What is a Chart of Accounts in Bookkeeping for Entertainment Industry?

Chart of Accounts in Bookkeeping for the Entertainment Industry

Accountants have carved out a highly lucrative niche in the multibillion-dollar entertainment industry, providing financial services to Hollywood studios, streaming platforms, independent production companies, and a wide spectrum of talent, from chart-topping musicians to sound engineers and B-movie extras.

Unlike most industries, entertainment accounting carries a unique complexity: projects are long-cycle, revenue streams are multi-layered (box office, streaming royalties, merchandise, licensing), and cost structures often span years. A well-organized Chart of Accounts (COA) is the financial backbone that keeps it all in order.

This guide walks you through the purpose, structure, and practical application of a COA tailored specifically for entertainment businesses.

The Entertainment Industry at a Glance

The global entertainment and media (E&M) industry is one of the largest and fastest-growing economic sectors in the world.

| Metric | Figure |

| Global E&M Revenue (2024) | ~$2.9 trillion (PwC) |

| Projected Global E&M Revenue (2029) | $3.5 trillion (PwC) |

| U.S. Share of Global Market | ~33% |

| U.S. M&E Market Value (2024) | $649 billion |

| U.S. Projected Growth to 2028 | $808 billion at 4.3% CAGR |

| Global Video Games Revenue (2024) | $224 billion |

| Global Cinema Revenue (2024) | $33 billion |

| Global OTT Video Revenue (2024) | $316+ billion |

| Digital Share of Ad Revenue (2024) | 72% |

The industry is growing at a compound annual growth rate (CAGR) of 3.7% — outpacing projected global economic growth. Key growth engines include streaming platforms, digital advertising, live events, and an increasingly dominant gaming sector.

The entertainment industry itself covers a wide range of verticals:

- Film — Major studios, independent productions, streaming originals

- Music — Recorded music, live performances, digital distribution

- Gaming — Console, mobile, PC, esports (revenues exceeding movies and music combined)

- Publishing — Books, digital media, newspapers, magazines

- Broadcast & Streaming — Television, OTT platforms, podcasts

- Live Events — Concerts, theatre, sporting events

Notable stat: The global video games market at $224 billion in 2024 now exceeds the combined revenues of the global film and music industries. Esports and in-game advertising are accelerating this growth further.

What Is a Chart of Accounts?

A Chart of Accounts (COA) is a structured index of every financial account used in a company’s accounting system. It categorizes all transactions, from a bank loan to a catering invoice on a film set into clearly defined accounts, making financial reporting, tax filing, and budgeting significantly easier.

Think of it as the master filing system for your company’s financial life. Every dollar that flows in or out must be assigned to an account in the COA.

The five primary account categories are:

- Assets — What your company owns

- Liabilities — What your company owes

- Equity — The residual interest (assets minus liabilities)

- Revenue — Income generated from operations

- Expenses — Costs incurred to generate revenue

A COA is not one-size-fits-all. An indie film studio and a major music label will have very different COA structures, even if the foundational categories are the same.

Why the Entertainment Industry Needs a Specialized COA

Unlike a retail business or a law firm, entertainment companies deal with:

- Long and irregular revenue cycles — A film may take 3 years to produce and generate royalties for 20 more

- Deferred revenue — Advance licensing payments or streaming deals paid upfront but earned over time

- Residuals and royalties — Ongoing payments to talent, unions, and rights holders

- Multi-entity structures — Single-purpose LLCs formed per project (very common in film)

- International transactions — Foreign distribution, currency gains/losses

- Intellectual property (IP) amortization — Copyrights, film negatives, and master recordings treated as long-term assets

These factors make a thoughtfully designed COA essential, not optional.

The Two-Tier Accounting Structure

One of the most distinctive features of entertainment industry bookkeeping is its two-tier accounting model, which separates general business operations from project-specific production costs.

Tier 1: Outside Accounting (General Operations)

This covers the company’s regular day-to-day operating costs — the kind you’d find in any business:

- Office rent and utilities

- Administrative salaries

- Marketing and PR

- Legal and accounting fees

- Equipment leases

Tier 2: Inside Accounting (Production Budget)

This tracks all costs directly tied to the production itself:

- Cast and crew wages

- Location fees

- Set construction and props

- Equipment rental (cameras, lighting, sound)

- Post-production (editing, VFX, color grading, sound mixing)

Why does this distinction matter? The two tiers must remain strictly separate. Mixing production costs with operating costs distorts your true production budget and can create legal exposure, a problem famously illustrated in the Buchwald v. Paramount case over the film Coming to America, where the blurring of costs led to a landmark Hollywood accounting lawsuit.

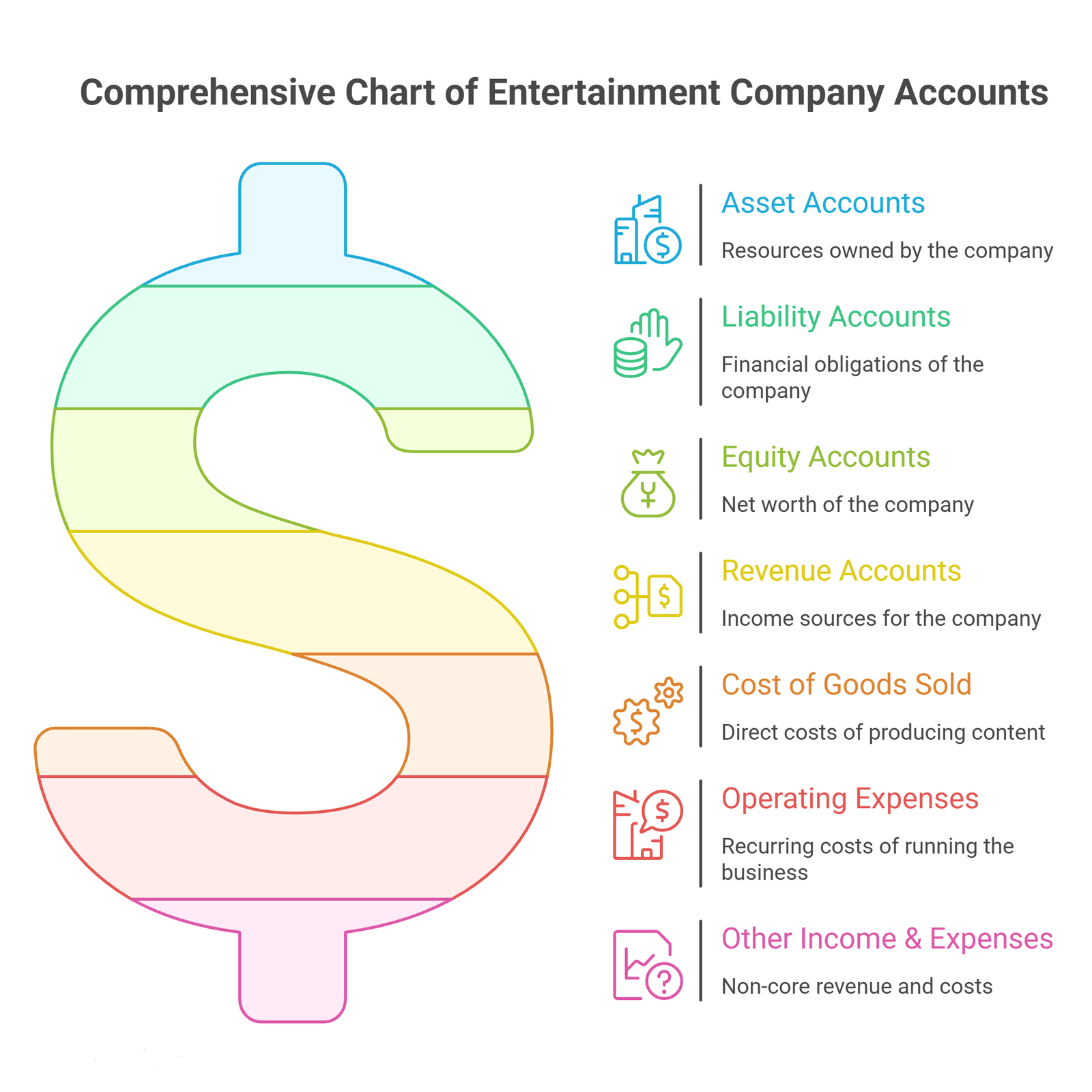

COA Structure & Account Number Ranges

Account numbers are used to uniquely identify each account and group related accounts together. The following ranges are widely used in entertainment company bookkeeping:

| Range | Category |

| 1000–1999 | Assets |

| 2000–2999 | Liabilities |

| 3000–3999 | Equity |

| 4000–4999 | Revenue / Income |

| 5000–5999 | Cost of Goods Sold (COGS) |

| 6000–6999 | Operating Expenses |

| 7000–7999 | Payroll Expenses |

| 8000–8999 | Other Income |

| 9000–9999 | Other Expenses |

Note: These ranges are conventions, not legal requirements. Your accountant may adjust them based on your company structure, the accounting software you use (QuickBooks, Sage, NetSuite), or industry-specific regulatory requirements.

Account Types Explained

1. Asset Accounts

Assets are everything of economic value that your entertainment company owns or controls. They are divided into current (short-term) and fixed (long-term) assets.

Current Assets:

- Cash and cash equivalents

- Accounts receivable (e.g., unpaid distribution invoices)

- Petty cash

- Prepaid expenses (insurance, location deposits)

- Inventory (physical media, merchandise)

- Allowance for doubtful accounts

Fixed Assets:

- Production equipment (cameras, rigs, lighting kits)

- Studio buildings and improvements

- Vehicles (production trucks, location vans)

- Film negatives and master recordings (capitalized IP)

- Accumulated depreciation

2. Liability Accounts

Liabilities are financial obligations the company must settle, either within the current year (current) or over a longer term (long-term).

Current Liabilities:

- Accounts payable (vendor invoices due)

- Payroll taxes payable

- Union and guild dues payable (SAG-AFTRA, IATSE, WGA)

- Deferred revenue (advance licensing payments)

- Short-term loans

Long-Term Liabilities:

- Production financing loans

- Equipment financing

- Mortgage on studio property

- Bond obligations

3. Equity Accounts

Equity represents the net worth of the business — what remains after subtracting liabilities from assets. The structure of your equity accounts depends on your IRS classification (sole proprietor, partnership, LLC, or corporation).

Common equity accounts include:

- Paid-in capital

- Retained earnings

- Owner’s draws or distributions

- Filmmaker/shareholder equity

- Additional contributed capital

4. Revenue Accounts

Revenue in entertainment is rarely a single stream. A comprehensive COA should track each income source separately for meaningful analysis:

- Theatrical box office receipts

- Streaming and OTT licensing fees

- Home video / digital download sales

- Broadcast licensing (TV rights)

- International distribution rights

- Music synchronization fees

- Merchandise and branding revenue

- Sponsorship and brand integration income

- Grant and subsidy income (common for independent and documentary filmmakers)

5. Cost of Goods Sold (COGS)

COGS in entertainment represents the direct costs of creating the product being sold or distributed.

Formula:

COGS = Beginning Inventory + Purchases During Period − Ending Inventory

For a film production company, COGS typically includes:

- Principal cast fees

- Supporting cast and extras

- Crew wages (directors, cinematographers, grips, gaffers)

- Location acquisition and permits

- Set design, construction, and dressing

- Costume and wardrobe

- Equipment rental

- Raw stock and digital storage

- Catering and transportation (production-specific)

- Visual effects (VFX) and post-production labor

Advertising, distribution, and PR costs are not included in COGS — they are classified as operating expenses.

6. Operating Expenses

These are the recurring costs of running the business that fall outside the production budget (Tier 1 / Outside Accounting):

- Administrative salaries

- Office rent and utilities

- Software subscriptions (accounting, editing, project management)

- Equipment depreciation

- Legal and professional fees

- Insurance (general liability, E&O, production insurance)

- Marketing and advertising

- Travel and entertainment (non-production)

- Repairs and maintenance

7. Other Income & Expenses

Moreover, other Income refers to revenue that doesn’t come from your core operations:

- Interest earned on bank accounts or investments

- Gains from foreign currency exchanges on international screenings

- Insurance claim proceeds

- Profit from asset sales (sold equipment, IP rights)

- Tax incentive and rebate income

Other Expenses:

- Interest expense on loans

- Legal settlements or damages

- Fraud losses

- Penalties and fines

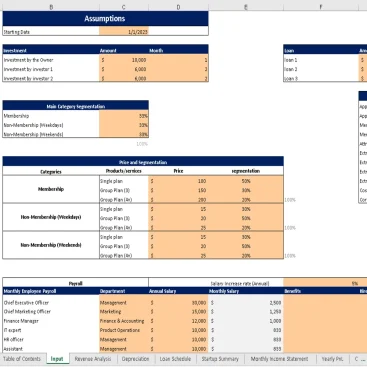

Sample COA for an Indie Production Company

Below is a simplified but realistic COA for a small to mid-size independent film production company:

ASSETS

1010 Checking Account

1020 Savings / Reserve Account

1030 Petty Cash

1100 Accounts Receivable

1200 Prepaid Insurance

1300 Production Equipment (at cost)

1310 Accumulated Depreciation – Equipment

1400 Film Negative / Master Recording (IP Asset)

1410 Accumulated Amortization – IP

LIABILITIES

2010 Accounts Payable

2020 Payroll Taxes Payable

2030 Guild and Union Dues Payable

2040 Deferred Revenue (Advance Licensing)

2100 Production Loan Payable

2200 Long-Term Equipment Financing

EQUITY

3010 Owner’s Equity / Paid-In Capital

3020 Retained Earnings

3030 Owner’s Draw / Distributions

REVENUE

4010 Domestic Theatrical Revenue

4020 OTT / Streaming Licensing Fees

4030 International Distribution Revenue

4040 Home Video & Digital Sales

4050 Broadcast Licensing

4060 Sync Licensing (Music)

4070 Merchandise Revenue

4080 Grants and Subsidies

COST OF GOODS SOLD (Production Budget)

5010 Principal Cast Fees

5020 Supporting Cast / Extras

5030 Director and Key Crew Fees

5040 Location and Permits

5050 Set Design and Construction

5060 Costume and Wardrobe

5070 Equipment Rental

5080 Visual Effects (VFX)

5090 Post-Production (Editing, Sound, Color)

5100 Catering and Craft Services (Production)

OPERATING EXPENSES

6010 Administrative Salaries

6020 Office Rent

6030 Utilities

6040 Legal and Accounting Fees

6050 Marketing and Advertising

6060 Insurance – General Liability

6070 Insurance – E&O (Errors & Omissions)

6080 Software and Technology

6090 Travel and Accommodation (Non-Production)

6100 Depreciation Expense

OTHER INCOME

8010 Bank Interest Income

8020 Foreign Exchange Gain

8030 Asset Sale Gain

8040 Insurance Proceeds

OTHER EXPENSES

9010 Loan Interest Expense

9020 Legal Settlements

9030 Foreign Exchange Loss

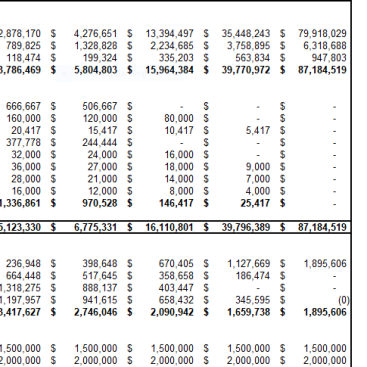

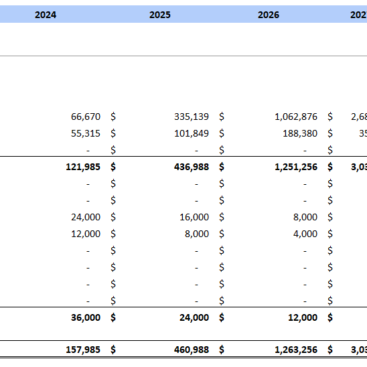

Below picture shows the charts of accounts of an entertainment company:

Income Prediction & Tax Considerations

The IRS requires entertainment companies to use the Income Forecast Method for depreciating certain intangible assets — including:

- Film and television productions

- Videotapes and sound recordings

- Copyrights and book patents

Under this method, the cost of a production is written off proportionally to the revenue it generates in each period. For example, if a film earns 15% of its lifetime projected revenue in Year 1, then 15% of its total production cost is deducted in that year.

Additional tax code provisions relevant to entertainment companies:

- Section 181 — Allows producers to deduct the first $15 million in qualified film, TV, or live theatrical production costs in the year they are incurred (up to $20 million in low-income/distressed communities)

- 15-Year Amortization — Creative property costs can be amortized over 15 years as an alternative treatment

- Bonus Depreciation — Certain production equipment may qualify for accelerated depreciation under TCJA provisions

- State Film Tax Credits — Many U.S. states (Georgia, New Mexico, New York) and international jurisdictions offer significant production incentives that must be correctly classified in the COA

Always consult a qualified entertainment CPA. Tax treatment of production costs is highly fact-specific, and improper classification can trigger audits or restatements.

Accounting Rules & GAAP Compliance

Entertainment companies must comply with accounting standards issued by several regulatory bodies:

- GAAP (Generally Accepted Accounting Principles) — The overarching framework for U.S. financial statements

- ASC 926 (FASB Accounting Standards Codification) — Specific guidance on accounting for entertainment companies, covering film cost capitalization and amortization

- AICPA Audit & Accounting Guide — Provides industry-specific guidance for entertainment entities

- IRS Revenue Procedures — Governs tax treatment of production costs and income recognition

Key accounting principles in practice:

- Accrual Accounting is standard — revenue and expenses are recorded when earned/incurred, not when cash is exchanged. This is critical for long-cycle productions.

- Double-Entry Bookkeeping — Every transaction has an equal and offsetting debit and credit. Production expenses are debited to the appropriate COGS account and credited to cash or accounts payable.

- Matching Principle — Costs should be recognized in the same period as the revenue they help generate.

- Conservatism — In cases of uncertainty (e.g., projected box office), recognize losses sooner and gains only when reasonably certain.

Operating Expense Ratio (OER):

A useful financial health metric for entertainment businesses is the Operating Expense Ratio:

OER = (COGS + Operating Expenses) ÷ Total Revenue

A lower OER indicates more efficient operations. Studios and production companies often benchmark this metric against peers to assess margin performance.

Frequently Asked Questions (FAQs)

Do indie filmmakers or small creators need a full COA?

Yes, but keep it simple. Even 20–30 accounts gives you clean separation between production costs, income, and expenses — making tax time and investor reporting far easier.

How is entertainment accounting different from other industries?

Two main things: a two-tier system (inside/outside production accounting) and unique assets like copyrights, film negatives, and master recordings that are amortized over time under ASC 926.

Accrual or cash-basis accounting — which should I use?

Accrual. It matches costs to the period revenue is earned, which is essential for long production cycles, deferred licensing income, and multi-year royalty streams.

Should each revenue stream have its own account?

Yes. Theatrical, streaming, licensing, merchandise, and broadcast should all be tracked separately. It tells you exactly which channel makes money and simplifies residual calculations.

What’s the difference between COGS and operating expenses in film?

COGS = costs tied directly to the production (cast, crew, locations, VFX). Operating expenses = costs of running the business (rent, admin salaries, marketing). Never mix the two.

Are film tax credits recorded as income?

Generally yes, as “Other Income” or a contra-expense, depending on your accountant’s approach and the jurisdiction. Always confirm treatment with a qualified entertainment CPA.

How often should a COA be updated?

Review it annually or at the start of each new project. New revenue streams (e.g., adding a podcast or merchandise line) or new tax rules may require new accounts.

What accounting software works best for entertainment companies?

QuickBooks (small/indie), Sage Intacct (mid-size studios), and Movie Magic Budgeting (production-specific) are the most widely used. Your COA structure should match the software’s account hierarchy.

Final Thoughts

A well-structured Chart of Accounts is not a bureaucratic formality — it is the financial infrastructure that determines whether an entertainment company can accurately track profitability, comply with complex tax and accounting rules, satisfy investors and lenders, and make informed creative and business decisions.

The global entertainment and media industry is on track to be a $3.5 trillion market by 2029, growing faster than the global economy. In an industry this large and this financially complex — where a single film can involve hundreds of vendors, multiple currencies, long-delayed revenue, and intricate royalty structures — the companies that manage their finances with precision will always have a competitive edge over those that don’t.

Whether you are an independent filmmaker bootstrapping your first feature or a mid-size production studio managing a slate of projects, investing in a properly designed COA — and the accounting talent to maintain it- is one of the highest-return decisions you can make.

{kind=link}