Chart of Accounts and Bookkeeping for a Consulting Business

Introduction to Chart of Accounts and Bookkeeping for a Consulting Business

Export your P&L from QuickBooks and you’ll likely see one line for “Consulting Revenue” and one for “Operating Expenses.” Both numbers are accurate. Neither tells you which clients are profitable, which service line is carrying the firm, or where your margin is quietly leaking out. That gap almost always traces back to one document: your chart of accounts.

A chart of accounts (CoA) is the categorized list of every account in your general ledger. If a category doesn’t exist in your CoA, it can’t show up on a report, no matter how good your bookkeeper is. For a consulting business, getting this structure right isn’t a filing exercise. It’s what turns your books from “technically correct” into a tool you can actually use to run the business. This guide walks through the account categories a consulting firm needs, how to number them so they scale, and the strategies that keep the bookkeeping behind them accurate.

What is a chart of accounts?

A chart of accounts is a structured list of every financial account in your general ledger, organized into five categories: assets, liabilities, equity, revenue, and expenses. Each account gets a name, a short description, and an identifying number.

Think of it as the filing system your bookkeeper uses to sort every transaction. One drawer labeled “stuff” tells you nothing. Labeled folders for every category you care about tell you exactly where your money is going and coming from. Consulting firms that skip this step end up with financial statements that are accurate but strategically useless: they show the totals, not the “why.”

The five core account categories

Every consulting business, regardless of size, needs these five account types in its chart of accounts:

| Category | What it tracks | Typical number range |

| Assets | What the firm owns | 1000–1900 |

| Liabilities | What the firm owes | 2000–2900 |

| Equity | The owner’s stake in the business | 3000–3900 |

| Revenue | Money earned from clients | 4000–4900 |

| Expenses | Money spent to run the business | 5000–5900 |

Assets

- Cash and cash equivalents

- Accounts receivable

- Short-term marketable securities

- Computer and office equipment

- Furniture and fixtures

- Leased equipment

Liabilities

- Accounts payable

- Notes payable

- Short-term loans and bank overdrafts

- Income taxes payable

- Accrued expenses (payroll, unpaid contractor invoices)

Equity

- Owner contributions

- Owner withdrawals

- Owner compensation

- Retained earnings

These three categories track the same fundamentals across most small businesses. Where consulting firms need to think differently is revenue and expenses, because a generic small-business template will actively hide the numbers that matter most.

Why “consulting revenue” isn’t a real revenue account

A single “Consulting Revenue” account can only answer one question: what’s your total revenue? It can’t tell you which service line is growing, which clients are worth keeping, or whether your retainer work is subsidizing your project work.

Break revenue into layers that mirror how the business actually makes money:

By service line. Separate accounts for each major offering, such as Strategy Consulting Revenue, Operations Consulting Revenue, and Implementation Services Revenue. A firm earning $900K with $100K profit looks like an 11% margin overall, but the service-line breakdown might show strategy work running at 35% margin while implementation limps along at 3%. Lump them together and that difference disappears.

By client type. Retainer Revenue, Project Revenue, and Hourly Revenue behave differently in terms of cash flow. Retainers arrive monthly and are easier to forecast. Project revenue lands at milestones and is lumpier. Knowing your mix tells you how predictable next quarter’s cash actually is.

Reimbursable revenue, separated out. When you bill a client for travel or a subcontractor, that money passes through your books but isn’t revenue you actually earned. Give it its own account (Reimbursable Revenue) so it doesn’t inflate your margin calculations. A financial model built for consulting businesses will already separate this out; your chart of accounts should match it.

Structuring expenses to separate direct costs from overhead

Gross margin only means something once direct project costs are isolated from fixed overhead. Most consulting firms should be running a 60% to 75% gross margin and a 15% to 25% operating margin. If your numbers sit well outside that range, the chart of accounts is usually why: everything is lumped into “general expenses” and nobody can see what’s driving the gap.

Direct project costs exist only because you have clients. These include:

- Contractor and subcontractor payments

- Project-specific software or licenses

- Client travel

Overhead exists regardless of how much work is on the books:

- Rent and facilities

- Insurance

- Marketing

- General software and admin tools

- Professional fees (accounting, legal, bookkeeping)

Compensation deserves its own breakdown by role, not one lump “payroll” account. Splitting Senior Consultant Salary from Junior Analyst Salary lets you calculate revenue per employee by seniority; a senior consultant generating $300K against $120K in comp is covering their cost 2.5 times over, while a junior analyst at $80K generated against $65K in comp is closer to 1.2 times, which changes how you think about utilization targets for each role.

This structure is also where a fractional CFO earns their keep: turning these account splits into a monthly margin review rather than a spreadsheet nobody opens.

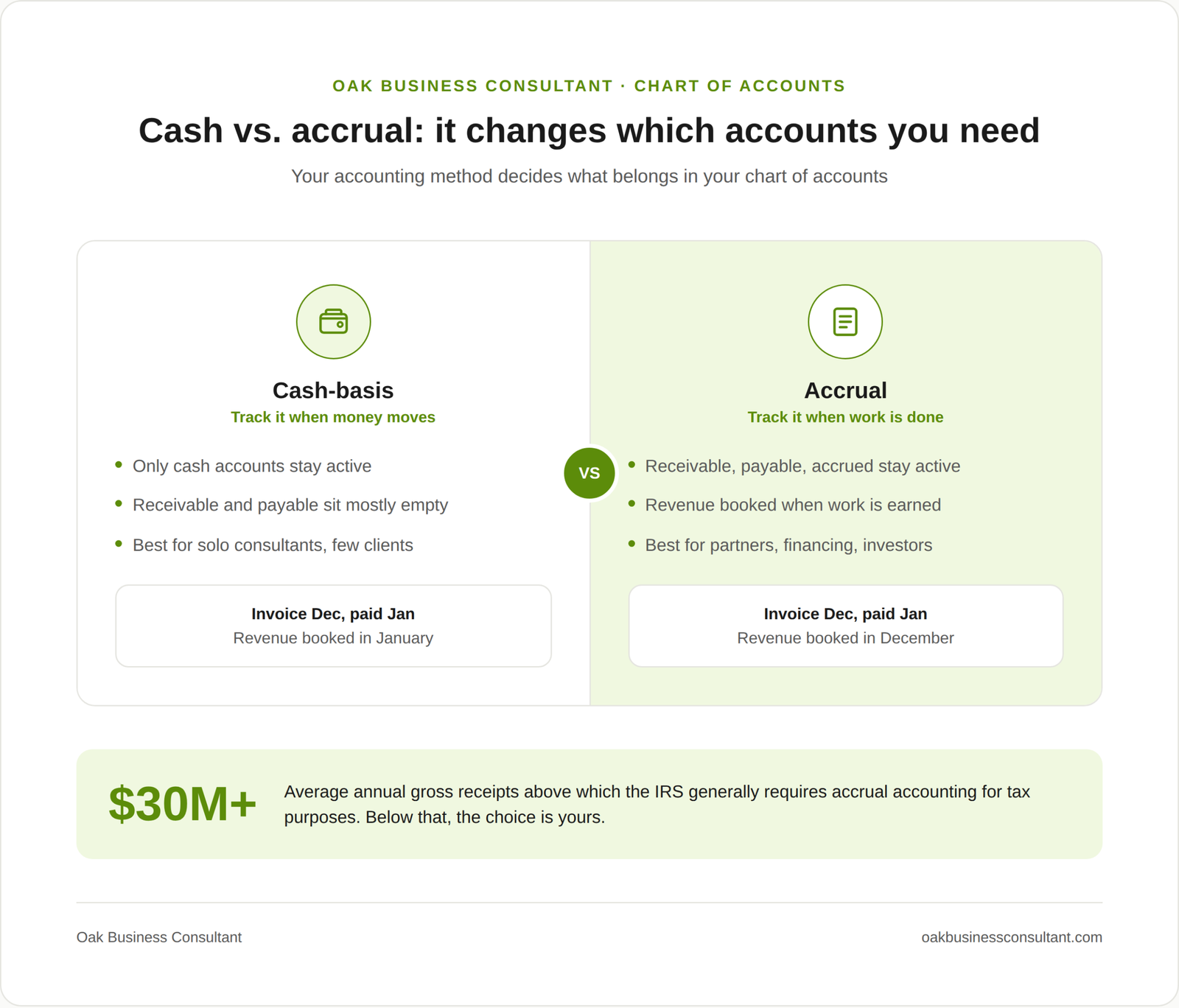

Cash vs. accrual: it changes which accounts you even need

Your accounting method decides which accounts belong in your chart of accounts, not just how you record transactions in them.

Under cash-basis accounting, you record revenue when the client’s payment hits your bank account and expenses when you actually pay them. Accounts Receivable and Accounts Payable barely matter here, since money is only tracked once it moves. This works fine for a solo consultant billing a handful of clients directly.

Under accrual accounting, you record revenue when you complete the work, regardless of when the client pays. That means Accounts Receivable, Accounts Payable, and Accrued Expenses become active accounts you’re updating constantly, not line items that sit empty. If you invoice a client in December for work finished that month but they pay in January, accrual accounting books that revenue in December. Cash-basis accounting books it in January.

The IRS generally requires businesses averaging above roughly $30 million in annual gross receipts to use accrual accounting for tax purposes. Below that threshold, you can choose. But once you bring on partners, take outside financing, or need financials a bank or investor will actually rely on, accrual accounting becomes the practical standard, since it’s what GAAP requires and what lenders expect to see.

Account numbering that scales

A four-digit numbering scheme keeps a consulting firm’s chart of accounts organized as it grows. Within each major range, leave gaps so you can insert new accounts later without renumbering everything:

- Assets: 1000–1900

- Liabilities: 2000–2900

- Equity: 3000–3900

- Revenue: 4000–4900, with sub-ranges like 4100–4199 for service-line accounts

- Direct project costs: 5000–5499

- Overhead: 5500–5900

Map your services, client types, and major expense categories before assigning numbers. For each potential account, ask a simple test: would you make a materially different decision if you could see this category on its own? If yes, give it an account. If not, group it with something similar rather than creating fifty accounts for minor expenses nobody reviews. Firms that want a starting point rather than building from scratch can use a ready-made chart of accounts template and adjust the account names to match their own service lines.

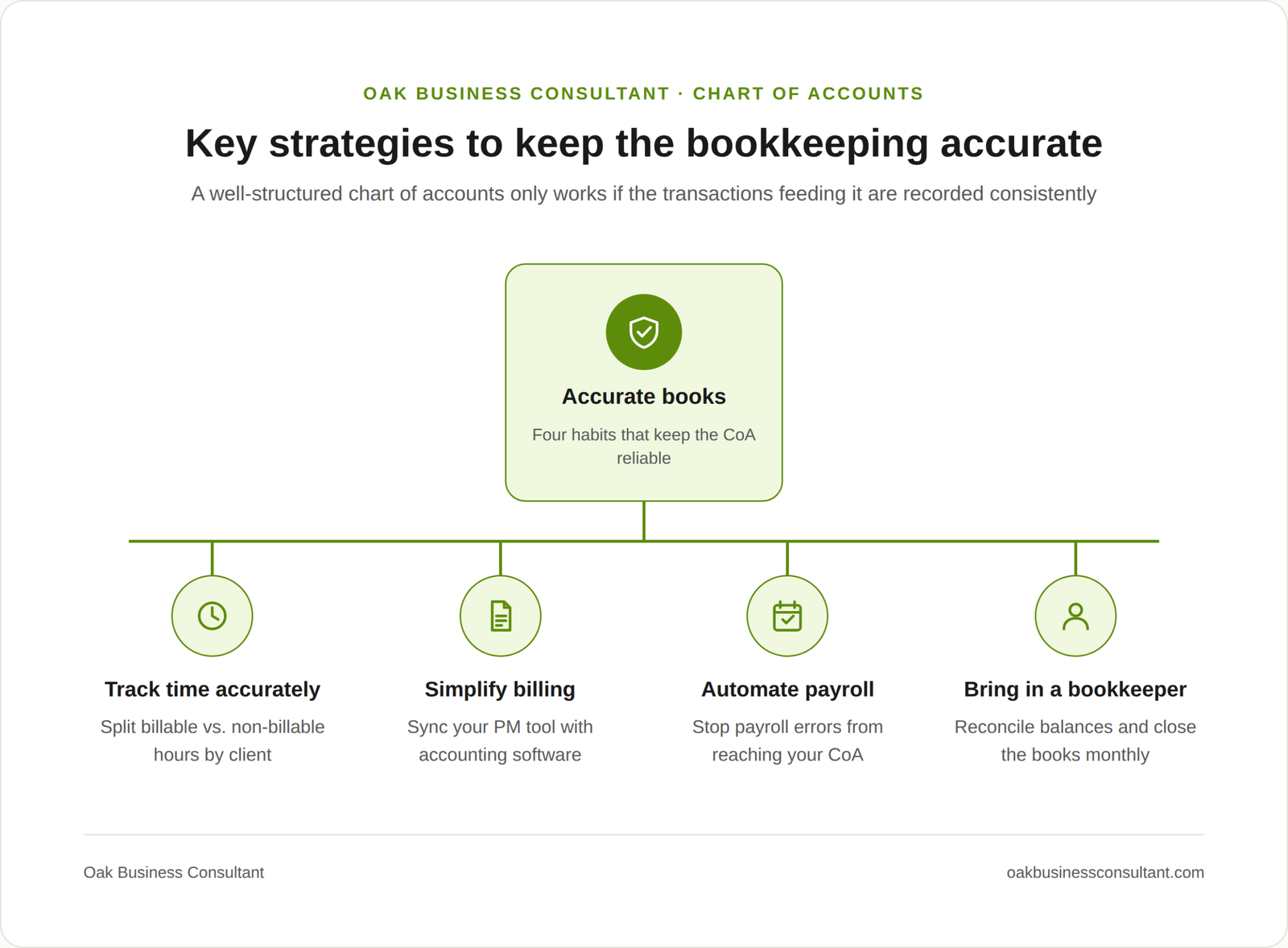

Key strategies to keep the bookkeeping behind it accurate

A well-structured chart of accounts only works if the transactions feeding it are recorded consistently. A few habits keep that from breaking down.

Track time properly. Accurate time records let you separate billable from non-billable hours by client and project, which feeds directly into your financial budgeting for future engagements. Research and client communication often feel non-billable but still cost money; tracking them gives a truer picture of profitability than billable hours alone.

Simplify billing. Connecting your project management system to your accounting software cuts down on manual invoice creation and speeds up collections. Solo consultants can often get by entering project details directly into their accounting software without a separate system. For the accounting platform itself, most consulting firms are well served by QuickBooks Online, since its chart of accounts supports the industry-specific customization this guide describes. Xero is a reasonable alternative for firms that prioritize simplicity or bill clients in multiple currencies.

Automate payroll. A timely, accurate payroll process prevents errors from bleeding into your chart of accounts, since payroll entries flow straight into the income statement. Time-tracking software that integrates with payroll reduces duplicate entries and missed hours.

Bring in a bookkeeper. Someone needs to own reconciling bank and credit card balances, categorizing transactions correctly against your CoA, and closing the books each month. Outsourcing this to an accounting and bookkeeping partner frees you up to run client work instead of chasing receipts.

Frequently asked questions

What are the 5 basic categories in a chart of accounts?

Assets, liabilities, equity, revenue, and expenses. Every transaction a consulting business records falls into one of these five groups.

Why isn’t a generic QuickBooks template enough for a consulting firm?

Generic templates are built for product businesses tracking inventory and COGS. Consulting firms need to see utilization rates, project profitability, and revenue per consultant, none of which a single “services revenue” account can show.

What expense category does consulting work fall under?

Fees paid to outside consultants are recorded as Professional Fees within operating expenses. For the consulting firm earning those fees, the same money is recorded as revenue, ideally split by service line rather than lumped together.

How often should a consulting firm review its chart of accounts?

Review categorization with your bookkeeper quarterly, and revisit the account structure itself roughly twice a year. Add new accounts when you launch a new service, enter a new market, or change your delivery model.

What’s the best business structure for a consulting company?

An LLC is the most common choice for the liability protection and simpler bookkeeping. An S-Corp becomes more attractive as revenue grows, for the tax treatment of owner compensation and payroll taxes. The right fit depends on firm size, growth plans, and funding needs.

Should a consulting firm use cash or accrual accounting?

Solo consultants billing a few clients directly can often stay on cash-basis accounting. Firms with partners, employees, outside financing, or clients who pay on delayed terms typically need accrual accounting, since it activates Accounts Receivable and Accounts Payable and matches revenue to the period the work was actually done.

Conclusion

A consulting firm’s chart of accounts is the difference between books that are technically accurate and books you can actually run decisions on. Structuring revenue by service line and client type, separating direct project costs from overhead, and numbering accounts with room to grow takes a few hours upfront. Skipping it costs months of cleanup once the firm hits the size where investors or lenders start asking for profitability by service line.

Bookkeeping built for how consulting firms actually make money

Generic templates miss the accounts that matter for a professional services firm. Our bookkeeping team builds and maintains a chart of accounts structured around your service lines, client types, and margin targets, so your monthly reports answer the questions you’re actually asking. Talk to a bookkeeping expert.

{kind=link}