What is Budgeting Financial Management and How to Do it?

Budgeting Financial Management

Most businesses don’t fail because of bad products. They fail because they run out of money at the wrong time, or spend it on the wrong things without realizing it until it’s too late.

Budgeting financial management is the discipline that prevents that. It’s not glamorous. It’s not the part of running a business that anyone brags about at dinner. But it is the difference between companies that scale and companies that quietly shut down.

This guide covers everything, from the basics of what budgeting financial management actually means, to advanced methods, common traps, and how to use modern tools (including AI) to make the whole process less painful. Whether you’re a founder managing your first $500K in revenue or a CFO overseeing a $50M operation, there’s something here that will sharpen how you think about money.

What Is Budgeting Financial Management?

Budgeting financial management is the process of planning, monitoring, and controlling how money moves through your business over a set period — usually a month, quarter, or year.

At its core, it answers three questions:

- Where is money coming from? (revenue sources, investments, loans)

- Where is it going? (expenses, salaries, operations, growth)

- Is the plan aligned with your goals? (are you spending in ways that actually move the needle?)

The word “budgeting” tends to make people think of restriction — spending less, cutting costs, tightening belts. That’s a partial view. Good budgeting financial management is equally about allocating resources toward the things that generate the most return, not just reducing what goes out.

A well-managed budget gives a business three things:

Clarity — You know exactly where you stand financially at any point in time, not just at the end of the quarter when it’s too late to course-correct.

Control — You make deliberate decisions about money rather than reacting to whatever’s in the bank account.

Confidence — You can take smart risks, invest in growth, and handle unexpected expenses without panic, because you’ve planned for them.

Budget vs. Financial Forecast vs. Financial Plan — What’s the Difference?

These three terms get used interchangeably, and they shouldn’t. Here’s how they actually differ:

| Budget | Financial Forecast | Financial Plan | |

| Purpose | Set spending and revenue targets | Predict future financial outcomes | Define long-term financial direction |

| Time Horizon | Usually 1 year | 3 months to 2 years | 3–10 years |

| Nature | Fixed (approved targets) | Dynamic (updated regularly) | Strategic (big-picture) |

| Who Uses It | Operations, department heads | CFO, investors, leadership | Board, founders, investors |

| Frequency of Updates | Annual (sometimes quarterly) | Monthly or quarterly | Annual or as strategy shifts |

| Answers | “What should we spend?” | “What will happen if we stay on this path?” | “Where do we want to be financially in 5 years?” |

Think of it this way: the financial plan sets the destination. The budget maps the road for this year. The forecast tells you whether you’re actually on track, or veering off course.

A company that only has a budget but no forecast is flying partially blind. A company with all three, properly maintained, has a serious financial edge over most competitors.

Why Budgeting Actually Matters (Beyond the Obvious)

Most guides will tell you budgeting matters because it “controls spending” and “helps reach goals.” True, but incomplete. Here’s what budgeting actually does inside a business that few people talk about:

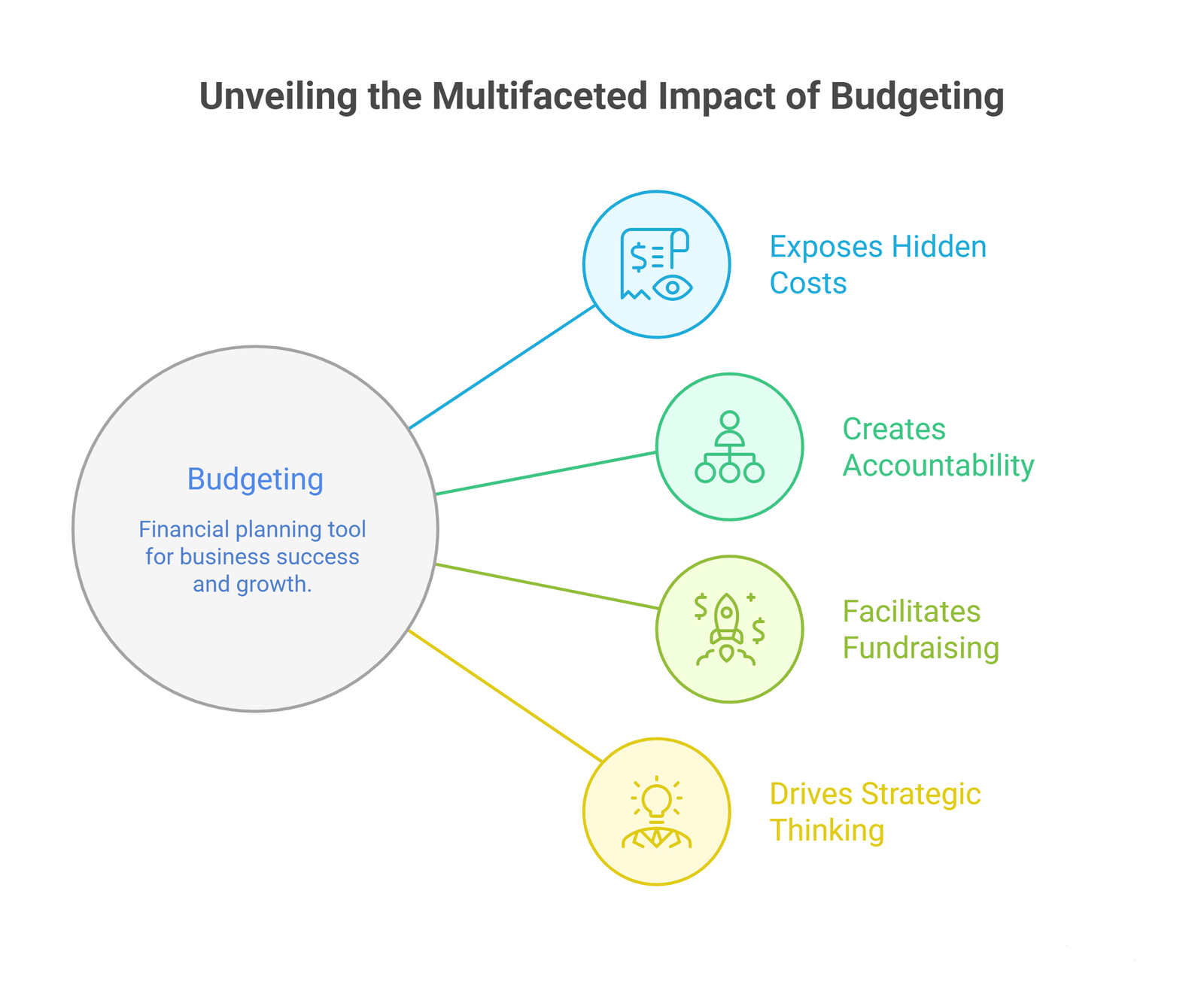

It Exposes Hidden Costs Before They Become Problems

Untracked expenses have a way of compounding. A $500/month SaaS subscription here, an overstaffed department there, vendor contracts that renewed automatically without review — none of these feel significant on their own. A real budgeting process forces you to see them all together, and the total is almost always a surprise.

It Creates Accountability Without Micromanagement

When every department head has a budget they own, you no longer need to approve every purchase decision yourself. They make calls within their allocation. You review results, not individual transactions. This is how finance scales with a company.

It Makes Fundraising Conversations Much Easier

If you’re talking to investors or lenders, your budget — and how accurately you’ve stuck to it historically — is one of the first things they look at. A business that can show it projected $2M in revenue, hit $1.95M, and explain the $50K variance with data is a business that earns trust fast.

It Forces Strategic Thinking

The process of building a budget requires you to make decisions: which markets to prioritize, which hires to make, which projects to fund. Companies that skip budgeting often skip that thinking too — and it shows.

Setting Financial Goals That Actually Work

Before you write a single number in a budget, you need to know what you’re actually trying to achieve. Vague goals produce vague budgets.

The common advice is to make goals “SMART” — Specific, Measurable, Achievable, Relevant, Time-bound. That’s fine as far as it goes, but in practice, the more important skill is connecting financial goals to business reality.

Here are a few things that make the difference between goals that drive behavior and goals that collect dust:

Tie goals to specific decisions. “Grow revenue by 25%” is a goal. “Grow revenue by 25% by adding two new enterprise accounts per quarter, which requires hiring one additional sales rep in Q1” is a goal that actually changes what you budget.

Set targets at multiple levels. Company-level, department-level, and individual-level goals should cascade from each other. When they don’t, departments optimize for their own metrics while the company misses its targets.

Build in variance tolerance. A goal with no room for reality is just pressure. Most experienced CFOs budget a variance of 5–10% and flag anything outside that range for review — not panic, review.

Review them quarterly, not just annually. A goal set in January based on assumptions that no longer apply by April isn’t helping anyone.

Types of Financial Goals

Short-Term Financial Goals (0–12 Months)

Short-term goals are where day-to-day operations connect to financial performance. These typically include:

- Hitting monthly or quarterly revenue targets

- Reducing a specific expense category by a set percentage

- Achieving positive cash flow by a certain date

- Collecting outstanding receivables within a defined period

- Building a cash reserve equal to 2–3 months of operating expenses

Short-term goals are the most measurable and the most immediately correctable. If you miss a monthly target, you know it quickly enough to adjust.

Medium-Term Financial Goals (1–3 Years)

Medium-term goals bridge daily operations and long-term strategy. They often involve investments that take time to pay off:

- Expanding into a new market or product line

- Upgrading technology infrastructure to reduce operational costs

- Growing a specific revenue stream (e.g., subscription revenue) from 20% to 40% of total income

- Reaching a certain headcount while keeping payroll below a specific percentage of revenue

- Achieving a defined profit margin

These goals require quarterly budget reviews to stay on track, because circumstances change more over two years than over two months.

Long-Term Financial Goals (3–10 Years)

Long-term goals are where vision and finance meet. Examples:

- Achieving a 3x return on a major capital investment

- Building the company to a specific revenue threshold for acquisition or IPO readiness

- Establishing a company-owned asset base (property, equipment, intellectual property)

- Reducing dependence on a single revenue source to below 30% of total income

Long-term goals shape how you structure today’s budget — whether you prioritize margin now, or reinvest aggressively for future scale.

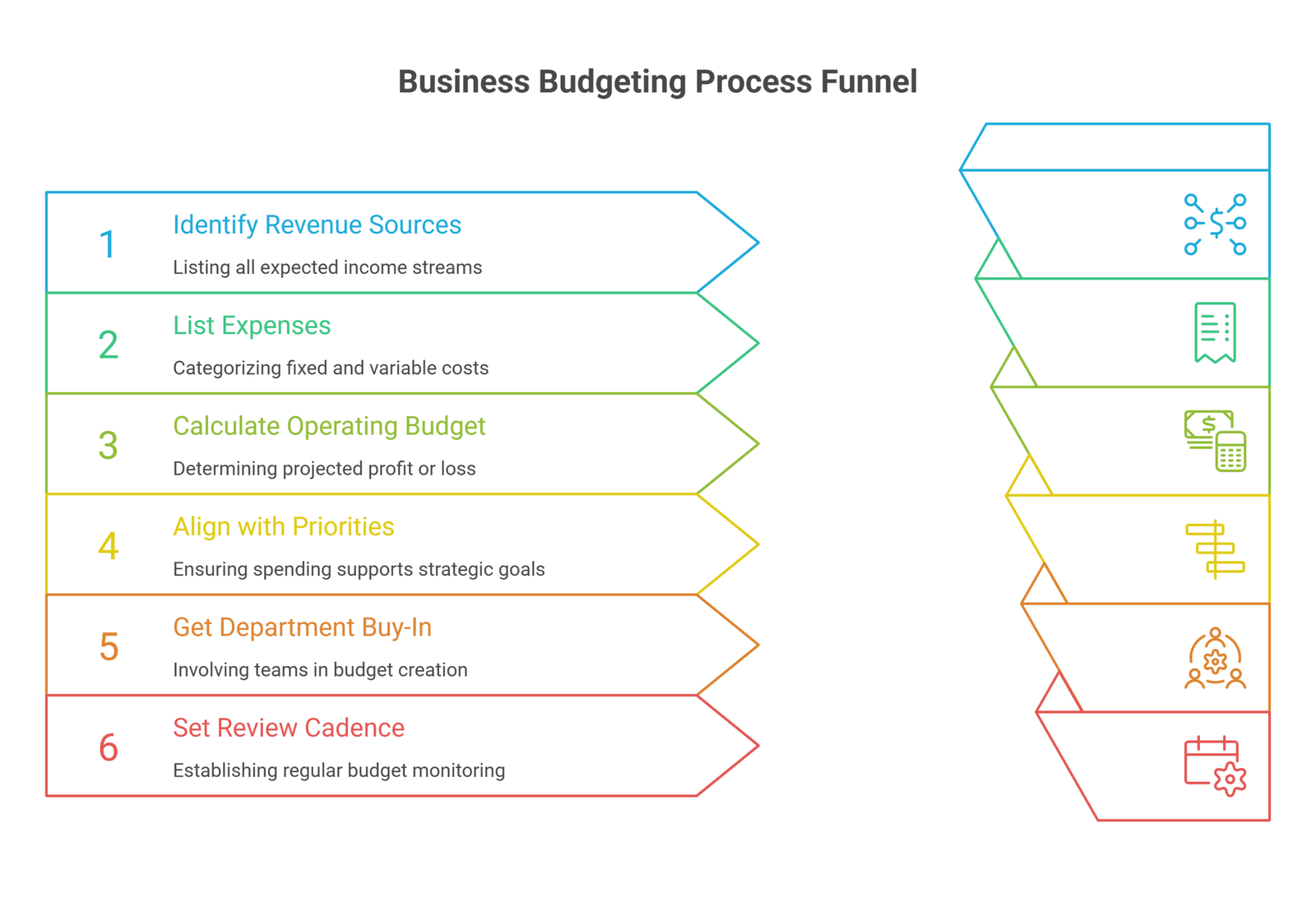

How to Create a Business Budget — Step by Step

Step 1: Gather Historical Data

If your business has been operating for at least a year, start with what actually happened — not what you planned. Pull revenue figures, expense reports, payroll data, and cash flow statements from the past 12–24 months.

Look for patterns: revenue peaks and troughs by season, expense spikes around certain periods, departments that consistently over- or under-spend. This is your baseline.

If you’re pre-revenue or early stage, use industry benchmarks, comparable companies, and your best-researched assumptions — and label them clearly as estimates.

Step 2: Identify All Revenue Sources

List every stream of income the business expects to generate, including:

- Product or service sales

- Subscription or recurring revenue

- Licensing or royalties

- Grants or funding rounds

- Investment income

- Any other sources (consulting, partnerships, etc.)

For each source, project realistic numbers based on your pipeline, historical growth rate, and market conditions. Be honest. Optimistic revenue projections are one of the most common and most damaging budgeting mistakes.

Step 3: List All Expenses — Fixed and Variable

Fixed expenses stay the same regardless of how much you sell: rent, salaries, software subscriptions, insurance, loan repayments.

Variable expenses change based on activity: cost of goods sold, shipping, commissions, advertising spend, freelancer costs.

Also plan for:

- One-time expenses: Equipment purchases, office build-outs, software migrations

- Semi-variable expenses: Utilities, travel, maintenance — which have a fixed base but scale somewhat with activity

- Contingency buffer: Most experienced operators budget 5–15% on top of projected expenses for the unexpected

Step 4: Calculate Your Operating Budget

Operating budget = total projected revenue − total projected expenses

If you’re projecting a loss, the question is whether that’s intentional (investing in growth) or a problem to fix before you start. Either answer is fine — but you should know which it is.

Step 5: Align Budget With Strategic Priorities

This is the step most businesses skip, and it’s where the most value gets left on the table. Go through your budget line by line and ask: does this spending support our actual goals for this year?

You’ll often find money going toward things that made sense 18 months ago but don’t serve the current direction. Reallocating even 10–15% of a budget toward higher-priority areas can significantly change outcomes.

Step 6: Get Department Buy-In

A budget built in a finance silo and handed down to department heads is a budget that will be resisted, worked around, and ultimately ignored. Involve department leads early. Let them flag unrealistic assumptions. The goal is a budget that operations teams feel ownership over, not just accountability for.

Step 7: Set a Review Cadence

Budget reviews should happen monthly at minimum, quarterly for deeper analysis. Each review should cover:

- Actual vs. budgeted performance (revenue and expenses)

- Variance explanations for anything outside tolerance

- Adjustments for the next period based on new information

- Flagging anything that needs leadership decisions

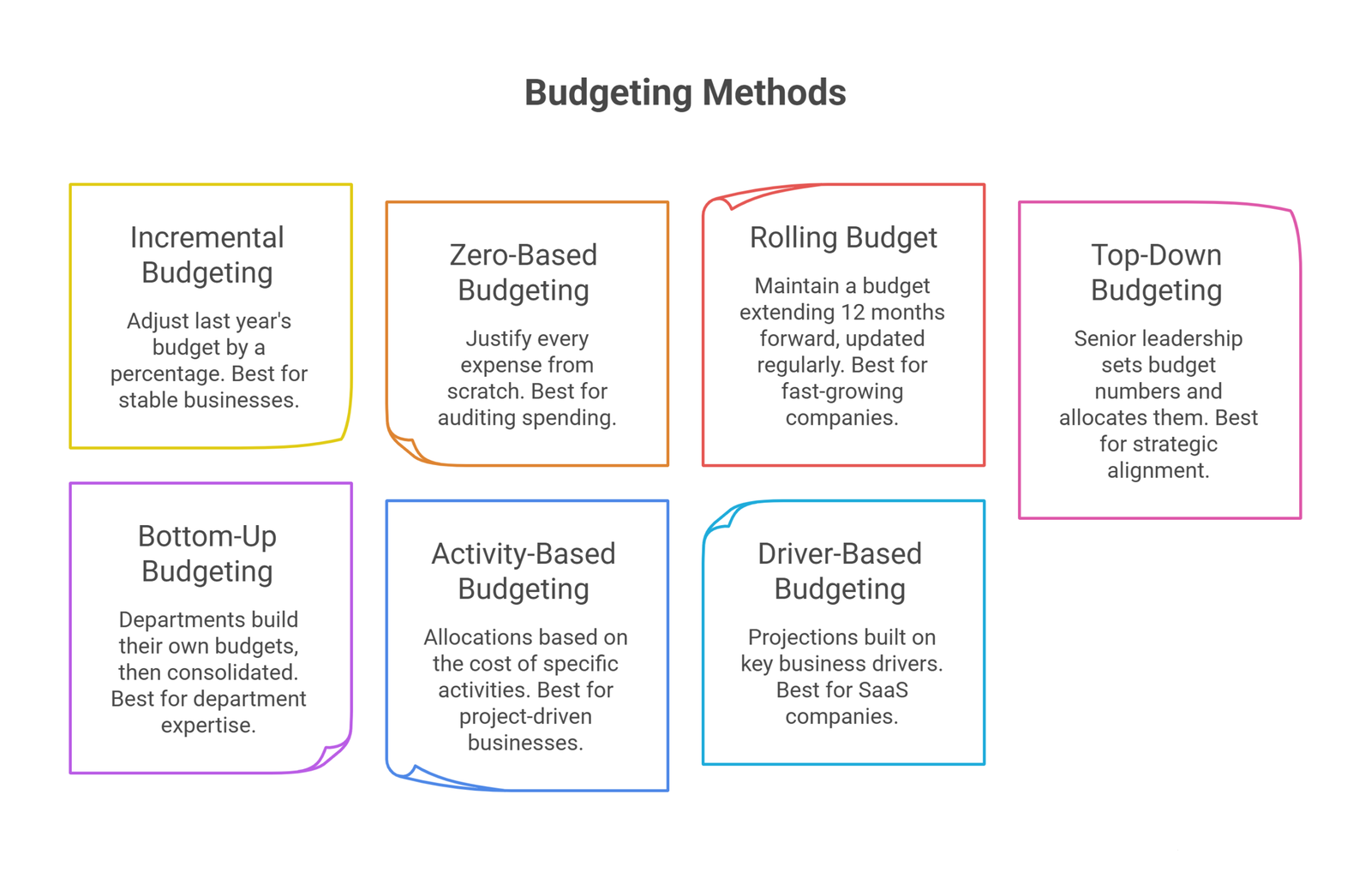

7 Budgeting Methods Explained

There isn’t one right budgeting method. The right one depends on your company’s size, stage, industry, and how dynamic your environment is. Here’s an honest breakdown of the seven most used approaches:

1. Incremental Budgeting

What it is: Take last year’s budget and adjust each line up or down by a percentage.

Best for: Stable, predictable businesses with consistent operations.

Honest drawbacks: It assumes last year’s spending was efficient — often it wasn’t. Inefficiencies get locked in year after year. Bad legacy expenses survive because no one questions them.

When to avoid it: High-growth companies, startups, or any business going through significant change.

2. Zero-Based Budgeting (ZBB)

What it is: Every expense must be justified from scratch each budget cycle. Nothing carries over automatically.

Best for: Companies that want to seriously audit spending and eliminate inefficiency. Works well for large organizations with bloated cost structures.

Honest drawbacks: Time-intensive. Requires significant effort from every department. Can create budget gaming, where managers over-request because they know everything gets cut.

When to avoid it: Small teams without the bandwidth for full justification exercises every year.

3. Rolling Budget (Continuous Budgeting)

What it is: Rather than setting a fixed annual budget, you maintain a budget that extends 12 months forward, updated each month or quarter.

Best for: Fast-growing companies or businesses in volatile markets where a fixed annual budget becomes obsolete quickly.

Honest drawbacks: Requires more frequent management attention. Can become a burden if not supported by the right tools.

When to use it: If you’ve ever reached June and realized your January budget assumptions are so outdated they’re actively misleading — this is the method for you.

4. Top-Down Budgeting

What it is: Senior leadership sets the overall budget numbers and allocates them down to departments.

Best for: Organizations where strategic alignment is a priority, or where leadership has strong insight into what each department needs.

Honest drawbacks: Department heads often feel disconnected from targets they had no input on. This can reduce accountability and motivation.

5. Bottom-Up Budgeting

What it is: Each department builds its own budget based on its actual needs and plans, which are then consolidated into a company-level budget.

Best for: Companies where department heads have the best information about what resources they actually need.

Honest drawbacks: Can result in bloated budgets if departments over-request to create padding. Requires careful consolidation and negotiation.

6. Activity-Based Budgeting (ABB)

What it is: Budget allocations are based on the cost of specific activities needed to achieve goals — not on departments or historical spending.

Best for: Project-driven businesses, professional services, manufacturing — anywhere the cost structure is activity-dependent.

Honest drawbacks: Complex to set up. Requires detailed tracking of activities and their associated costs.

7. Driver-Based Budgeting

What it is: Budget projections are built on key business drivers — metrics like units sold, number of customers, website traffic, or headcount — rather than on line-item expenses.

Best for: SaaS companies, subscription businesses, any business where a handful of metrics drive most of the financial outcomes.

Example: If you know that every new customer costs $200 to acquire, generates $50/month in revenue, and stays for an average of 18 months, you can build an entire budget from those three numbers.

Why it’s gaining popularity: It creates a direct, visible link between operational decisions and financial outcomes. When drivers change, the budget updates logically rather than requiring a full rebuild.

Budgeting by Business Type

Generic budgeting advice often breaks down when you apply it to a specific type of business. Here’s how the approach shifts:

Startups (Pre-Revenue to Series A)

Cash runway is everything. Your budget’s primary job is to make sure you don’t run out of money before you reach the next milestone — revenue, fundraising, or profitability.

Key focus areas:

- Burn rate (how much cash you spend per month)

- Runway (how many months you have before cash runs out)

- Product-market fit spending vs. operational overhead — keep the latter as lean as possible

- Scenario planning: what does the budget look like if revenue takes 6 months longer than expected?

Most early-stage founders underestimate time-to-revenue. Build in a longer runway than you think you need.

SaaS Companies

The key metrics that should drive a SaaS budget are Monthly Recurring Revenue (MRR), Customer Acquisition Cost (CAC), Customer Lifetime Value (LTV), and churn rate.

A healthy SaaS company typically targets:

- LTV:CAC ratio of at least 3:1

- CAC payback period under 18 months

- Gross margin above 70%

Budget conversations should always connect back to these ratios. If you’re planning to increase marketing spend, the question isn’t just “how much?” — it’s “what CAC does this produce, and does the LTV justify it?”

Retail Businesses

Seasonal cash flow management is the core budgeting challenge. Revenue may be heavily concentrated in Q4, while costs are more evenly distributed.

Key considerations:

- Inventory financing and timing

- Seasonal staffing costs

- Marketing spend aligned to peak demand periods

- Cash reserve strategy for low-season months

Professional Services / Consulting

The main variable is billable utilization — what percentage of available hours are actually billed to clients. A firm budgeting 100% utilization is setting itself up to fail; 70–80% is a more realistic target.

Budget considerations:

- Revenue per consultant

- Overhead cost per billable hour

- Non-billable time (business development, admin, training)

- Accounts receivable management — late-paying clients can destroy cash flow even when revenue is strong

Small and Medium Businesses (SMEs)

The most common gap in SME budgeting is owner compensation. Many small business owners don’t pay themselves a market-rate salary, which distorts profitability figures. Build in proper owner compensation and you’ll get a much more honest picture of whether the business is actually making money.

Also, don’t skip building a cash reserve. The standard recommendation is 3–6 months of operating expenses. Most SMEs have far less — which is why one slow quarter can become a crisis.

Tracking Income and Expenses — The Right Way

Tracking isn’t just bookkeeping. Done well, it gives you a live picture of financial health and early warning when something is going sideways.

Build a Tracking Framework

The foundation is a proper chart of accounts — a categorized list of every type of income and expense in your business. Categories should be specific enough to be useful but not so granular that they create reporting noise.

A useful expense structure might include:

- Cost of Goods Sold / Cost of Revenue

- Personnel (broken out by department if possible)

- Marketing and Sales

- Technology and Software

- Facilities and Overhead

- Professional Fees

- Financing Costs

- Other Operating Expenses

Every transaction should be consistently categorized so that your reports mean the same thing month after month.

Record Transactions Promptly

The longer a transaction waits to be recorded, the more likely it is to get miscategorized, lost, or forgotten. Same-day or next-day recording is the goal. For businesses with higher transaction volumes, automated bank feeds (available in most modern accounting software) handle most of this automatically.

Review Weekly, Analyze Monthly

A weekly 15-minute check of outstanding invoices, account balances, and major transactions catches problems early. Monthly, do a proper reconciliation and compare actuals to budget. Quarterly, do a full budget review with leadership.

Tools Worth Using

- QuickBooks Online / Xero — the most widely used small-to-mid-size business accounting platforms. Both handle invoicing, expense tracking, payroll integration, and financial reporting.

- FreshBooks — simpler, often preferred by service businesses and freelancers

- NetSuite — for larger organizations that need deeper financial controls and multi-entity support

- Fathom / Spotlight Reporting — analytics layers on top of your accounting software that make budgeting and variance analysis much cleaner

- Mosaic / Pigment / Jirav — FP&A platforms built specifically for financial planning, forecasting, and scenario modeling

How AI Is Changing Financial Management

AI-powered tools are genuinely shifting what’s possible in financial management — not by replacing CFOs or financial analysts, but by automating the mechanical parts so that humans can focus on judgment and strategy.

Here’s where AI is making the most practical difference right now:

Automated Expense Categorization

Tools like Expensify, Ramp, and Brex use machine learning to automatically categorize transactions, flag potential duplicates, and surface unusual spend patterns. What used to take a bookkeeper hours per week now happens in near real-time.

Cash Flow Forecasting

AI forecasting tools can analyze historical cash flow patterns, accounts receivable aging, and sales pipeline data to generate rolling cash flow projections with higher accuracy than manual forecasting. Platforms like Float, Cashflow Fathom, and Pulse offer this for small businesses; larger organizations use tools like Anaplan or Planful.

Variance Analysis at Scale

When you have dozens of cost centers and hundreds of budget lines, manually analyzing variance is exhausting. AI tools can flag the variances that matter — the ones statistically likely to indicate a real trend rather than just noise — and explain the likely drivers.

Scenario Modeling

Traditionally, building scenario models (best case, worst case, base case) was time-consuming because changing one assumption required manually updating dozens of connected cells. Modern FP&A tools with AI-assisted modeling let you change a single driver and see cascading impacts across the full financial model instantly.

What AI Doesn’t Replace

Context. A tool can tell you that marketing spend is up 40% versus budget. It can’t tell you whether that’s justified because you just landed a major enterprise client and accelerated Q3 campaigns on purpose — or whether it’s a sign that the team is overspending. The judgment behind the numbers still requires humans.

8 Most Common Budgeting Mistakes

1. Revenue Optimism

Over-projecting revenue is the single most common budgeting mistake. It creates a cascade of problems — over-hiring, over-spending, insufficient cash reserves, and eventually, a scramble to cut costs that could have been avoided.

Build your budget on conservative revenue assumptions. Run a more optimistic version as a scenario, not as your operating plan.

2. Forgetting One-Time Expenses

Annual subscriptions that renew in Q2. Equipment that needs replacing. Software migrations. Conference sponsorships. These items are easy to omit from a budget because they feel exceptional — but most businesses have several of them every year. Build a category for anticipated one-time expenses and review it against last year’s actuals.

3. Treating the Budget as Static

A budget built on January assumptions that nobody revisits until December isn’t a financial management tool — it’s a historical document. Markets shift, hiring plans change, revenue timelines move. Your budget should be a living reference, not a filed report.

4. Underestimating Personnel Costs

Salaries are straightforward. But total compensation includes payroll taxes, benefits, bonuses, recruiting costs, training, and equipment. Underestimating these by even 15–20% across a team of 20 people can represent hundreds of thousands of dollars in unplanned expense.

5. No Contingency Buffer

The standard advice is to build in 5–15% of total operating expenses as a contingency. Most businesses don’t do this, and most businesses have at least one significant unexpected expense per year. The two facts are related.

6. Siloed Budget Conversations

When finance builds the budget and hands it to operations, operations often doesn’t feel ownership over it. When there’s no cross-functional input, critical information doesn’t make it into the numbers — and the budget ends up not reflecting how the business actually works.

7. Confusing Cash Flow With Profit

A business can be profitable on paper and still run out of cash. If customers pay 60–90 days after invoicing but you pay suppliers in 30 days, there’s a structural cash flow gap that doesn’t appear in a profit and loss statement. Cash flow forecasting and profitability analysis are separate exercises — both are necessary.

8. No Accountability Structure

A budget without ownership is just a spreadsheet. Every line in the budget should have someone accountable for it. Budget owners should know their numbers, understand what drives them, and have the authority to make decisions within their allocation.

How to Stick to a Budget Without Micromanaging Everyone

The common assumption is that sticking to a budget requires constant oversight — tracking every purchase, approving every expense. That’s not management; that’s distrust. It also doesn’t scale.

Here’s what actually works:

Give People Budget Ownership, Not Just Budget Limits

There’s a real difference between telling a department head “you have $80K for the quarter” and involving them in building that $80K figure, explaining the reasoning, and letting them own how it gets spent. The second approach produces more disciplined spending because the person making decisions has context and ownership rather than just a constraint.

Review Variance, Not Transactions

Your job as a financial manager isn’t to review individual expense reports. It’s to review variances — where actual spending or revenue diverges from the plan — and understand why. A 5% variance in one direction with a clear explanation is fine. A 5% variance with no explanation is worth investigating.

Create Clear Escalation Thresholds

Define in advance what requires approval versus what falls within a manager’s discretion. For example: anything within budget allocation and under $5,000 needs no approval; anything over $5,000 or outside budget requires finance sign-off. This removes friction for normal decisions while maintaining controls for significant ones.

Use Monthly Financials as a Conversation, Not a Report Card

Monthly budget reviews work best as forward-looking conversations: “Given where we are through month 5, what do we need to adjust for months 6 through 12?” Companies that use financial reviews primarily to assign blame end up with departments that hide problems until they can’t be hidden anymore.

Reward Accurate Forecasting, Not Just Favorable Variances

Being exactly on budget is not the highest possible standard. Coming in dramatically under budget because you spent conservatively when you should have been investing — that’s also a failure mode. Reward teams that forecast accurately and make good decisions with their allocations, not just teams that spend less.

Free Budget Template — What to Include

A usable business budget template should have at minimum:

Revenue Section

- Revenue by product/service line or channel

- Prior year actual, current year budget, current year forecast

- Variance columns ($ and %) for actual vs. budget

Cost of Revenue

- Direct costs tied to delivering products or services

- Gross margin calculation

Operating Expenses (by department or category)

- Personnel (salaries, benefits, payroll taxes)

- Marketing and advertising

- Technology and software

- Facilities

- Travel and entertainment

- Professional services (legal, accounting, consulting)

- Depreciation/amortization

- Other operating

Cash Flow Summary

- Operating cash flow

- Capital expenditures

- Net cash change

- Opening and closing cash balance

Summary Dashboard

- Revenue vs. budget

- Gross margin %

- Operating expenses vs. budget

- EBITDA

- Cash runway (months)

The format matters less than the discipline of using it. A simple spreadsheet used consistently every month beats an elaborate model that gets opened twice a year.

Frequently Asked Questions

What is budgeting financial management?

It’s the process of planning, monitoring, and controlling how money flows through your business over a set period — answering where money comes from, where it goes, and whether spending aligns with your goals.

What’s the difference between a budget, a forecast, and a financial plan?

A budget sets spending/revenue targets for the year. A forecast predicts whether you’re on track. A financial plan defines your 3–10 year direction. They work together — plan sets the destination, budget maps the route, forecast checks if you’re on it.

Which budgeting method is best for my business?

It depends on your stage. Startups and fast-growing companies benefit from rolling or driver-based budgeting. Stable businesses can use incremental. Companies with bloated costs should consider zero-based budgeting.

How often should I review my budget?

At minimum, monthly for actuals vs. budget checks, and quarterly for deeper analysis and forward-looking adjustments.

What’s the most common budgeting mistake?

Over-projecting revenue. It triggers over-hiring, overspending, and cash shortfalls. Always budget conservatively on revenue and run optimistic numbers as a separate scenario.

Final Thoughts

Budgeting financial management is one of those things that feels administrative until it saves your business — or until the lack of it sinks it.

The companies that handle money well don’t necessarily have the most sophisticated tools or the largest finance teams. They have clarity about their numbers, discipline in reviewing them regularly, and the judgment to make decisions based on reality rather than optimism.

Start where you are. If you don’t have a budget at all, build a simple one this week. Additionay, if you have one but never look at it, schedule monthly reviews starting now. If your reviews are happening but not driving decisions, look at how financial information is being shared with the people who need to act on it.

The mechanics of budgeting are learnable. The harder part — building a culture where financial discipline is part of how a company operates, not an afterthought — takes time, but it starts with the same first step: knowing your numbers.

Building a culture of financial discipline doesn’t mean you have to figure it out alone. If you are ready to move past guesswork and start making data-driven decisions that scale your business, we can help. Partner with Oak Business Consultant today. Our expert CFO Services provide the strategic clarity, robust budgeting frameworks, and ongoing financial leadership your business needs to thrive. Contact us now to schedule a free consultation.