Holistic Financial Budget Definition, Its Types, and Uses

Introduction: Why a Financial Budget Is the Foundation of Business Success

Every business that survives long enough to scale has one thing in common: a disciplined approach to financial planning. A financial budget is not a bureaucratic formality. It is the mechanism through which a company translates its strategy into numbers, allocates resources with intention, and holds itself accountable to goals that were set with clear eyes rather than wishful thinking.

Without a budget, decisions about spending, hiring, investing, and pricing are made reactively, driven by what is happening today rather than what the business needs to achieve tomorrow. With a budget, every dollar has a purpose, every department knows its constraints and targets, and leadership has a reliable instrument for measuring whether the business is performing as planned.

This guide covers every dimension of financial budgeting: a precise definition drawn from multiple authoritative sources, a full breakdown of the six core budget types every business should understand, the five capital budgeting methods used to evaluate major investments, proven approaches for choosing the right budgeting methodology, and a practical step-by-step process for building a budget that serves as a genuine management tool rather than an annual paperwork exercise.

What Is a Financial Budget? Definitions from Leading Authorities

A financial budget means different things depending on the context, the business, and who is defining it. Here is how the leading finance authorities frame it, followed by a synthesized working definition.

Investopedia defines financial budgeting as the process of creating a plan to spend money. The budget should include all expected income and expenses, covering both short-term and long-term obligations for which the individual or organization is responsible.

Harvard Business Review frames it as a formalized process for setting objectives and tracking progress toward achieving those objectives over time. A key part of this process is developing a plan for managing resources effectively by anticipating needs, setting priorities, ensuring accountability, monitoring performance, and making adjustments when necessary.

All Finance Terms defines financial budgeting as the projection of income and expenditure for a given period. It calculates the income you will earn and save in relation to your expenses. Budgeting plans can be long-term or short-term depending on objectives, and typically encompasses balance sheets, income statements, and cash flow statements.

Forbes emphasizes that financial budgets should be thoughtfully planned with clear goals in mind, involving forecasting revenues and expenses so that a business can assess how much money is genuinely available to reach those goals.

The Working Definition

Bringing these perspectives together: a financial budget is a forward-looking financial plan that quantifies a company’s expected revenues, expenses, and capital flows over a defined period, aligned explicitly with the organization’s strategic goals. It is simultaneously a planning tool, a performance benchmark, a communication mechanism, and a risk management instrument. The best budgets are not static documents but living frameworks that adapt as circumstances change while keeping the organization anchored to its objectives.

Why Financial Budgeting Matters: The Business Case

Before diving into types and methods, it is worth being explicit about why budgeting deserves serious organizational attention rather than being treated as an annual ritual.

Resource allocation discipline. Every organization operates with finite capital, people, and time. A budget forces explicit decisions about where those resources go, preventing the diffuse spending that occurs when no one is accountable for ensuring that investment priorities match strategy.

Performance accountability. A budget establishes financial targets against which actual results can be measured. Variance analysis, the comparison of actuals to budget, is one of the most powerful early-warning systems available to management, revealing where execution is on track and where intervention is needed before small problems become large ones.

Funding credibility. If a business is approaching venture capital firms, banks, or strategic partners for investment or financing, credible budget documents are not optional. Investors want evidence that leadership understands its financial dynamics and has a disciplined approach to deploying capital. Learn more about how investor-ready financial planning supports fundraising confidence.

Strategic alignment. The budgeting process forces conversations about priorities. When a department requests resources that exceed what the budget can accommodate, the organization must make trade-off decisions that clarify what it actually values. This process, while sometimes uncomfortable, is healthier than allowing ambiguity about priorities to persist.

Liquidity protection. The most immediate purpose of a budget is ensuring the business does not run out of cash. A clear forward view of inflows and outflows, with early identification of periods of potential shortfall, is the difference between managing through a tight quarter and being caught off-guard by an unexpected cash crisis.

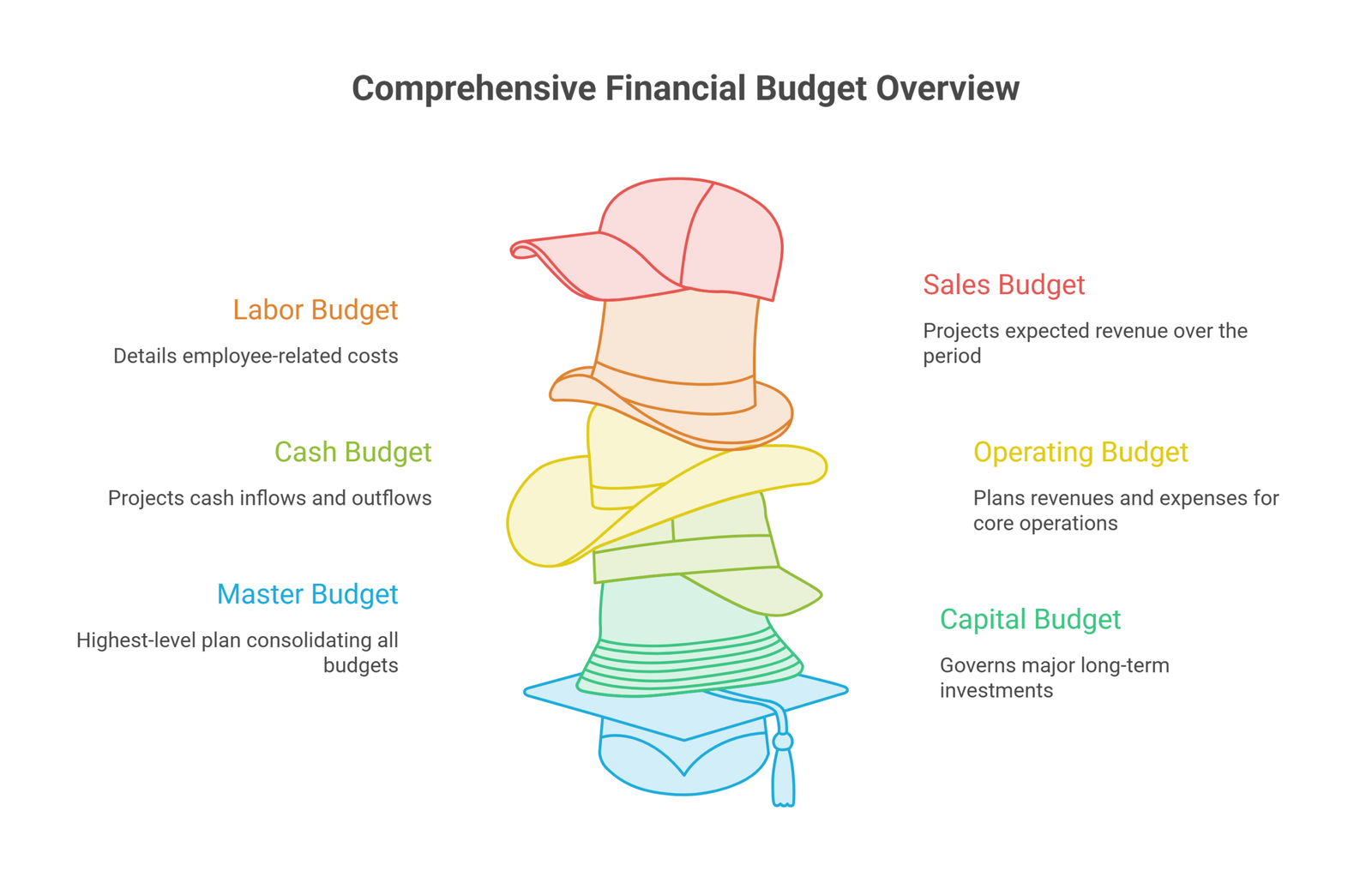

The Six Core Financial Budget Types

Different budget types serve different planning purposes. Large organizations typically use several simultaneously. Smaller businesses prioritize the types most relevant to their current challenges and growth stage.

1. Master Budget

The master budget is the highest-level financial plan of an organization. It consolidates all other budgets into a single integrated document that represents the company’s complete financial picture for the planning period.

What it includes: Revenue projections across all business lines, operating expense budgets from every department, capital expenditure plans, cash flow projections, and the resulting pro forma financial statements: projected income statement, balance sheet, and statement of cash flows. It covers both short-term and long-term horizons, typically with monthly or quarterly granularity within a one-year frame and directional projections extending two to five years.

Who should use it: The master budget is most valuable for mid-sized and larger businesses with multiple departments, cost centers, or revenue streams that need coordination. Smaller businesses benefit from a simplified version that captures the same essential dynamics without unnecessary complexity.

How it works in practice: Each functional area — sales, operations, human resources, finance — submits its own budget, which rolls up into the master. Senior leadership uses the consolidated view to identify where departmental plans are internally inconsistent, where trade-offs are needed, and whether the aggregate plan is likely to achieve the organization’s financial targets.

Industry applications: Construction companies rely on master budgets to coordinate project timelines, labor schedules, and material procurement across multiple simultaneous jobs. Retail chains use them to plan inventory purchases, staffing levels, and marketing spend seasonally. Manufacturing businesses use them to align production capacity with sales forecasts and capital investment plans.

2. Capital Budget

The capital budget governs decisions about major long-term investments in assets that will generate value over multiple years. Unlike the operating budget, which manages day-to-day revenue and expenses, the capital budget focuses on expenditures that build or maintain the productive capacity of the business.

What it covers: Purchases of property, plant, and equipment; technology infrastructure investments; facility expansions or renovations; vehicle fleets; and any other expenditure that will appear on the balance sheet as a long-term asset and be depreciated over time.

Why it matters: Capital investments are typically large, difficult to reverse, and have long-term consequences for the cost structure and capacity of the business. Making these decisions without a structured evaluation process — tying up capital in projects that do not generate adequate returns or depriving the business of liquidity it needs for operations — is one of the more consequential financial errors a business can make.

Who needs one: Every business that owns significant physical assets or technology infrastructure needs a capital budget. Manufacturing companies plan machinery upgrades. Technology companies budget for server infrastructure or software platforms. Healthcare organizations budget for medical equipment and facility improvements. Retail businesses budget for store renovations and point-of-sale systems.

The Five Capital Budgeting Evaluation Methods

Capital investment decisions require rigorous financial analysis because the stakes are high and the time horizons are long. Five methods are used in practice, each offering a different lens on the investment opportunity.

Internal Rate of Return (IRR) — IRR is the annualized rate of return that a project is expected to generate over its life. It is the discount rate at which the net present value of all project cash flows equals zero. A project is attractive when its IRR exceeds the company’s cost of capital (hurdle rate). IRR is intuitive because it expresses returns as a percentage, making it easy to compare against the cost of borrowing or the return available from alternative investments. The limitation is that IRR can be misleading when comparing projects of different sizes or when cash flows change direction multiple times.

Net Present Value (NPV) — NPV calculates the present value of all future cash flows generated by the investment, discounted at the company’s required rate of return, and subtracts the initial cost. A positive NPV means the investment is expected to create more value than it costs. NPV is considered by most finance authorities to be the theoretically superior method because it directly measures the dollar value of wealth creation and accounts for the full project life and the time value of money. For mutually exclusive projects where only one can be selected, the project with the highest positive NPV creates the most value. Use our NPV Calculator to evaluate your investments.

Profitability Index (PI) — The Profitability Index is calculated by dividing the present value of future cash flows by the initial investment. A PI greater than 1.0 indicates a value-creating project. PI is particularly useful when capital is constrained and the organization needs to rank a portfolio of projects to determine which combination creates the most value from available resources. Explore our business calculators for quick Profitability Index analysis.

Accounting Rate of Return (ARR) — ARR measures the expected annual profit from an investment as a percentage of the capital invested. It is simpler to calculate than NPV or IRR because it uses accounting profit figures rather than cash flows, but it does not account for the time value of money and can therefore give a misleading picture of long-horizon projects where early cash flows are worth more than later ones.

Payback Period — The payback period measures how long it takes for a project to recover its initial investment from the cash inflows it generates. Projects with shorter payback periods carry less risk because capital is at stake for a shorter time. It is the most intuitive metric for assessing investment risk and liquidity, though it ignores all cash flows after the payback point and does not account for the time value of money. Most organizations use it as a screening tool alongside NPV and IRR rather than as a standalone decision criterion.

3. Cash Budget

The cash budget is a forward projection of all expected cash inflows and outflows over a specific period, typically monthly or quarterly within a fiscal year. Its purpose is to ensure that the business maintains sufficient liquidity to meet its obligations at every point in time, not just on average over the year.

Why it is distinct from the income statement: A business can be profitable on an accrual basis and still run out of cash, because profit measures revenue earned and expenses incurred regardless of when cash changes hands. Understanding the difference between cash and profit is fundamental before building this budget. The cash budget captures the timing of actual cash movements, revealing periods when collections from customers lag behind payments due to suppliers, employees, and lenders.

What it projects: Opening cash balance, expected cash receipts from sales, collections on accounts receivable, loan proceeds, and other inflows; expected cash disbursements for payroll, vendor payments, rent, debt service, tax payments, and capital expenditures; and the resulting closing cash balance for each period. If the projected closing balance falls below the minimum operating reserve, the budget triggers a financing or cost-reduction decision before the shortfall actually occurs.

Who needs one: Every business that carries accounts receivable, manages inventory, has significant seasonal fluctuations in revenue or expenses, or operates with limited cash reserves needs a cash budget. It is especially critical for startups, rapid-growth companies burning cash faster than revenue comes in, and service businesses where client payment terms create timing mismatches.

Industry applications: Retail businesses use cash budgets to plan for the inventory investment required ahead of peak selling seasons. Construction firms use them to manage the gap between project milestones and client payment schedules. Service companies use them to ensure payroll can be met even when major client invoices are outstanding.

4. Operating Budget

The operating budget is a comprehensive plan for the revenues and expenses associated with a company’s core business operations over a defined period, typically one fiscal year. It is the most frequently used budget type and the one that drives day-to-day financial management decisions.

What it encompasses: Revenue projections by product, service line, or customer segment; cost of goods sold or cost of services; operating expenses including salaries, rent, utilities, marketing, technology, and administrative costs; and the resulting operating income. The operating budget excludes capital expenditures, financing costs, and non-operating items, which are handled in the capital budget and cash budget respectively.

How to build one effectively:

Step one is reviewing historical financial performance in detail, including prior-year actuals, to understand baseline revenue run rates, cost structures, and seasonal patterns.

Step two is developing revenue projections grounded in sales pipeline data, market conditions, pricing assumptions, and realistic growth rates. Revenue is the most consequential assumption in any operating budget, and optimism here cascades into every other line item.

Step three is modeling the cost of delivering those revenues, distinguishing between costs that scale directly with volume (variable costs) and costs that are fixed or semi-fixed regardless of revenue level.

Step four is projecting operating expenses by department or cost center, with each manager owning their portion of the budget and justifying their requests against the revenue and strategic priorities.

Step five is stress-testing the operating income result against downside scenarios to ensure the business remains viable if revenue comes in below plan.

Step six is establishing monthly variance tracking so that actual performance is compared to budget each month and corrective action is taken promptly when gaps emerge.

Industry applications: Manufacturing companies use operating budgets to plan production volumes, direct labor requirements, and overhead absorption rates. Technology companies use them to plan headcount growth, cloud infrastructure costs, and customer acquisition spending. Restaurant groups use them to manage food cost percentages, labor ratios, and venue-level profitability.

5. Labor Budget

The labor budget is a detailed plan for all employee-related costs over the budget period, including salaries, wages, benefits, payroll taxes, bonuses, overtime, and training expenditures. For most service and labor-intensive businesses, personnel costs represent the single largest expense category, making the labor budget one of the most consequential components of the overall financial plan.

Why it deserves dedicated attention: Labor costs are a mix of fixed (salaried employees), variable (hourly or commission-based workers), and semi-variable components. Getting this mix right requires forecasting not just total cost but staffing levels by role, location, and time period, matching headcount to projected workload rather than simply rolling forward last year’s numbers.

How to build one: Start with a complete inventory of current headcount by role and compensation level. Add expected new hires based on the operating plan’s revenue and workload projections, with specific target start dates. Include planned terminations, retirements, or restructuring. Apply anticipated salary increases, merit adjustments, and benefits cost changes. Layer in overtime estimates for roles with seasonal demand peaks. Add training and development costs. The result is a month-by-month view of total personnel cost that can be monitored against actual payroll.

Why it is valuable beyond cost tracking: A well-built labor budget reveals overstaffing and understaffing risks before they materialize. It identifies periods when hiring needs to occur months in advance to avoid productivity gaps. It makes explicit the connection between the sales plan and the headcount required to deliver it, catching plans that assume revenue growth without modeling the labor investment needed to generate it.

Industry applications: Retail and hospitality businesses, which employ large numbers of part-time and seasonal workers, use labor budgets to match staffing to foot traffic and revenue projections week by week. Manufacturing companies use them to manage shift patterns and overtime against production plans. Professional services firms use them to ensure billable headcount is sufficient to meet client delivery commitments while controlling bench costs.

6. Sales Budget

The sales budget is a projection of expected revenue over the budget period, broken down by product, service, customer segment, geography, or sales channel depending on how the business is structured. It is typically the first budget created in the planning cycle because every other budget — operating expenses, headcount, inventory, cash flow — depends on the revenue assumption.

What it consists of: Historical sales performance by category, which reveals trends and seasonality; current market conditions and competitive dynamics; the sales pipeline and conversion rates from leads to closed business; pricing assumptions including any planned changes; new product or service launches planned during the period; and the expected impact of marketing and sales investments. These inputs combine into a period-by-period revenue forecast.

Why getting the sales budget right is so important: An overoptimistic sales budget is the most common source of budget failure. When revenue comes in below plan, every downstream cost commitment made in anticipation of that revenue becomes a burden. Businesses that plan conservatively on revenue and aggressively on cost management have far more resilience than those that plan growth first and hope cost management follows.

Variance monitoring: The sales budget establishes monthly revenue targets against which actual bookings and recognized revenue are compared. Early identification of a revenue shortfall — in month two rather than month nine — gives leadership time to accelerate sales activity, adjust cost structures, or revise investor communications before the gap becomes unmanageable.

Industry applications: Consumer goods companies use sales budgets to plan production runs and retail channel inventory levels. Technology companies use them to model subscription growth rates and churn impacts. Professional services firms use them to forecast billable hours and effective billing rates across client portfolios.

Budgeting Methodologies: Choosing the Right Approach

Beyond the types of budgets, organizations must choose the methodology by which they construct and update them. The methodology determines how much baseline-carrying happens from prior periods, how rigorously each expense must be justified, and how frequently the budget is refreshed as actual results accumulate.

Traditional (Incremental) Budgeting

The most widely used approach. The prior year’s budget or actual results serve as the baseline, and departments negotiate incremental increases or decreases for the new period. It is fast, familiar, and administratively simple. The weakness is that it institutionalizes historical spending patterns without questioning whether those patterns remain optimal. Inefficiencies from prior years are embedded into future budgets almost automatically.

Best for: Stable businesses operating in predictable environments where the cost structure and revenue model are well understood and unlikely to change significantly.

Zero-Based Budgeting (ZBB)

Every expense in every department must be justified from a zero base each budget cycle, regardless of what was spent in prior periods. There is no assumption that last year’s allocation is a reasonable starting point. Managers must articulate why each expenditure is necessary and what value it delivers. Guess, the fashion brand, used ZBB during the pandemic to cut quarterly operating costs by USD 60 million in just a few weeks by eliminating spending that could not justify its existence. Kraft Heinz used ZBB to redirect resources toward more profitable business areas.

The trade-off is that ZBB is significantly more time-intensive than incremental budgeting, requires strong finance support, and can, if applied too aggressively, crowd out long-term investments whose value is not easily quantified in a single budget cycle.

Best for: Organizations with significant cost inefficiency, businesses undergoing transformation or restructuring, and companies that need to re-examine spending patterns that have accumulated over years without scrutiny.

Rolling Forecast Budgeting

Rather than producing a single annual budget and tracking against it for twelve months, rolling forecast budgeting continuously extends the planning horizon. Each month or quarter, a new period is added to the forecast so that the organization always has a fixed forward view of twelve or more months. Rolling forecasts replace stale annual assumptions with updated information as the year progresses, making them especially valuable in fast-moving or uncertain environments.

Research consistently shows that leading finance organizations have adopted rolling forecasts as standard practice, yet most organizations still rely on static annual budgets. The gap between the two approaches creates a significant competitive information advantage for those that update their forecasts continuously.

Best for: High-growth companies, businesses operating in volatile markets, and any organization where quarterly or annual planning cycles produce forecasts that become materially inaccurate before the period ends.

Flexible Budgeting

A flexible budget adjusts key expense lines automatically based on actual revenue or volume. Rather than holding expense targets fixed regardless of whether revenue comes in above or below plan, flexible budgeting scales variable costs proportionally to actual business activity. This makes variance analysis more meaningful because it separates the variance caused by volume differences from the variance caused by genuine cost inefficiency.

Best for: Businesses with significant variable cost structures, such as manufacturers, distributors, and service businesses where labor and materials scale with output volume.

How to Build an Effective Financial Budget: A Practical Process

Regardless of which budget type or methodology applies to your business, the construction process follows a consistent logic. Working with experienced budgeting consultants can help align each step with your strategic vision.

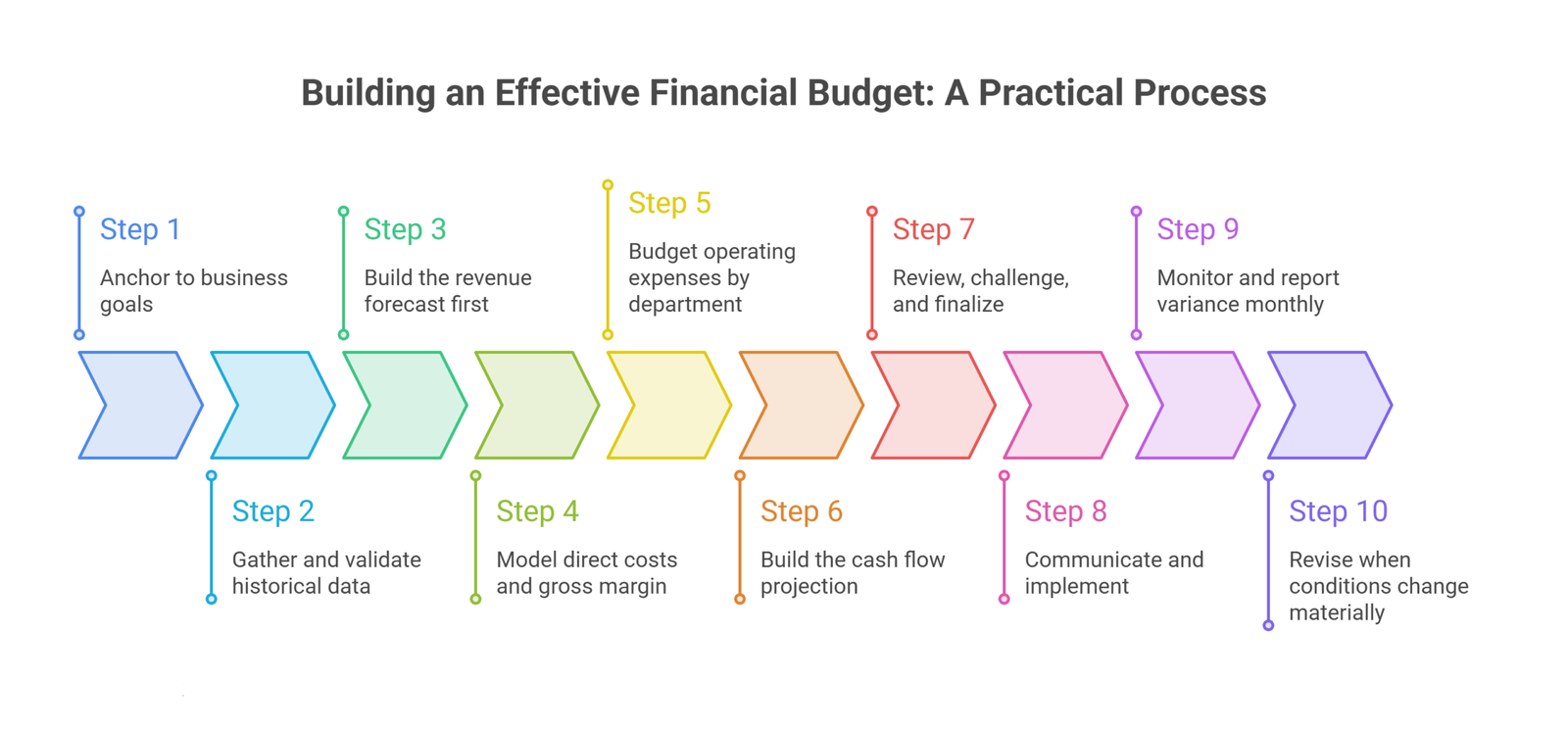

Step 1: Anchor to Business Goals. Start with the strategic objectives for the period. Revenue growth targets, market expansion plans, new product launches, operational improvements, and profitability goals all translate into financial resource requirements. A budget that is not connected to strategy is just a spreadsheet.

Step 2: Gather and Validate Historical Data. Pull at least two to three years of actual financial results. Identify trends, seasonality patterns, cost ratios, and any historical anomalies that should not be extrapolated forward. The quality of the budget is directly tied to the quality of the data informing it.

Step 3: Build the Revenue Forecast First. Work bottom-up from pipeline data, customer contracts, pricing assumptions, and market conditions. Apply conservative adjustments to early-stage pipeline where conversion timing is uncertain. The revenue forecast sets the ceiling for every cost commitment that follows.

Step 4: Model Direct Costs and Gross Margin. For every revenue assumption, model the direct costs associated with delivering it: cost of goods sold, direct labor, materials, commissions. Establish the gross margin expectation for each revenue category, as this determines how much is available to fund operating expenses.

Step 5: Budget Operating Expenses by Department. Have each department leader build their expense budget from their operational plan, identifying what they need to accomplish their goals within the constraints of the revenue forecast and gross margin. Challenge assumptions that do not connect clearly to outputs or strategic priorities.

Step 6: Build the Cash Flow Projection. Convert the accrual-basis income statement assumptions into a monthly cash flow forecast, accounting for the timing of collections on receivables, payment of payables, and the impact of capital expenditures and debt service. Identify any periods where cash is projected to fall below the minimum operating reserve and plan the response.

Step 7: Review, Challenge, and Finalize. Senior leadership reviews the consolidated budget against strategic goals, financial benchmarks, and prior-year performance. Identify where the plan is internally inconsistent or where assumptions appear unrealistic. Adjust and confirm.

Step 8: Communicate and Implement. Share the approved budget with all budget owners so that everyone understands their targets, constraints, and how their budget connects to the overall business plan.

Step 9: Monitor and Report Variance Monthly. Compare actuals to budget each month. Investigate significant variances, both favorable and unfavorable, to understand whether they reflect a real change in the business environment or execution issues that can be corrected. Use the analysis to inform rolling forecast updates.

Step 10: Revise When Conditions Change Materially. A budget built on assumptions that are now clearly wrong is not a useful management tool. When market conditions, competitive dynamics, or business performance diverge significantly from the plan, update the forecast to reflect reality while keeping the original budget as a benchmark for understanding what changed and why.

Common Financial Budgeting Mistakes to Avoid

Revenue optimism without pipeline discipline. Building revenue targets without grounding them in actual sales pipeline data and realistic conversion rates produces budgets that disappoint almost every quarter.

Treating the budget as a ceiling rather than a plan. Managers who see the budget as a permission slip to spend up to their allocated amount, rather than a target to achieve outcomes efficiently, will consistently spend to budget regardless of whether results warrant it.

Failing to update when assumptions break. Organizations that cling to an annual budget long after market conditions have made it irrelevant are not managing with financial discipline. They are managing with a document.

Building the budget in a silo. Finance-only budgets that do not involve operational leaders in building their own cost and revenue assumptions produce plans that operations does not own and will not actively manage against.

Ignoring cash timing. An operating budget that shows a profitable year can still produce a cash crisis if the timing of cash inflows and outflows is not managed. The cash budget is not an optional supplement; it is essential.

Frequently Asked Questions

How often should a business update its budget?

Most businesses keep a static annual budget as the benchmark and maintain a rolling forecast updated monthly or quarterly. In volatile or high-growth environments, update forecasts more frequently.

What is zero-based budgeting (ZBB) and when should it be used?

Zero-based budgeting requires justifying every expense from scratch each cycle instead of rolling over last year’s numbers. Best used during cost crises, restructuring, or major strategic shifts. It is more time-consuming but delivers strong cost discipline.

What is the difference between an operating budget and a capital budget?

The operating budget covers day-to-day revenues and expenses such as salaries, rent, and marketing. The capital budget covers long-term asset investments, equipment, buildings, and major technology, that appear on the balance sheet.

How does a master budget differ from other budgets?

The master budget is the complete consolidated view. It combines the sales, operating, labor, capital, and cash budgets into one integrated financial plan.

Can small businesses benefit from formal budgeting?

Yes. Even a simple budget (monthly cash flow plus revenue targets) gives owners far better control. Scale the complexity to the size of the business — the discipline matters more than the detail.

What is the payback period and how is it used in capital budgeting?

The payback period calculates how long it takes to recover the initial investment from project cash flows. It is a simple risk and liquidity screen where a shorter period is preferable. It should be used alongside NPV and IRR, as it ignores the time value of money and cash flows that occur after the payback point.

Conclusion

A financial budget is among the most powerful management tools available to any business, regardless of size or industry. When built rigorously, connected to strategy, and monitored actively throughout the year, it transforms financial management from a reporting function into a genuine driver of business performance.

The six budget types covered in this guide, master, capital, cash, operating, labor, and sales, each serve a distinct purpose and together form a comprehensive financial planning system. The five capital budgeting methods provide the analytical framework for making major investment decisions with discipline. And the choice of budgeting methodology, from traditional incremental approaches to zero-based, rolling, or flexible frameworks, should reflect the business environment and the organization’s need for agility versus administrative efficiency.

The businesses that budget well do not just track where money went. They decide in advance where money should go, hold themselves accountable to those decisions, and learn from the gaps between plan and reality in ways that make the next planning cycle better than the last.If you need expert support in building or refining your financial budget, Oak Business Consultant offers CFO services, financial modeling, and budgeting consulting tailored to businesses of all sizes. Explore our free tools and templates or contact us to discuss your needs.