Difference between Operating and Capital Budgets – A Comprehensive Guide

Introduction: Why Getting Your Budgets Right Has Never Mattered More

Most businesses that struggle financially do not struggle because their products fail or their markets disappear. They struggle because their financial planning is blurry. Specifically, they treat all spending as one undifferentiated mass, when in reality every dollar a business spends falls into one of two very different categories: it either keeps the business running today, or it builds the business for tomorrow.

That is the core distinction between an operating budget and a capital budget. Understanding it clearly is not an accounting technicality. It is a foundational management skill. It affects how you report profits, how you pay taxes, how you pitch to lenders, how you measure performance, and how you make strategic decisions about growth.

The One Big Beautiful Bill Act restored 100 percent bonus depreciation for many fixed assets and raised the Section 179 expensing limit to $2.5 million. That means capital planning decisions now carry bigger and more immediate tax consequences than at any point in recent years. Businesses that understand the difference between their two budgets are positioned to capture those benefits. Those that lump everything together will miss them.

This guide covers both budget types in full depth: what they are, what goes in them, how to build them, how they interact, and how to use them together as an integrated tool for financial strategy.

Part 1: The Operating Budget

What Is an Operating Budget?

An operating budget is a detailed financial plan covering all the revenues and expenses associated with running a business during a defined period, almost always one fiscal year. It captures the recurring, day-to-day financial activity of the organization: the money coming in from sales and services, and the money going out to keep operations running.

Think of the operating budget as the financial heartbeat of the business. It does not concern itself with major asset purchases, facility expansions, or long-range capital projects. It is purely about what the business does every day to serve its customers, pay its people, and maintain its operations.

Every department in a business contributes to and is governed by the operating budget: sales, marketing, human resources, IT, administration, and customer service all have their costs captured here. Revenue projections anchor the plan, and expense categories define how resources will be deployed in pursuit of those projections.

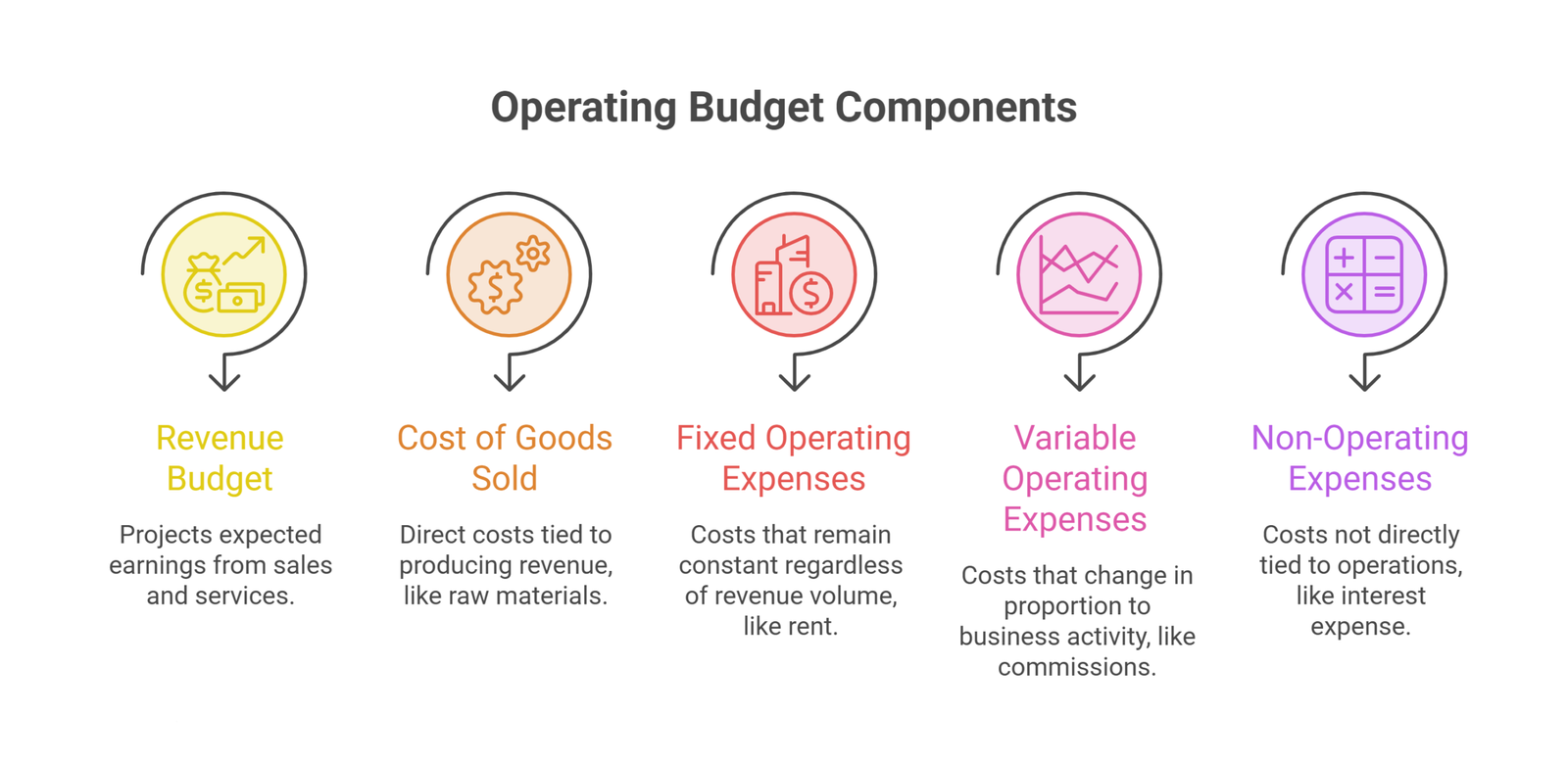

Components of an Operating Budget

A well-constructed operating budget typically contains five core components:

1. Revenue Budget

The revenue budget projects how much money the business expects to earn during the period. It is built from sales volume forecasts multiplied by expected pricing, adjusted for seasonality, competitive dynamics, historical trends, and strategic growth initiatives. The revenue budget is the foundation everything else is built on: underestimate it and you will over-restrict spending; overestimate it and you will over-commit resources.

Inputs to a rigorous revenue budget include prior-period income statements, market trend data, sales pipeline analysis, known contract renewals, and management assumptions about new customer acquisition rates. Each revenue stream should be projected separately before being consolidated.

2. Cost of Goods Sold (COGS)

COGS captures the direct costs tied to producing the revenue. For a manufacturer, this means raw materials, direct labor, and production overhead. For a software company, it might include hosting costs, customer success labor, and third-party license fees directly attributable to revenue delivery. COGS is separated from operating expenses because it is the primary driver of gross margin, which tells you how efficient the core business model is before accounting for overhead.

3. Fixed Operating Expenses

Fixed expenses remain constant regardless of revenue volume. Rent or lease payments, base salaries, insurance premiums, software subscriptions, and professional retainer fees are all fixed. These expenses are predictable and relatively easy to budget. They represent the minimum cost floor the business must cover before generating any profit, which is why understanding fixed costs is essential to break-even analysis.

4. Variable Operating Expenses

Variable expenses change in proportion to business activity. Commissioned sales compensation, marketing spend tied to campaign volume, shipping and logistics costs, and hourly labor costs for production workers are all examples. Variable costs provide the operating budget with flexibility: if revenue falls short, variable costs can often be reduced to partially protect margins. Building accurate variable cost ratios requires historical data on cost-per-unit or cost-as-a-percentage-of-revenue across each category.

5. Non-Operating Expenses and Adjustments

Some costs affect the income statement without being directly tied to operations, including interest expense on debt, one-time charges, and tax provisions. While these are not strictly operating items, they need to be reflected in a complete operating budget to present a true picture of net income.

A Practical Example

A regional accounting firm budgets for the year ahead. On the revenue side, it projects billings across its audit, tax, and advisory service lines based on contracted clients and expected new business. On the expense side, fixed costs include staff salaries, office rent, malpractice insurance, and accounting software licenses. Variable costs include contract staff fees during peak audit season and marketing spend that scales with the number of proposals the firm pursues. The firm’s finance team reviews prior years, adjusts for planned headcount changes and a known rent increase, and builds a month-by-month budget that shows exactly when cash will be tight (typically during the slow summer months) and when it will be flush (post-tax-season).

This is an operating budget in action: a granular, time-phased plan for managing the recurring financial life of the business.

How to Prepare an Operating Budget

Step 1: Anchor on historical performance. Pull the last two to three years of income statements. Identify which revenue lines grew, which shrank, and which expense categories ran over or under prior-year budgets. This data reveals the real cost structure of the business and exposes assumptions that did not hold up, which is exactly the kind of insight that prevents repeating expensive mistakes.

Step 2: Build the revenue forecast first. Start with what you know: signed contracts, subscription renewals, and committed purchase orders. Then layer on projected new business based on sales pipeline conversion rates and market conditions. Be explicit about assumptions. A revenue forecast that says “sales will grow 20 percent” is not a budget; it is a wish. A forecast that explains why growth will be 20 percent, based on three new salespeople starting in Q2 and two known enterprise contracts, is the beginning of a real plan.

Step 3: Map expenses to revenue drivers. Separate fixed from variable costs. For variable costs, establish a ratio to revenue or units and apply it consistently. For fixed costs, gather actual quotes or contract amounts wherever possible rather than estimating from memory.

Step 4: Build in a contingency reserve. A contingency of 5 to 10 percent of projected expenses is standard practice. Unexpected costs are not exceptional in business; they are routine. Budgets that do not reserve for them are structurally fragile.

Step 5: Review by department, then consolidate. Distribute draft budget assumptions to department heads for validation. Operational leaders know things finance teams do not: a planned software migration, a key supplier relationship at risk, a team that is understaffed for the pipeline. Collecting that input before finalizing the budget prevents expensive surprises mid-year.

Step 6: Compare against targets and iterate. Once consolidated, compare the draft budget to profitability and cash flow targets. If the plan produces a projected loss, identify specific levers to pull rather than applying arbitrary cuts. Targeted adjustments that preserve strategic investments while reducing discretionary spend will outperform across-the-board reductions in almost every scenario.

Part 2: The Capital Budget

What Is a Capital Budget?

A capital budget is a financial plan for major, long-term investments in assets or projects that will provide value to the business over multiple years. Where the operating budget manages the present, the capital budget shapes the future. It is where a company decides to build a new facility, acquire new machinery, invest in enterprise software, expand into a new geography, or make a strategic acquisition.

Capital budgets are governed by a fundamentally different logic than operating budgets. Because capital expenditures are large, infrequent, and have long payback periods, they require structured evaluation methods, explicit return calculations, and multi-year financial modeling. A capital spending decision made poorly can burden the business with debt and depreciation costs for a decade. A capital spending decision made well can compound shareholder value across the same time horizon.

Capital expenses are not expensed on the income statement in the year they are incurred the way operating costs are. Instead, they are capitalized on the balance sheet as assets and depreciated over their useful life. This accounting treatment, which follows Generally Accepted Accounting Principles (GAAP), means that a $500,000 equipment purchase does not create a $500,000 expense in year one; it creates a depreciation charge spread over five, ten, or more years depending on the asset class.

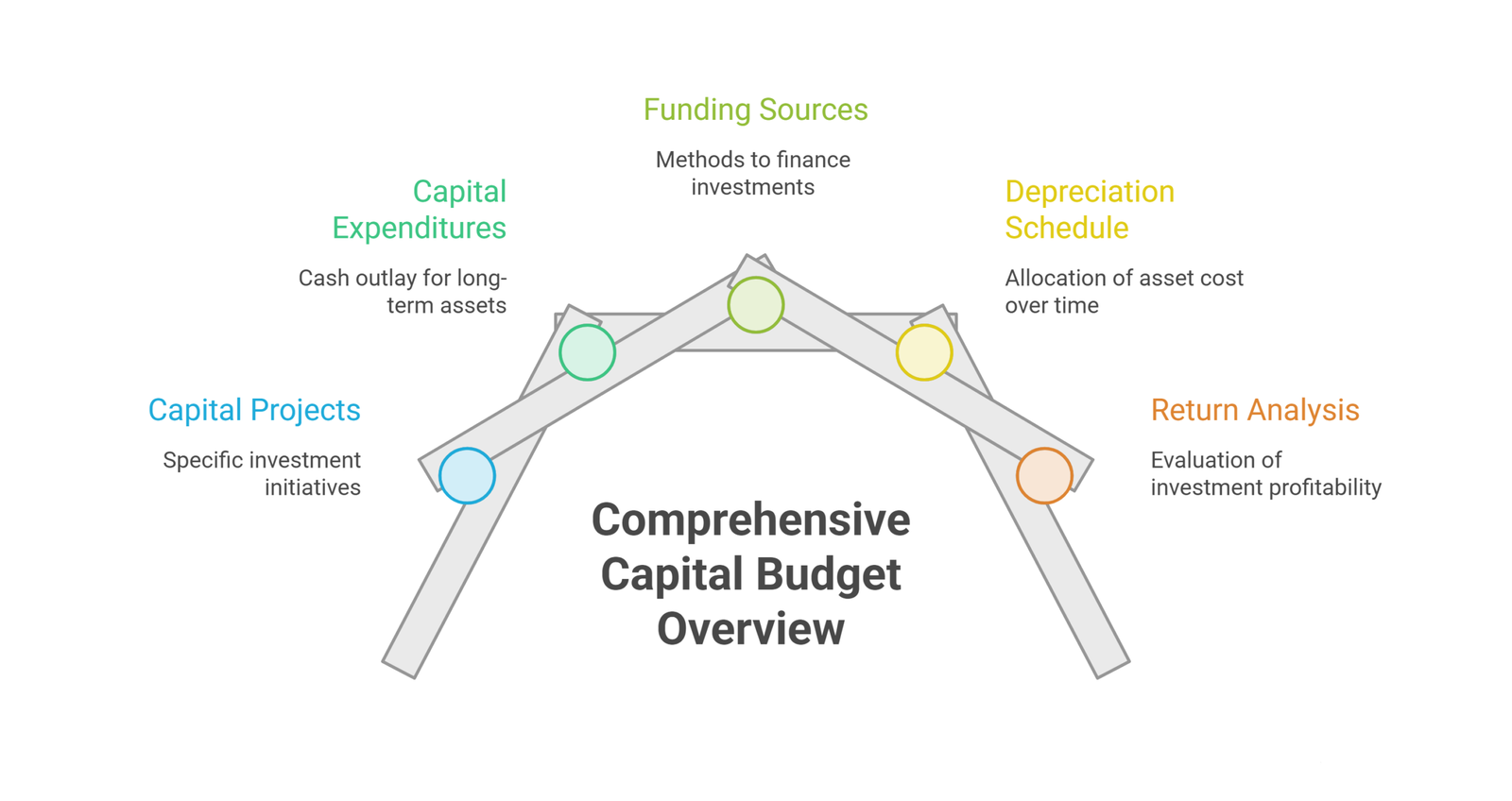

Components of a Capital Budget

1. Capital Projects

Capital projects are the specific investments under consideration. They may include physical assets like machinery, vehicles, buildings, and equipment; technology assets like enterprise resource planning (ERP) systems, manufacturing automation, or data center infrastructure; and strategic projects like market expansions, acquisitions, or significant research and development programs. Each project should be documented with a clear business case, cost estimate, expected useful life, and projected financial return.

2. Capital Expenditures (CapEx)

CapEx is the actual cash outlay to acquire or improve a long-term asset. It is distinguished from operating expenditure (OpEx) by the principle of future economic benefit: if an expense creates an asset that will generate value beyond the current year, it is a capital expenditure. Replacing a roof on a manufacturing facility extends the life of the asset and qualifies as CapEx. Routine HVAC servicing is maintenance and goes into the operating budget.

The distinction matters enormously in practice. Misclassifying a capital expenditure as an operating expense inflates operating costs and understates asset values. Misclassifying an operating expense as capital understates current-year costs and inflates profitability in the near term. Both errors distort the financial picture that management and investors rely on.

3. Funding Sources

Capital investments must be financed. Common sources include retained earnings (internal cash generation), bank loans and credit facilities, equipment financing and leasing arrangements, equity investment from owners or external investors, and government grants or incentive programs. The choice of funding source affects the cost of capital, the balance sheet structure, and the cash flow implications of the investment. A capital budget should explicitly document how each project will be funded and what the total cost of that funding is.

4. Depreciation Schedule

Because capital assets are depreciated over time, the capital budget must include a depreciation schedule that shows how each asset’s cost will be allocated across its useful life. This schedule feeds directly into the operating budget in future years, because depreciation is an operating expense even though the cash was spent at acquisition. Under the 2025 tax law changes, many businesses can elect 100 percent bonus depreciation for qualifying assets, creating an immediate tax deduction even as the book depreciation is spread over multiple years.

5. Return Analysis

Every capital investment should be evaluated using one or more return metrics before it is approved. The four most widely used techniques are:

- Net Present Value (NPV): Calculates the present value of all future cash flows generated by the investment, discounted at the company’s cost of capital, and subtracts the initial investment cost. A positive NPV means the project creates value; a negative NPV means it destroys value. NPV is the most theoretically rigorous method because it accounts for the time value of money and the risk profile of the investment.

- Internal Rate of Return (IRR): Calculates the discount rate at which the NPV of the investment equals zero. In plain terms, IRR is the annualized return the project is expected to generate. Projects with an IRR above the company’s hurdle rate (cost of capital) are accepted; projects below it are rejected or deprioritized.

- Payback Period: Calculates how many years it takes for the investment to recover its initial cost from generated cash flows. Payback period is simple to compute and easy to understand, but it ignores cash flows beyond the payback date and does not account for the time value of money. It is most useful as a secondary screen for liquidity risk rather than a primary investment decision tool.

- Profitability Index (PI): Calculated as the ratio of the present value of future cash flows to the initial investment. A PI above 1.0 indicates a value-creating investment. PI is particularly useful when comparing multiple projects competing for limited capital, as it normalizes returns across different investment sizes.

A Practical Example

A regional coffee roaster has grown significantly and its current roasting facility is at capacity. The ownership team is evaluating a $1.2 million investment in a larger facility and new roasting equipment. They prepare a capital budget that documents the full acquisition and buildout cost, projects the incremental revenue the larger capacity will enable, calculates the annual operating savings from more efficient equipment, builds a 10-year NPV model using a discount rate that reflects their cost of debt and equity, and estimates a 5.5-year payback period. They document that the expansion will be funded through a combination of bank financing (75 percent) and retained earnings (25 percent). The analysis shows a positive NPV of $340,000, making the investment financially justified. The board approves the capital budget and the project moves to implementation.

How to Prepare a Capital Budget

Step 1: Identify and document all candidate projects. Collect capital requests from department heads and operational leaders. Use a standardized capital request form that requires submitters to document the project description, strategic rationale, cost estimate, expected useful life, and expected return. Standardization ensures that all projects are evaluated on comparable terms.

Step 2: Prioritize by strategic alignment and return. Not all projects with a positive NPV should be funded simultaneously. Capital is finite. Rank projects by a combination of strategic importance, financial return, risk level, and urgency. Projects that are operationally critical (a failing piece of equipment that will halt production) take priority over projects that are growth-oriented but deferrable.

Step 3: Model costs and returns rigorously. For each shortlisted project, build a detailed financial model that captures all costs (acquisition, installation, training, and incremental operating costs) and all returns (incremental revenue, cost savings, and terminal value at end of useful life). Apply sensitivity analysis to the key assumptions: what happens to NPV if revenue growth is 20 percent lower than projected? What if interest rates rise before financing is secured?

Step 4: Evaluate and select. Apply your organization’s capital approval criteria. Most companies use a combination of NPV threshold, minimum IRR, and maximum payback period. Projects that meet all three criteria are approved; those that meet two of three are reviewed by senior leadership; those that meet one or none are declined or deferred.

Step 5: Integrate with the operating budget. Once capital projects are approved, their depreciation schedules, incremental maintenance costs, and new staffing requirements must be reflected in future operating budgets. Capital and operating planning are not sequential; they are continuous loops that feed each other.

Part 3: Key Differences Between Operating and Capital Budgets

Understanding the differences in a structured way helps finance teams, business owners, and department leaders make correct decisions about how to classify and plan for spending.

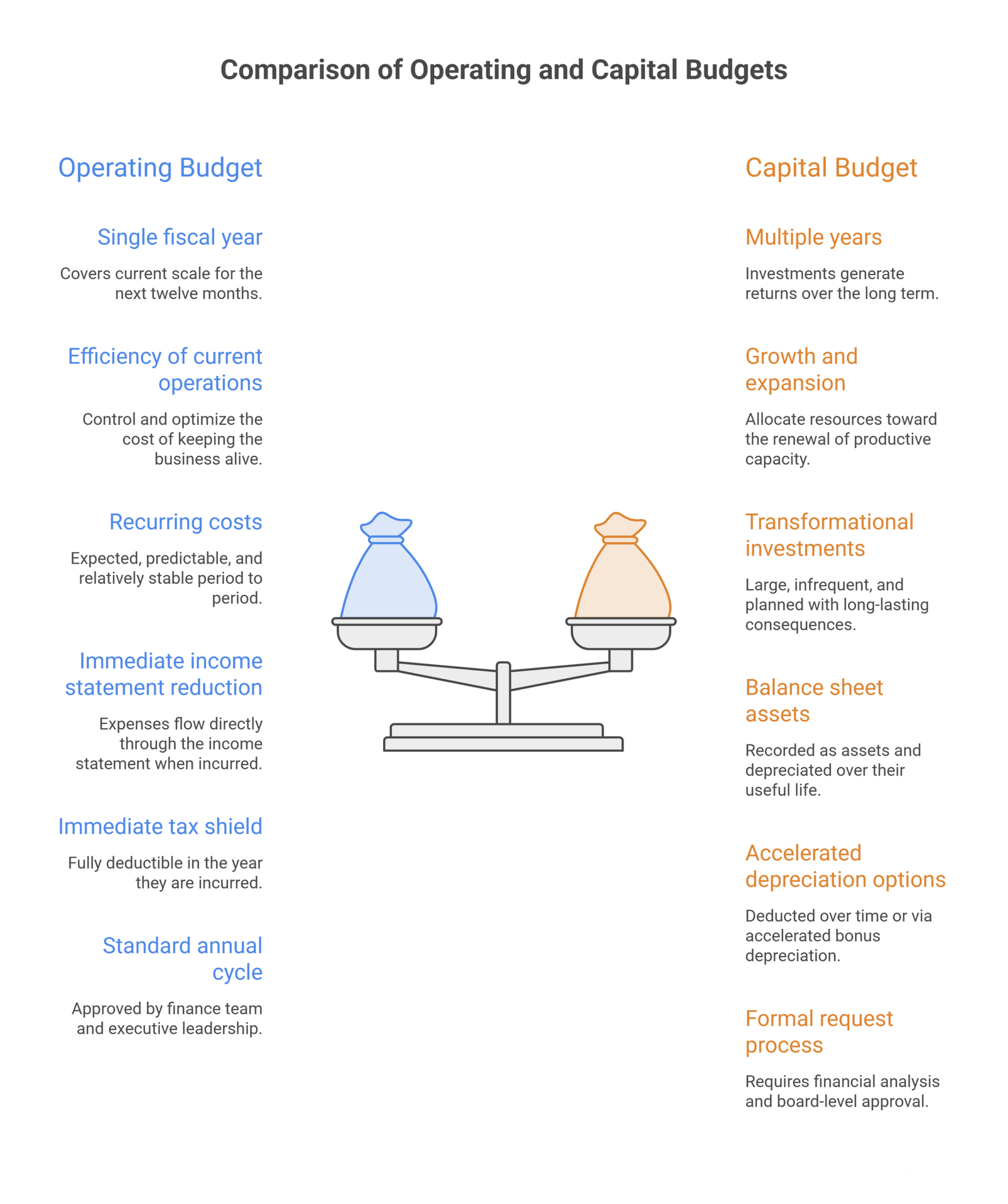

Time Horizon

The operating budget covers a single fiscal year and is often broken into monthly or quarterly sub-periods. It answers the question: what does it cost to run this business at its current scale for the next twelve months?

The capital budget spans multiple years, often three to ten, because capital investments create assets with multi-year useful lives. It answers the question: what investments should we make today that will generate returns over the long term?

Purpose

The operating budget exists to control and optimize the efficiency of current operations. It governs the cost of keeping the business alive and functioning.

The capital budget exists to allocate resources toward growth, expansion, and the renewal of productive capacity. It governs the cost of building what the business will become.

Nature of Costs

Operating costs are recurring: salaries paid monthly, rent charged monthly, utilities billed monthly, supplies replenished regularly. They are expected, predictable, and relatively stable period to period.

Capital costs are large, infrequent, and transformational. Buying a building or a manufacturing line does not happen every year. These investments are planned carefully precisely because they are significant commitments with long-lasting consequences.

Accounting and Financial Statement Impact

Operating expenses flow directly through the income statement in the period they are incurred. They reduce net income immediately and are fully deductible in most cases for tax purposes in the year of payment.

Capital expenditures are recorded as assets on the balance sheet. They do not reduce net income immediately. Instead, they are depreciated over their useful life, with each year’s depreciation charge hitting the income statement. This timing difference is fundamental: a $1 million capital investment might generate only $100,000 in annual depreciation expense if the asset has a 10-year life, so its near-term income statement impact is far smaller than if it had been expensed immediately.

This also affects financial ratios. EBITDA, for example, adds back depreciation because it is a non-cash charge, so EBITDA is not affected by capital spending the way operating costs are. Working capital ratios reflect current assets and liabilities but not fixed assets, so capital spending improves the asset base without necessarily affecting working capital. Mixing capital and operating items corrupts every ratio that depends on clean expense categorization.

Tax Treatment

Operating expenses are generally fully deductible in the year they are incurred, providing an immediate tax shield.

Capital expenses are depreciated over time for book purposes, but tax law often provides accelerated options. Under the 2025 One Big Beautiful Bill Act, 100 percent bonus depreciation is restored for qualifying fixed assets, allowing the full cost to be deducted in year one for tax purposes even while being depreciated over multiple years on the books. The Section 179 expensing limit was raised to $2.5 million, expanding access to immediate tax deductions for smaller capital investments. Businesses that understand this distinction can structure their capital spending to capture maximum near-term tax savings.

Approval Process

Operating budget items are typically approved annually by the finance team and executive leadership as part of the standard budget cycle. Routine operating expenses within approved categories often require only manager-level sign-off.

Capital expenditures, given their size and permanence, require a more formal approval process. Most organizations require a capital request form, supporting financial analysis, and executive or board-level approval for items above a defined threshold, often $10,000 to $50,000 depending on the size of the organization.

Part 4: How Operating and Capital Budgets Interact

These two budgets are not parallel, independent plans. They are deeply interconnected, and managing that connection is one of the most important skills in corporate financial planning.

Operational Surplus Funds Capital Investment

When the operating budget is managed well and the business runs efficiently, it generates cash. Retained earnings from profitable operations are one of the most cost-effective funding sources for capital investment because they carry no interest cost and no dilution of ownership. A business that consistently exceeds its operating budget targets builds the internal capital base that fuels future expansion without taking on debt.

Conversely, a business that consistently overspends its operating budget has less cash available for capital investment. It may be forced to borrow more expensively, delay growth investments, or pass up strategic opportunities because its balance sheet is strained by operational inefficiency.

Capital Investment Creates Future Operating Costs

When a capital investment is approved and implemented, it creates new operating obligations that must be reflected in future operating budgets. A new manufacturing facility requires maintenance staff, utilities, property taxes, and insurance. New enterprise software requires support contracts, training, and IT administration. New vehicles require fuel, insurance, and servicing.

Failing to model these downstream operating costs is one of the most common and expensive mistakes in capital budgeting. A project that looks profitable in isolation can strain the operating budget significantly in its first years of operation, creating cash flow pressure that was not anticipated. The capital budget and operating budget must be modeled together, not sequentially.

Depreciation Bridges the Two Budgets

Depreciation is the accounting mechanism that connects capital investment to operating results over time. When a $500,000 piece of equipment is capitalized, it does not affect the income statement immediately. But in each subsequent year of the asset’s useful life, a depreciation charge (say, $50,000 per year for a 10-year asset) appears as an operating expense. This means the operating budget in years 1 through 10 will carry a non-cash expense that reduces reported profit, even though no cash is being spent in those years.

Finance teams that manage this connection well use a fixed asset register that tracks all capital purchases, their depreciation schedules, and the resulting annual charges. This register feeds directly into operating budget preparation each year, ensuring that depreciation is accurately forecasted rather than estimated.

Integrated Planning Is the Standard of Excellence

The highest-performing finance organizations do not plan their operating and capital budgets separately. They build an integrated financial plan that models both simultaneously, traces the cash flow implications across time, and shows how today’s capital decisions affect next year’s operating margins. This integrated view is what allows leadership teams to answer questions like: can we afford this capital project without compromising our operating budget? What operating cost savings will this investment generate, and when? How does the depreciation from this investment affect our EBITDA in year three?

Rolling forecasts, updated monthly or quarterly, are the mechanism by which integrated plans stay current. A budget built in October that is never updated is substantially less valuable than one that is refreshed regularly as actual results are known and conditions change.

Part 5: Common Mistakes and How to Avoid Them

Mistake 1: Lumping All Expenses Together

Many smaller businesses maintain a single expense register without distinguishing operating from capital costs. This creates accounting errors, distorts profitability metrics, generates incorrect tax filings, and makes it impossible to evaluate the true return on capital investments. The fix is straightforward: establish a capitalization threshold (for example, any single asset costing over $2,500 with a useful life over one year is capitalized) and apply it consistently.

Mistake 2: Underestimating the Operating Cost Tail of Capital Projects

A capital investment decision that ignores the downstream operating costs it creates will always look better on paper than it performs in reality. Model the full lifecycle cost of every capital project, including maintenance, staffing, insurance, and training, before approving it.

Mistake 3: Building the Budget in Isolation

Budgets created entirely by the finance team without input from operational leaders are structurally compromised. Sales leaders know what the pipeline actually looks like. Operations leaders know which equipment is approaching end of life. IT leaders know which systems need replacement. Gathering that input before finalizing the budget produces a more accurate plan and greater organizational commitment to staying within it.

Mistake 4: Not Adjusting for Inflation

With inflation remaining a significant factor in business cost structures, operating budgets that simply roll forward prior-year expense amounts without inflation adjustments will systematically underfund every cost category. Apply category-specific inflation rates: wage inflation may differ from materials inflation, which may differ from energy cost inflation.

Mistake 5: Ignoring Cash Flow Timing

An operating budget that shows annual profitability can still create a cash crisis if the timing of receipts and payments is not modeled. A business might be profitable on an accrual basis while simultaneously running out of cash because customers pay late and suppliers demand early payment. Build cash flow projections alongside the income statement, not just at year end.

Mistake 6: Skipping Post-Project Reviews on Capital Investments

One of the most underused practices in capital budgeting is the post-implementation review: comparing the actual financial performance of a completed project against the projections that justified its approval. This review reveals whether the budgeting assumptions were sound, holds decision-makers accountable for the returns they committed to, and systematically improves the quality of future capital investment decisions.

Part 6: A Comparison Summary

| Dimension | Operating Budget | Capital Budget |

| Time horizon | One fiscal year (monthly or quarterly) | Multiple years (3 to 10 or more) |

| Focus | Day-to-day operations | Long-term asset acquisition and growth |

| Type of costs | Recurring, routine | Large, infrequent, transformational |

| Financial statement impact | Income statement (expenses) | Balance sheet (assets) |

| Tax treatment | Fully deductible when incurred | Depreciated over useful life (bonus depreciation may apply) |

| Approval level | Department or executive (annual cycle) | Executive or board (project-by-project) |

| Evaluation method | Comparison to revenue and expense targets | NPV, IRR, payback period, profitability index |

| Planning frequency | Annual with monthly tracking | Project-based with ongoing portfolio review |

Frequently Asked Questions

Can an expense be partly operating and partly capital?

Yes. A building renovation that both repairs existing damage (operating) and adds new functionality (capital) must be split between the two categories based on the work performed. This is a common accounting judgment call that requires documentation.

Why does it matter which budget an expense goes into?

It affects your income statement, your balance sheet, your tax position, and your financial ratios. Misclassification distorts all of these and can lead to poor decisions, compliance issues, and missed tax opportunities.

How often should operating and capital budgets be reviewed?

Operating budgets should be reviewed monthly against actual results. Capital budgets should be reviewed at each project milestone and at least quarterly for the overall portfolio of approved investments.

What is the relationship between depreciation and the two budgets?

Capital investments are capitalized on the balance sheet and depreciated over time. Each year’s depreciation charge flows into the operating budget as an expense. This is the accounting bridge between the two budgets.

Do small businesses need both types of budgets?

Yes. Even a business with five employees should distinguish between its operating costs and any significant asset purchases. The formality of the process scales with business size, but the conceptual discipline applies to every organization.

What happens if a company only has an operating budget and no capital plan?

It tends to underinvest in assets, defer maintenance until equipment fails, and miss growth opportunities because it has not evaluated them rigorously. It also loses the tax benefits of structured capital planning.

Conclusion

No business thrives by managing only one of these two budgets. An organization that excels at controlling its operating costs but never invests in its future will gradually become obsolete. An organization that invests aggressively in capital projects without controlling its operating costs will burn through cash faster than it can replace it. Excellence in financial management requires both.

The operating budget ensures the business works well today. The capital budget ensures the business is positioned to work well tomorrow. Together, they form a complete picture of financial health: the income statement tells you what you earned and spent, the balance sheet tells you what you own and owe, and the two budgets behind them tell you whether you planned both well.

Understanding the distinction between these two instruments is not just an accounting exercise. It is the foundation of strategic financial leadership, the capability that allows businesses to grow deliberately, invest confidently, and navigate uncertainty with a clear plan rather than a reactive scramble.

An aggressive capital project without operational cost controls will burn through cash. Tight operational budgeting without long-term investment breeds obsolescence.

Achieving the perfect financial equilibrium requires sophisticated forecasting. Whether you are modeling downstream operating tails for a facility expansion or structuring capital funding sources, Oak Business Consultant provides the precision financial engineering your board and investors demand. We’ll help you establish clear capitalization thresholds and build robust rolling forecasts. Schedule a free financial strategy session with our corporate specialists.