Balance Sheet vs Income Statement

Balance sheet vs income statement: what each one actually shows

A business can show a healthy profit on paper and still run out of cash the same month. That gap confuses a lot of first-time founders, and it comes down to reading only one financial statement instead of both. The income statement can tell you the business made money last quarter. The balance sheet is what tells you whether that money is actually sitting in the bank, tied up in unpaid invoices, or already spent on equipment. You need both to know where you really stand.

This guide breaks down what a balance sheet and an income statement each report, how they differ, how they connect to each other, and which one to reach for depending on the decision in front of you.

What a balance sheet shows

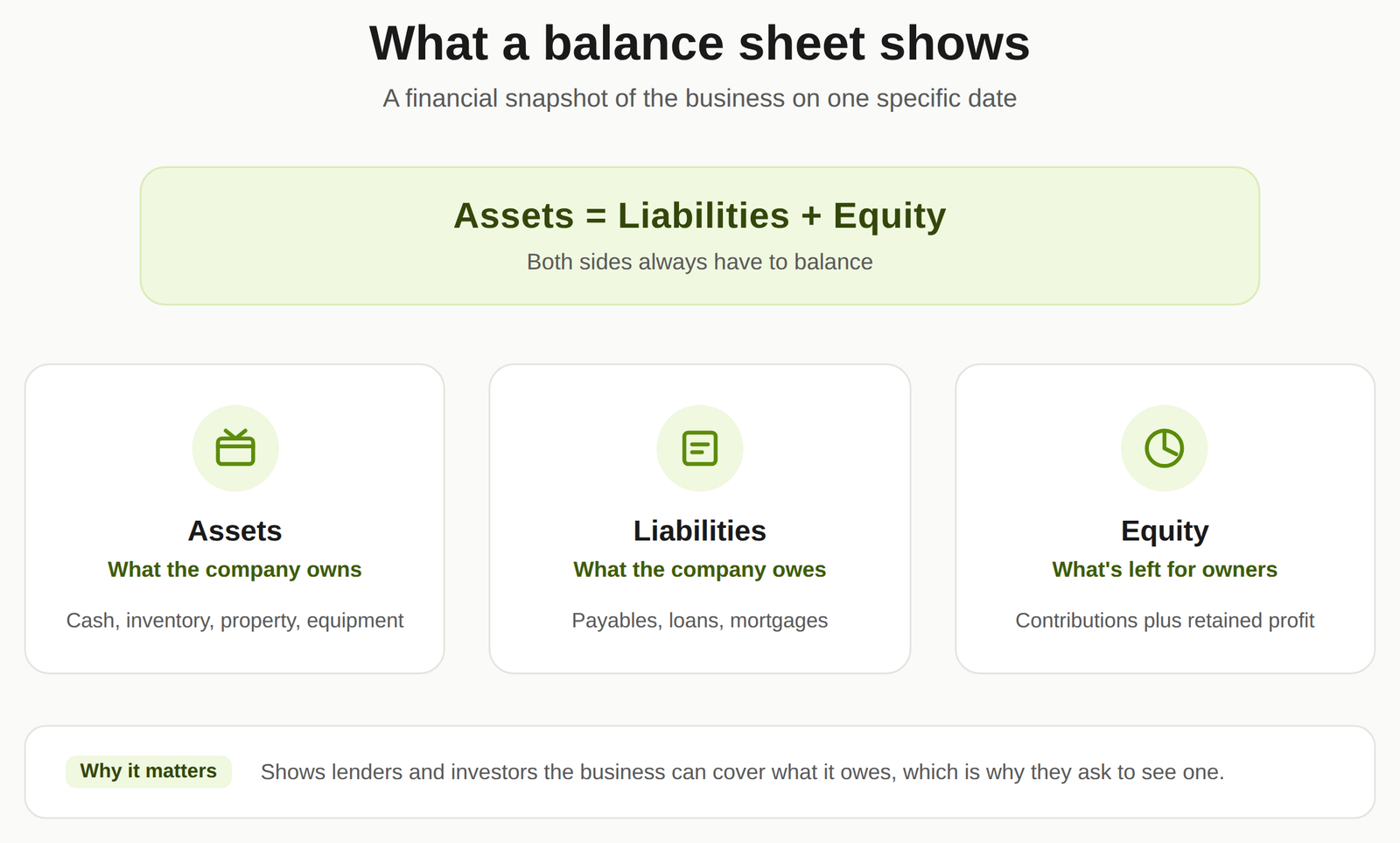

A balance sheet is a snapshot of your business on one specific date. Not a month, not a quarter, one day. It lists three things: what the company owns (assets), what it owes (liabilities), and what’s left over for the owners (equity).

It follows a simple equation that always has to balance, which is where the name comes from:

Assets = Liabilities + Equity

If that equation doesn’t balance, something in the books is wrong.

Assets

Assets split into two groups. Current assets are things you can turn into cash within a year: cash on hand, money customers owe you (accounts receivable), and inventory sitting on shelves. Long-term assets take longer to convert, things like property, equipment, or patents.

Liabilities

Liabilities also split by timing. Current liabilities are due within a year, including accounts payable, short-term loans, and wages you owe but haven’t paid out yet. Long-term liabilities are debts stretching past a year, like a mortgage on your office or a multi-year equipment loan.

Equity

Equity is what’s left after you subtract liabilities from assets. It represents the owners’ stake in the business: money they put in directly, plus profits the company has kept rather than paid out as dividends.

A balance sheet with strong assets and manageable liabilities tells lenders and investors the business can cover what it owes and still has room to grow. That’s why banks ask for one before approving a loan, and why investors want to see one before writing a check.

Most small businesses use a vertical balance sheet, listing assets, liabilities, and equity top to bottom on a single date. Larger companies sometimes also prepare a horizontal balance sheet, laying two or more periods side by side to track how each line item has moved over time. Neither format changes what’s being reported, just how it’s arranged for comparison.

What an income statement shows

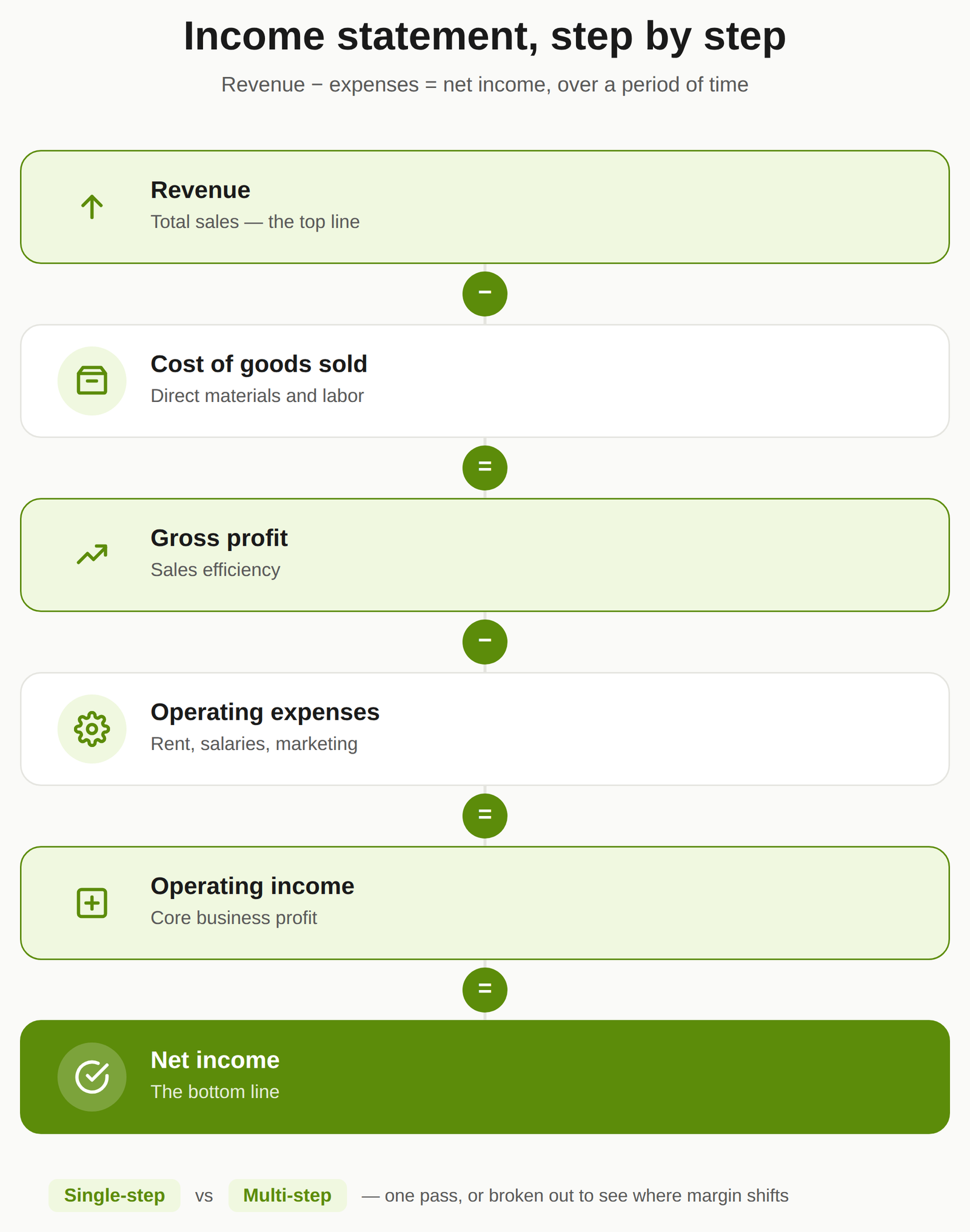

An income statement, also called a profit and loss statement or P&L, covers a period of time rather than a single date, usually a month, quarter, or year. It answers a narrower question than the balance sheet: did the business make money during that period, and how much?

The formula here is:

Revenue − Expenses = Net income

Revenue

Moreover, revenue is everything the business earned from selling its products or services during the period, before any costs are subtracted. This is often called the top line.

Cost of goods sold

Cost of goods sold, or COGS, covers the direct costs of producing whatever you sold, materials and labor most commonly. Subtract COGS from revenue and you get gross profit, which tells you how efficiently the business turns raw costs into finished sales.

Operating expenses

Operating expenses are the costs of running the business day to day: rent, salaries not tied directly to production, marketing, software subscriptions. These get subtracted from gross profit to arrive at operating income.

Net income

Net income, the bottom line, is what’s left after every expense, tax, and non-operating cost gets subtracted from revenue. A positive number means the business turned a profit for the period. A negative one means it operated at a loss.

Small businesses often use a single-step income statement, subtracting total expenses from total revenue in one pass. A multi-step income statement breaks that out into gross profit, operating income, and net income separately, which makes it easier to see exactly where margin is being gained or lost.

Balance sheet vs income statement: the core differences

The two statements answer different questions, cover different time frames, and get used by different people for different decisions.

| Balance sheet | Income statement | |

| Time frame | Snapshot on one date | Covers a period (month, quarter, year) |

| Core question | What do we own and owe right now? | Did we make money during this period? |

| Formula | Assets = Liabilities + Equity | Revenue − Expenses = Net income |

| Main sections | Assets, liabilities, equity | Revenue, expenses, net income |

| Used for | Assessing solvency, liquidity, and net worth | Assessing profitability and operating efficiency |

| Typical reader | Lenders, investors, board members | Managers, investors, tax authorities |

A balance sheet is closer to a photograph. An income statement is closer to a video. One captures a moment, the other captures movement over time, and you need both to see the full picture.

Which one gets prepared first

Accountants usually build the income statement before the balance sheet. That’s because net income, the final figure on the income statement, flows directly into the equity section of the balance sheet as retained earnings. You can’t finish the balance sheet without that number.

This isn’t a strict rule every company follows in the same order, but it’s the standard sequence in the accounting cycle: income statement, then balance sheet, then cash flow statement.

How the two statements connect

The balance sheet and income statement aren’t separate reports that happen to sit next to each other. They’re linked.

When the income statement closes out a period, its net income figure becomes part of the balance sheet’s equity section. If the company made $50,000 in profit and didn’t pay any of it out as dividends, that $50,000 shows up as an addition to retained earnings on the next balance sheet. Losses work the same way in reverse, shrinking equity.

This is why a business can’t judge its health from either statement alone. A strong income statement with rising profit doesn’t matter much if the balance sheet shows the company can’t cover its short-term debts. And a strong balance sheet built years ago doesn’t tell you if the business is still profitable today.

Which statement matters more for your decision

The honest answer is that it depends on what you’re trying to figure out.

If you’re applying for a business loan, the lender wants your balance sheet first. It shows them your assets, your existing debt load, and whether you have the equity cushion to handle a new loan without becoming over-leveraged.

If you’re pitching investors, they’ll want to see both, but the income statement usually gets more attention early on because it shows growth and whether the business model actually generates profit.

If you’re deciding whether to expand, hire, or cut costs, the income statement is your working document. It tells you where the money is going and whether your margins can absorb a new hire or a rent increase.

If you’re preparing for an audit, a funding round, or a sale, both statements need to be clean, consistent, and reconciled with each other. This is usually where a fractional CFO earns their keep: making sure the two statements tell a coherent story rather than contradicting each other, and building the financial models that project both forward.

Common mistakes business owners make reading these statements

A few patterns show up often enough to be worth naming directly.

Owners sometimes treat net income as if it were cash in the bank. It isn’t. A sale on the income statement might still be sitting as unpaid accounts receivable on the balance sheet, meaning the cash hasn’t actually arrived yet.

Owners also sometimes look at a single balance sheet in isolation and assume a big asset number means the business is doing well, without checking what portion of those assets is financed by debt versus equity. A company with $2 million in assets and $1.9 million in liabilities is in a much shakier position than one with the same assets and half the debt.

And it’s easy to skip the connection between the two statements entirely, reviewing them as separate documents instead of checking that this quarter’s net income actually shows up correctly in the next balance sheet’s equity section. When it doesn’t reconcile, that’s usually a bookkeeping error worth chasing down before it compounds.

Frequently Asked Questions

What are the three main financial statements?

The balance sheet, the income statement, and the cash flow statement. Together they cover financial position, profitability, and the actual movement of cash.

Is a P&L the same as an income statement?

Yes. Profit and loss statement, P&L, and income statement all refer to the same document.

Which comes first, the balance sheet or the income statement?

The income statement is typically prepared first, since its net income figure is needed to complete the equity section of the balance sheet.

Can a company be profitable on its income statement but still fail?

Yes, and it happens more often than people expect. A business can report a profit while its balance sheet shows dangerously low cash or unmanageable short-term debt. Profit on paper doesn’t guarantee the cash to pay bills on time.

Do small businesses need a formal balance sheet if they’re not seeking a loan?

Yes. Even without a lender asking for one, a balance sheet is the clearest way to track whether the business is building equity or slowly accumulating debt it can’t service.

How often should a business update its balance sheet and income statement?

Most businesses prepare income statements monthly and update balance sheets on the same schedule, though some smaller businesses stretch this to quarterly. More frequent updates catch problems earlier.

Conclusion

A balance sheet and an income statement aren’t competing reports where you pick the more useful one. They’re two views of the same business, one static and one moving, and misreading either in isolation is how businesses miss warning signs until it’s too late.

If you want a second set of eyes on what your statements are actually telling you, or you need proforma balance sheets built out for a funding round or a bank application, Oak Business Consultant’s fractional CFO services are built for exactly this. We also handle business valuations and day-to-day bookkeeping for businesses that want their statements reconciled correctly the first time. Book a call and we’ll walk through your numbers together.

{kind=link}