Mastering the Stress Test Financial Model

Stress Test Financial Model Guide

Building a robust stress test financial model is no longer optional for financial institutions; it is the cornerstone of survival in today’s regulatory and economic environment. A well-designed stress test financial model integrates the balance sheet, income statement, and cash flow projections under severe yet plausible adverse scenarios, enabling banks to prove capital adequacy to the Federal Reserve, European Banking Authority, Bank of England, and other regulatory bodies. Whether you are preparing for the Comprehensive Capital Analysis and Review (CCAR), Dodd-Frank Act Stress Tests (DFAST), EBA stress exercises, or internal capital adequacy assessment processes, your stress test financial model will determine if your institution can withstand economic downturns, financial crises, or hypothetical scenarios without breaching minimum capital requirements.

This article dives deep into everything you need to know to create, validate, and defend a best-in-class stress test financial model that outperforms what most competitors currently rank for.

Why the Stress Test Financial Model Has Become the Most Critical Tool in Banking

After the 2008 financial crisis, regulators worldwide realized that traditional capital ratios were meaningless if they collapsed during real stress. The Dodd-Frank Act in the U.S. and Basel III globally introduced mandatory supervisory stress testing. Today, every major bank runs an enterprise-wide stress testing program built around a central stress test financial model that links:

- Balance sheet dynamics (loan growth, deposit behavior, securities portfolio)

- Income statement sensitivity (net interest income, fee income, credit losses)

- Risk parameters (probability of default, loss given default, exposure at default)

- Capital adequacy ratios (CET1, Tier 1, Total Capital, Leverage Ratio, Stress Capital Buffer)

The Federal Reserve, through its annual CCAR and DFAST exercises, uses its own models to challenge the bank-submitted stress test financial model. Passing is not just about meeting minimums; failing can restrict dividends, share buybacks, and executive bonuses for years.

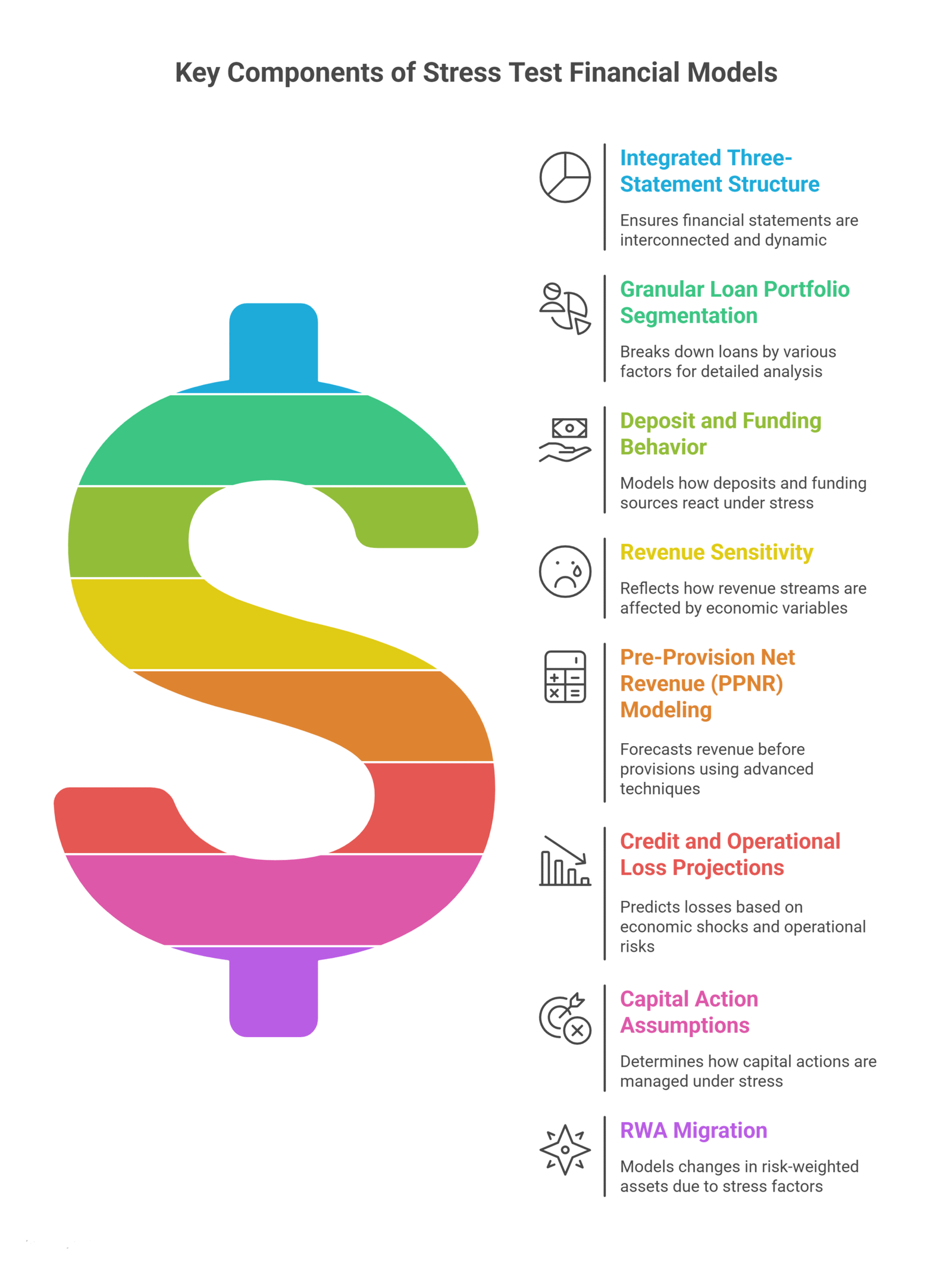

Core Components Every Stress Test Financial Model Must Include

- Integrated Three-Statement Structure

Your stress test financial model must start with fully integrated core statements: balance sheet, income statement, and cash flow statement. Most weak models treat these in silos. Best-practice models roll the balance sheet forward month-by-month (or quarter-by-quarter) under baseline, adverse, and severely adverse scenarios. - Granular Loan Portfolio Segmentation

Segment loans by product (residential mortgage, CRE, C&I, credit cards, auto), geography, FICO/vintage, and risk rating. Apply scenario-specific PD, LGD, and prepayment vectors. - Deposit and Funding Behavior

Model non-operational deposit runoff, wholesale funding cost spikes, and liquidity management actions under stress. - Revenue Sensitivity

Net interest income compression, fee income collapse, and trading book shocks must flow logically from macro-economic variables (GDP, unemployment, home prices, interest rates, equity markets). - Pre-Provision Net Revenue (PPNR) Modeling

The most scrutinized part of any U.S. stress test financial model. Use a combination of driver-based forecasting and statistical techniques (panel regression, ARIMA, machine learning) while maintaining auditability. - Credit and Operational Loss Projections

Link macro-economic shocks directly to loss rates. Include operational risk events that typically spike during recessions (fraud, litigation, model risk). - Capital Action Assumptions

Decide whether to keep dividends and buybacks fixed, suspend them, or model them dynamically based on capital ratios. - RWA Migration

Risk-weighted assets often balloon in stress due to rating downgrades and model parameter floors (Basel III output floor impact).

Scenario Design and Macro-Economic Variables

The best stress test financial model is only as good as the scenarios you feed it. Regulators publish baseline, adverse, and severely adverse macro-economic scenarios (unemployment peaking at 10-12%, GDP contracting 6-8%, equity markets down 50-65%, etc.). Top-tier banks supplement these with internal scenarios that reflect their specific risk profile and risk appetite.

Common variables to satellite into the stress test financial model:

- GDP growth

- Unemployment rate

- House Price Index (Case-Shiller or FHFA)

- Commercial real estate price index

- Corporate bond spreads (Baa, High Yield OAS)

- 3-month Treasury, 10-year Treasury, Fed Funds path

- Oil price, USD index, VIX

Advanced teams now incorporate climate risk, geopolitical shocks, and cyber scenarios into their enterprise-wide stress testing models.

Model Validation, Error Checks, and Governance

Even the most sophisticated stress test financial model will be torn apart in regulatory exams if proper governance is missing. Implement:

- Hard-coded error checks and sanity tests (balance sheet always balances, retained earnings roll correctly)

- Formula logic transparency (no hidden circularities or hard-coding)

- Sensitivity analysis and Monte Carlo simulation around key assumptions

- Comprehensive documentation (model inventory, methodology papers, user guides)

- Independent model validation by a dedicated team reporting to the Chief Risk Officer

Real-World Example: 2023 CCAR Severely Adverse Scenario

In the Fed’s 2023 scenario, unemployment rose to 10%, equities fell ~55%, and house prices dropped 28%. Banks that had conservative deposit beta assumptions and aggressive commercial office loan loss projections in their stress test financial model sailed through. Those still using pre-COVID assumptions faced massive objections and capital plan denials.

Frequently Asked Questions

How long does it take to build a production-grade stress test financial model?

A first-version integrated model can be built in 3-6 months by an experienced team. Reaching regulatory-grade quality with full documentation and validation typically takes 12-18 months of iteration.

Excel or specialized software?

While many mid-size banks still run the core stress test financial model in Excel (with heavy VBA), large institutions have migrated to Python, SAS Stress Testing suites, Moody’s Analytics, or custom scenario tools for speed and scalability.

Do we really need monthly granularity?

For CCAR and DFAST, the Federal Reserve requires nine-quarter projections, but running the stress test financial model monthly catches intra-quarter liquidity and capital cliffs that quarterly models miss.

How do we handle the FR Y-14 reporting schedules?

Map every line item in your stress test financial model directly to the Y-14A, Y-14Q, and Y-14M templates from day one. It saves hundreds of hours during submission season.

Is machine learning allowed in regulatory stress testing?

Yes, but with heavy challenger models and explainability requirements. Pure black-box models will be rejected during the supervisory process.

What is the biggest mistake most banks make?

Treating stress testing as a compliance exercise instead of a strategic decision-support tool used by the CFO, CRO, and the board for capital planning, risk appetite setting, and business valuation.

Conclusion

The difference between an average stress test financial model and a great one is not complexity; it is integration, transparency, and relentless focus on how the bank actually makes and loses money under stress. Invest the time upfront in driver-based logic, bullet-proof error checks, and scenario flexibility, and your stress test financial model will not only satisfy the Federal Reserve, EBA, or Bank of England; it will become the single most valuable risk management and decision-support tool your institution owns. Start building (or rebuilding) your stress test financial model today. In the next crisis, it will be the only thing standing between your bank and catastrophe.

Ready to master your financial future? Contact us today to deploy expert-level risk models that drive superior decision making and growth.