business Growth

Most business owners reach a point where staying the same starts to feel risky. Your customers want more. Your team has outgrown its space. A competitor is moving into your territory. Growth is calling, and you know it.

But growth costs money. Figuring out how to finance business expansion is one of the most important decisions a founder or CEO will ever make. Get it right, and you unlock years of compounded momentum. Get it wrong, and even a great business can end up in serious trouble.

This guide walks you through everything you need to know, from understanding your readiness to choosing the right funding source to managing the money once it arrives.

Are You Actually Ready to Expand?

Before you think about financing, you need to be honest with yourself about where your business stands today. Expansion amplifies what already exists. If your operations, people, or finances are shaky, adding capital will not fix them. It will make the problems bigger and faster.

Here are the signs that suggest you are genuinely ready:

Your revenue has grown consistently for at least two or three years. Not just one good quarter, but a real, repeatable trend. Your cash flow is positive and predictable. You are not barely covering payroll month to month. You have more demand than you can comfortably serve. Customers are waiting, or you are turning work away. Your team has the capacity and leadership to manage a larger operation. You have a specific, costed plan for what expansion will look like.

If you can check most of those boxes, you are in a strong position. If several of them feel uncertain, the work to do right now is internal, not external.

Why the “How” of Financing Matters More Than You Think

Many business owners approach financing like a transaction. They need money, they find money, done. But the structure of your financing shapes your business for years. The terms, the repayment obligations, the equity you give up or keep, the covenants attached to a loan, all of these things influence your freedom to make decisions.

Knowing how to finance business expansion properly means thinking beyond the immediate cash. It means asking what this financing will cost you at year three or year five. It means thinking about your relationship with lenders or investors, not just the amount they write. And it means building a plan you can actually execute, not one that sounds good in a pitch deck.

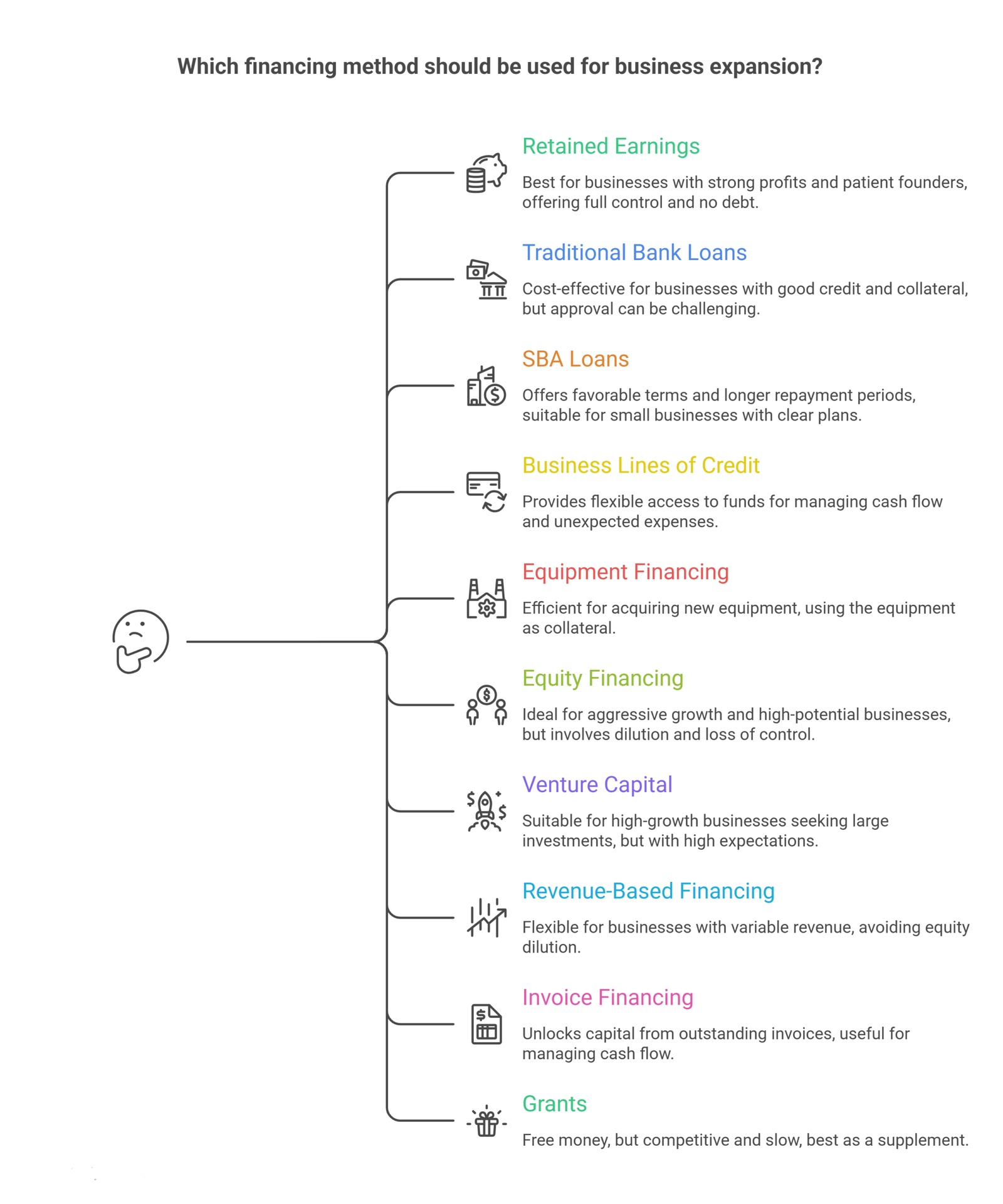

The Main Ways to Finance Business Expansion

There is no single right answer. The best approach depends on your business model, your financial position, the nature of your expansion, and what you are willing to trade for capital.

Retained Earnings and Internal Cash Flow

The cleanest way to fund growth is with your own money. If your business generates strong profits, reinvesting those earnings into expansion keeps you in full control and avoids debt. You move at your own pace. You owe nothing to outside parties.

The downside is speed. Self-funded expansion is slower, and in competitive markets, slow can be costly. It also requires real financial discipline to build up reserves over time rather than distributing profits or spending on non-essentials.

This approach works best for businesses with solid margins, patient founders, and expansions that do not need to happen immediately.

Traditional Bank Loans

A term loan from a bank is one of the most straightforward ways to finance business expansion. You borrow a fixed amount, repay it over a set period with interest, and the bank has no stake in your business.

Banks typically offer lower interest rates than alternative lenders. For businesses with strong credit, solid financials, and real assets to offer as collateral, a bank loan is often the most cost-effective choice.

The challenges are the approval process and the criteria. Banks want to see several years of financial history, healthy revenue, good credit scores, and often significant collateral. If your business is younger or has had some rough patches, approval can be difficult.

Prepare your financial statements, tax returns, a well-written business plan, and clear projections before you apply. A disorganized application wastes time and reduces your credibility with the lender.

SBA Loans

SBA loans, backed by the U.S. Small Business Administration, sit between traditional bank loans and alternative financing. Because the SBA guarantees a portion of the loan, lenders take on less risk and can offer more favorable terms to small businesses.

The SBA 7(a) loan is the most commonly used. It works well for general business expansion, purchasing equipment, hiring staff, or opening new locations. SBA 504 loans are designed for major fixed assets like property or large machinery.

Repayment terms are often longer than standard bank loans, which reduces monthly payments and frees up cash flow. Interest rates are competitive. The tradeoff is a more involved application process and stricter eligibility requirements around business size, financial health, and how the funds will be used.

If you have time to prepare a strong application and your expansion plan is clear, an SBA loan is worth serious consideration for most small businesses.

Business Lines of Credit

A line of credit gives you flexible, revolving access to funds up to a set limit. You draw what you need, repay it, and draw again. You only pay interest on what you actually use.

This is not typically the right tool for large capital investments like buying a building or acquiring a company. But for managing cash flow during a growth phase, funding short-term inventory builds, covering hiring costs before new revenue materializes, or handling unexpected expenses during an expansion, a line of credit is extremely useful.

Many businesses use a line of credit alongside a term loan when they finance business expansion. The loan covers the large, planned costs. The credit line handles the day-to-day variability.

Equipment Financing

If your expansion requires new machinery, vehicles, technology, or other equipment, equipment financing is often the most efficient route. The equipment itself serves as collateral, which makes approval easier and rates more favorable.

You preserve your working capital and your other credit facilities. The loan is structured around the useful life of the equipment, which makes the math predictable. For manufacturing companies, medical practices, logistics businesses, and many others, this is one of the most practical ways to finance a specific type of business expansion.

Equity Financing and Outside Investors

Equity financing means bringing in capital in exchange for ownership in your business. This can take the form of angel investors, venture capital firms, private equity, or strategic partners.

The obvious advantage is that you receive capital without taking on debt. There are no monthly repayments. If the business struggles, you do not face a lender demanding payment.

The real cost, however, is dilution and influence. Investors get a seat at the table, to varying degrees. You may lose some control over strategic decisions. You will be expected to deliver returns, and the timeline for those returns will be shaped by what your investors want, not just what you want.

Equity financing makes the most sense for businesses pursuing aggressive growth, entering new markets quickly, or building something with a large potential exit. It is less ideal for businesses that want to grow steadily and stay independent.

Venture Capital

Venture capital is a subset of equity financing aimed specifically at high-growth businesses. VC firms invest large sums in exchange for significant equity stakes and usually have strong opinions about strategy, hiring, and the path to scale.

This is not the right fit for most traditional businesses. VC-backed companies are typically expected to grow very fast and eventually exit through an acquisition or IPO. If that matches your vision, VC can be transformative. If you want to build a lasting, owner-operated business, VC is likely to create friction rather than freedom.

Revenue-Based Financing

Revenue-based financing is a newer model where investors provide capital in exchange for a percentage of your future revenue until a set repayment cap is reached. There is no fixed monthly payment. When revenue is strong, you pay more. When it dips, you pay less.

This can be a good fit for businesses with consistent but somewhat variable revenue, like SaaS companies or e-commerce brands. It avoids equity dilution and has more flexibility than a fixed loan. The cost of capital is often higher than a bank loan, but the terms can feel more manageable for certain businesses.

Invoice Financing and Factoring

If your business sells to other businesses on credit terms, you may have a lot of capital tied up in outstanding invoices. Invoice financing lets you borrow against those receivables. Factoring lets you sell them outright to a third party at a discount in exchange for immediate cash.

These tools do not replace a comprehensive strategy for how to finance business expansion, but they can be a valuable bridge. If slow-paying clients are strangling your cash flow during a growth phase, invoice financing can unlock the capital you have already earned.

Grants and Government Programs

Grants are free money. There is no repayment, no equity, no interest. But they are also competitive, restrictive, and slow.

Government grants often target specific sectors, geographic regions, or business characteristics. If your expansion aligns with an economic development priority, a sustainability initiative, or a specific industry focus, it is worth researching what might be available. The application process is typically time-consuming and the award is not guaranteed.

Grants work best as a supplement to other financing, not as the primary strategy. If you find one that fits, apply. But do not build your expansion timeline around a grant you have not yet received.

How to Choose the Right Financing Structure

Matching your financing to your expansion type is essential. Here is a simple way to think about it:

If your expansion is a long-term investment, like a new facility or an acquisition, a long-term loan with a fixed repayment schedule makes sense. The cost of the project should generate returns over years, and the loan should mirror that timeline.

If your expansion requires operational cash, like hiring, inventory, or marketing, shorter-term tools like a line of credit or revenue-based financing might be more appropriate.

If your expansion is aggressive and fast, and you need a major capital partner, equity or venture financing may be the right path, assuming you are comfortable with the tradeoffs.

When thinking about how to finance business expansion, it is also worth considering a blended approach. Many businesses use a term loan for capital expenditures, a credit line for working capital, and retained earnings to cover softer costs like training and onboarding. This layered structure can reduce overall risk and provide flexibility.

What Lenders and Investors Actually Want to See

Whether you are talking to a bank, an SBA lender, or a private investor, they all want to see essentially the same things, expressed in different ways.

They want to know that your business is financially healthy today. That means clean books, organized financial statements, and a clear picture of revenue, expenses, and profitability.

They want to know that you have a credible plan. Not a vague aspiration, but a specific, costed plan that shows where the money goes, how the expansion generates returns, and what the timeline looks like.

They want to know that you can service the debt or deliver returns. That means cash flow projections that are realistic and supported by evidence.

And they want to know that you and your team are capable of executing. Management quality matters a great deal. Lenders and investors back people as much as they back businesses.

Spending time building these materials before you approach any financing source is not just helpful. It is essential.

Mistakes to Avoid When Financing Business Expansion

The most common mistake is underfunding. Business owners estimate their expansion costs, then discover they underestimated by thirty or forty percent. Unexpected costs, delays, and ramp-up time are almost inevitable. Build in a buffer of at least fifteen to twenty percent above your projected needs.

Another common mistake is taking on too much debt too fast. The monthly repayment obligations can squeeze cash flow, especially during the ramp-up period when new revenue has not yet fully materialized. Model your cash flow carefully under different scenarios before committing.

Many business owners also make the mistake of mixing financing types incorrectly. Using short-term credit to fund long-term capital investments creates a mismatch that becomes painful quickly. Match the duration of your financing to the nature of the investment.

Finally, some business owners approach financing reactively, when they are already in trouble or in a rush. The best time to arrange credit and explore financing options is when you do not desperately need it. Lenders can smell urgency, and it weakens your position.

The Role of Financial Leadership in Business Expansion

One thing most competitor articles on how to finance business expansion overlook is this: the financing decision is only as good as the financial leadership behind it.

Many growing businesses lack a full-time CFO. They have an accountant who keeps the books and maybe a bookkeeper who handles day-to-day entries. But they do not have someone who is actively thinking about capital structure, financial risk, cash flow modeling, and lender relationships.

This gap is costly. Without strong financial leadership, businesses make reactive decisions instead of strategic ones. They miss opportunities, overpay for capital, or take on financing structures that create problems three years later.

A fractional CFO or a dedicated financial advisory partner brings that strategic perspective without the cost of a full-time executive. They help you build your financial story, identify the right financing sources, prepare the materials lenders want to see, and manage the process from start to finish.

Building Your Expansion Financial Plan

Before you approach any lender or investor, you should have a clear financial plan in place. This is not just a pitch deck or a summary. It is a working document that includes:

A detailed cost breakdown for the expansion, including capital expenditures, working capital needs, and a contingency buffer.

Revenue projections that show how the expansion is expected to generate returns, including realistic timelines for when new revenue will begin.

Cash flow projections covering at least twenty-four months, showing how you will service any new debt obligations while maintaining operations.

A clear explanation of how the financing fits into your overall capital structure, including existing debt, equity, and available reserves.

Sensitivity analysis showing how the plan holds up under more conservative assumptions, not just the best-case scenario.

With this plan in hand, you are not just asking for money. You are presenting a case. That changes the dynamic of every conversation.

Frequently Asked Questions

What is the most common way to finance business expansion?

For most small and mid-sized businesses, term loans and SBA loans are the most common methods. They provide a lump sum at a fixed rate and repayment schedule, which makes planning straightforward. Lines of credit are also widely used to manage cash flow during growth phases.

How much should I borrow to expand my business?

Borrow based on your detailed cost plan, not on what you think you can get approved for. Calculate your total expansion costs, add a fifteen to twenty percent buffer, and model whether your expected cash flow can comfortably cover the repayments. Overborrowing creates pressure; underborrowing creates delays and the need to return to lenders mid-project.

Does expansion financing hurt my credit?

Applying for business credit typically results in a hard inquiry, which can temporarily affect your credit score. Carrying additional debt will affect your debt-to-income ratios. However, if you service the debt responsibly, expansion financing can actually strengthen your credit profile over time.

What financials do I need to apply for a business loan?

Most lenders will ask for two to three years of business tax returns, profit and loss statements, balance sheets, bank statements, and cash flow projections. Having these organized and accurate before you apply speeds up the process significantly.

Should I use equity or debt to finance business expansion?

It depends on your goals. Debt keeps you in control but creates repayment obligations. Equity brings a partner and capital without repayment pressure, but you give up ownership and some influence. Most businesses that want to stay independent and grow sustainably prefer debt-based financing where possible.

Can I finance business expansion with a line of credit?

A line of credit can help cover short-term operational costs during an expansion, like hiring or inventory. But it is not the right tool for large capital investments. Lines of credit are revolving and typically carry higher rates than term loans. Use them for flexibility, not for the core funding of a major expansion.

How long does it take to get approved for expansion financing?

It varies widely. Alternative online lenders can approve and fund within days. Traditional bank loans may take four to eight weeks. SBA loans often take eight to twelve weeks or more. Plan your timeline accordingly and start the process earlier than you think you need to.

What if my business has bad credit?

Bad credit limits your options but does not eliminate them. Alternative lenders, revenue-based financing, and equipment financing can all work with weaker credit profiles, typically at higher rates. Building your credit profile before you need to expand is the better long-term strategy.

How do I know if my business is ready for expansion?

Consistent revenue growth, positive and predictable cash flow, more demand than you can serve, and a specific plan for what expansion will look like are all strong signals. If you are uncertain, working with a financial advisor to assess your readiness is a smart step before committing to anything.

Conclusion

Understanding how to finance business expansion is one thing. Executing it with the right structure, the right lenders, and the right financial oversight is another.

At Oak Business Consultant, our CFO services are designed specifically for growing businesses that need strategic financial leadership without the overhead of a full-time executive. We help founders and CEOs build sound financial plans, identify the most appropriate financing sources, and manage the numbers through every phase of expansion.

If you are thinking seriously about growth and want a financial partner who can help you get there the right way, we would love to talk. Reach out now to learn more about our CFO services and how we work with businesses at every stage of expansion.