Utilization of Funds in Business Planning

Beyond the Budget: The Art and Science of Utilization of Funds

Every dollar your business holds is either working for you or working against you. There is no neutral ground.

Whether you are running a startup on seed funding, managing a mid-size operation, or preparing investor materials for a Series A, how you deploy your capital shapes everything. This guide covers what utilization of funds actually means, why it matters more than most founders realize, where capital comes from, and how to make smarter decisions with whatever you have.

What Is Utilization of Funds?

Utilization of funds refers to the deliberate deployment of a company’s financial resources toward activities that generate value. It covers the full range of how a business actually spends and invests its capital, from paying salaries and rent to purchasing equipment, funding research and development, expanding into new markets, and managing the daily working capital cycle.

In plain terms, it answers one of the most important questions in business finance: once we have the money, what do we actually do with it?

This is not just about spending carefully. It is about spending with intention. Every allocation decision should move the business measurably closer to its financial and operational objectives. When done well, effective fund utilization increases the firm’s overall value, lowers the cost of capital over time, and keeps cash flows predictable enough to support smart decisions.

When done poorly, even a technically profitable business can find itself unable to meet payroll, repay a loan, or take advantage of a growth opportunity that needed capital right now.

Why It Matters More Than You Think

It Directly Shapes Business Value

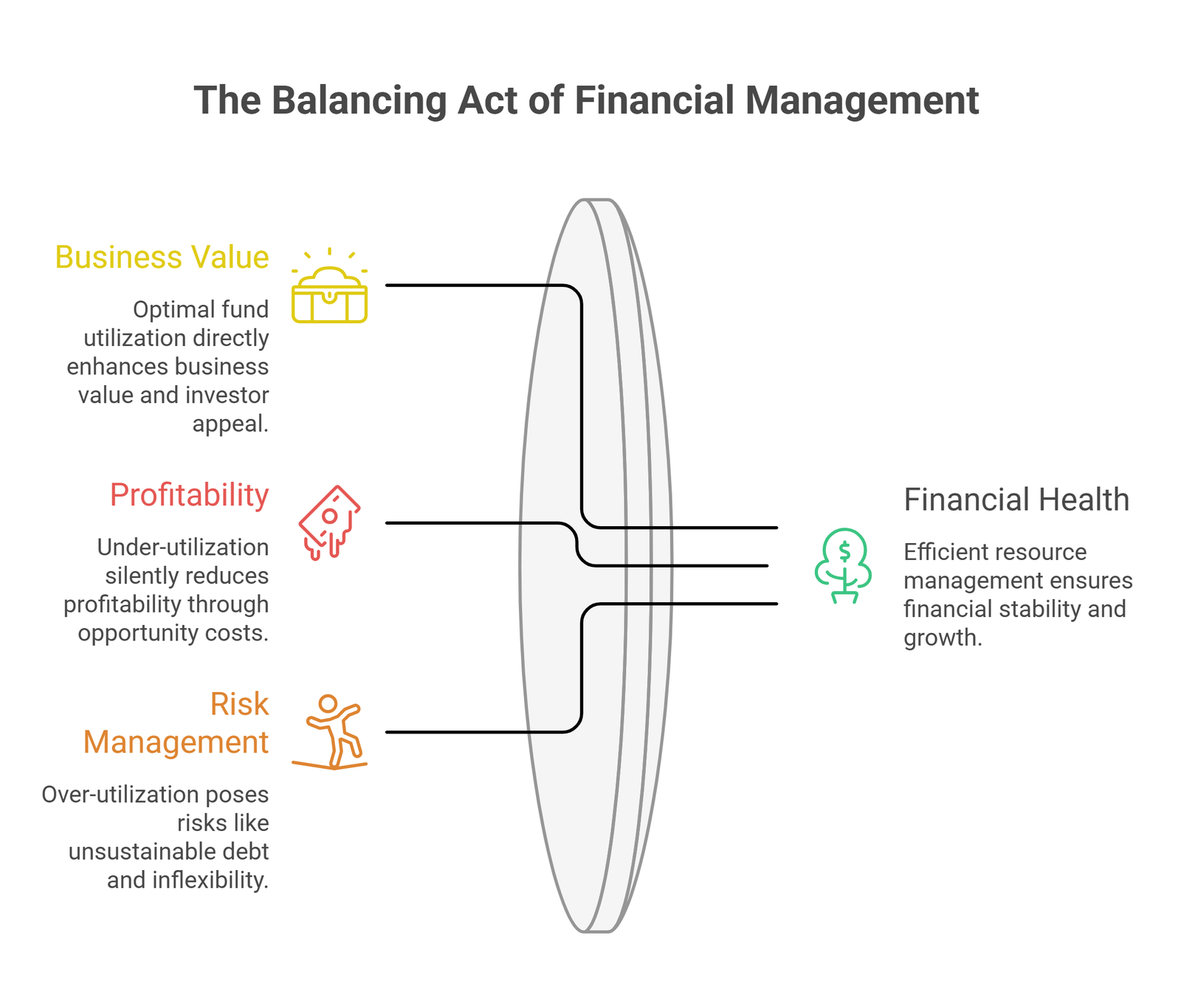

Businesses that put money to work efficiently earn more from the same asset base, reinvest surplus into opportunities that compound returns, and build the kind of financial track record that makes investors and lenders want to participate. The connection between fund utilization and enterprise value is not theoretical. It shows up in margins, in EBITDA, in valuation multiples.

The inverse is equally true. Poor utilization quietly erodes value without any single dramatic event to signal the problem. By the time the damage becomes obvious, it is often structural.

Under-Utilization Is a Silent Profit Killer

When a business lets its resources sit idle, it loses whatever return those resources could have generated. Surplus cash parked in a low-yield account, unused equipment sitting on the floor, inventory that has been overstocked past any realistic demand; these all represent real opportunity cost. This is capital under-utilization, and it tends to accumulate slowly while going largely unnoticed until it has carved a significant hole in profitability.

Over-Utilization Creates a Different Kind of Risk

Deploying funds too aggressively, without adequate financial analysis or cash flow modeling, creates its own set of serious problems. Businesses that overextend often find themselves carrying unsustainable debt loads, losing strategic flexibility to creditors, or unable to raise additional capital when they need it most. Over-utilization can push a company toward default even when revenue looks healthy on paper.

The goal is balance. A company needs to find the appropriate deployment level for its current stage, risk tolerance, and long-term strategy, and then monitor and adjust that level regularly.

The Role of Financial Management

Financial management is the structural backbone that makes disciplined fund utilization possible. It involves four core activities that work together as a system:

Planning involves estimating capital requirements based on realistic cost projections, growth targets, and both short-term and long-term operational needs. Without a solid plan, fund allocation becomes guesswork.

Organizing means constructing a capital structure that balances debt and equity in proportions that suit the business’s risk profile and growth trajectory. A company that is too equity-heavy may be leaving leverage on the table. One that is too debt-heavy may be one bad quarter away from a covenant breach.

Controlling involves the ongoing process of monitoring cash flows, reviewing financial statements at regular intervals, and adjusting allocations as market conditions and business performance shift. Budgets set in January are not automatically valid in October.

Directing means making active, informed decisions about investments, financing arrangements, and returns to shareholders to maximize long-term value while keeping risk within acceptable limits.

Today, financial managers operate in an increasingly complex environment. Capital expenditure decisions, loan structuring, and market entry strategies all carry significant downstream consequences. Reading a profit and loss statement with precision is table stakes. What separates good financial management from great financial management is the ability to see forward, model scenarios, and make decisions before problems develop.

Types of Fund Utilization

1. Funds Invested in Fixed Assets

Long-term investments in property, equipment, machinery, and infrastructure form the productive backbone of most businesses. These are not one-time purchases; they are commitments that must be planned forward because fixed assets depreciate over time and will eventually need replacement or upgrade.

Sound capital budgeting for fixed assets involves analyzing expected returns against opportunity costs, running profit and loss projections tied to the asset’s expected productive life, and making sure the purchase timing aligns with the business’s revenue trajectory. When done right, these investments push operations toward optimal capacity and generate consistent, measurable returns. When done wrong, they tie up capital in assets that cannot carry their weight.

2. Funds Invested in Current Assets

Short-term or current assets, including cash on hand, accounts receivable, and inventory, require equally careful attention as part of the broader working capital cycle.

The objective here is efficiency rather than accumulation. Excess inventory ties up funds that could be deployed elsewhere, often at far better returns. Slow-moving receivables reduce available cash and can mask underlying credit risk with customers. Overly conservative cash reserves sacrifice returns unnecessarily.

Effective working capital management keeps adequate liquidity available without letting funds stagnate. It requires regular review, solid accounts receivable practices, disciplined inventory management, and a clear understanding of the business’s actual cash conversion cycle. This is an area where many small and mid-sized businesses consistently underperform, often because it gets treated as an operational issue rather than a financial one.

Sources of Funds

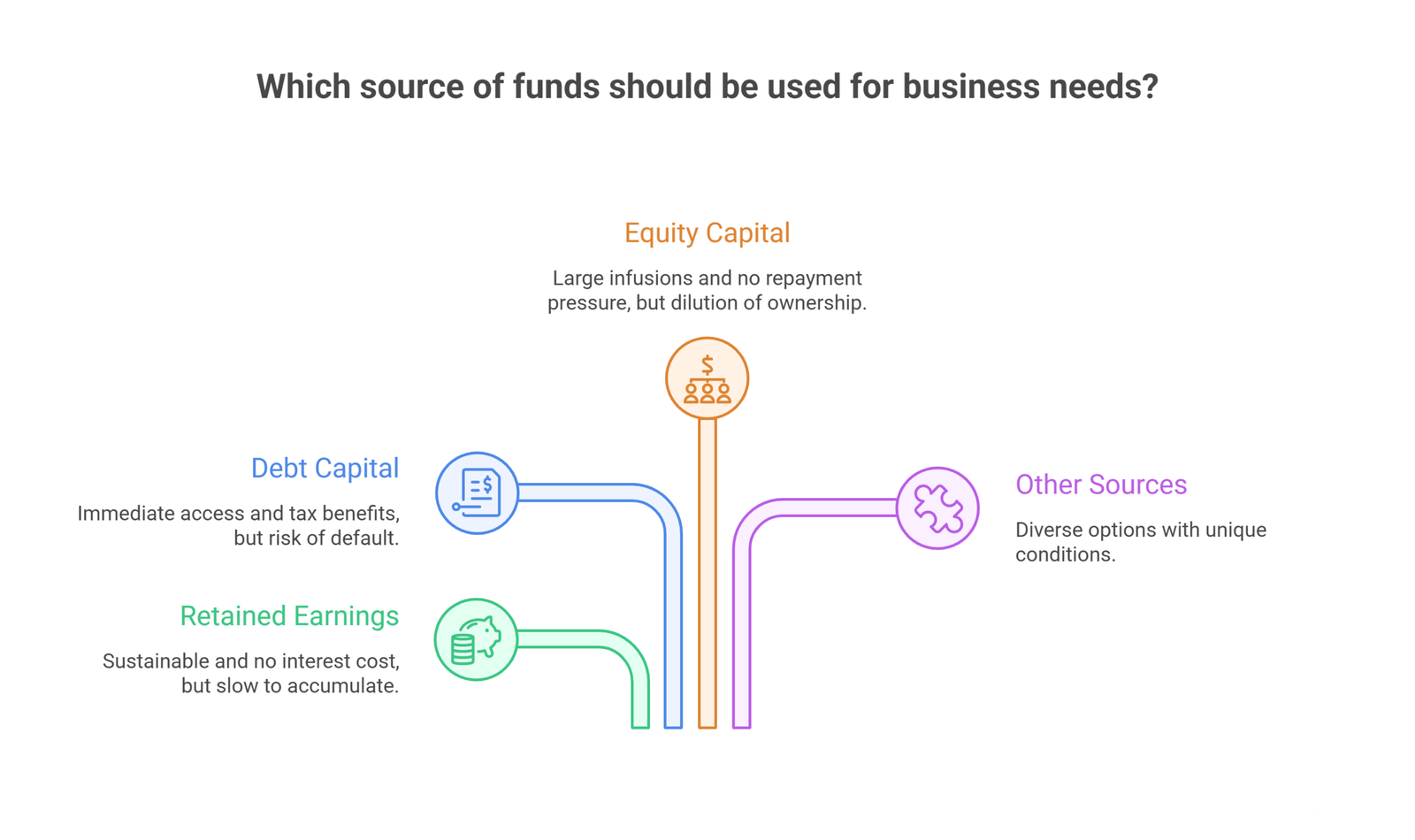

To invest, expand, or simply sustain operations through a lean quarter, a business needs access to capital. There are three primary sources, each with distinct characteristics, costs, and appropriate uses.

Retained Earnings

The most straightforward source. A business generates revenue, covers its expenses, and retains whatever margin remains after dividends or owner draws. Those retained earnings can fund new initiatives, cover operational gaps, or be held as a strategic cash reserve.

Retained earnings carry no interest cost and do not dilute ownership stakes. For businesses with consistent profitability and patient leadership, this is often the cleanest and most sustainable form of internal funding. The downside is speed; retained earnings accumulate gradually and may not match the pace that growth opportunities demand.

Debt Capital

Companies can access capital through bank loans, revolving credit facilities, term loans, or by issuing bonds to institutional or public investors. Lenders become creditors rather than owners, and the business repays the principal with interest over an agreed timeline.

Debt is a powerful tool when used appropriately. It provides immediate access to capital without diluting ownership, and interest payments are often tax-deductible, which lowers the effective cost of borrowing. However, the business must be able to service that debt from consistent cash flows. Consistent failure to meet interest payments or principal repayments creates default risk, which can lead to loss of assets, loss of business control, or insolvency.

The level of debt a business carries must always be matched to its demonstrated ability to generate revenue, not its projected ability.

Equity Capital

Selling shares allows a company to raise capital from investors who become partial owners. These shareholders earn returns through dividends and share price appreciation as the business grows.

Equity financing suits businesses that need large capital infusions and are willing to share ownership control and accountability with a broader investor base. It does not create the same repayment pressure that debt does, which makes it well-suited for early-stage companies or those pursuing long-horizon growth strategies. The tradeoff is dilution of existing ownership stakes and the ongoing obligation to answer to investors.

Other Sources

Beyond these three core channels, businesses can also explore crowdfunding platforms, government grants and subsidies, angel investment networks, venture capital, strategic partnerships with capital components, and in certain industries or geographies, specific development funds or public financing programs. These alternatives often come with their own conditions, timelines, and reporting requirements that must be factored into the decision.

Effective Strategies for Fund Utilization

Match the Funding Horizon to the Asset Life

Short-term needs, payroll, inventory, accounts payable, should generally be financed with short-term funds. Long-term investments, equipment, property, multi-year product development, should be financed with long-term capital. Mismatching these horizons creates liquidity risk because short-term debt comes due before long-term assets generate their full return. It also tends to raise overall capital costs.

Review Financial Statements on a Regular Cycle

Cash flow statements, income statements, and balance sheets are active management tools, not just compliance documents. Reviewing them monthly or quarterly reveals spending patterns, flags underperforming investments early, and shows where reallocation could meaningfully improve returns. A business that only looks at its financials at year end is operating with one eye closed.

Build a Contingency Reserve

Unexpected costs are not exceptions in business; they are certainties over any multi-year horizon. Maintaining an emergency reserve covering three to six months of critical operating expenses protects the business during downturns, supply disruptions, or sudden market shifts. Having that buffer means the business can respond without resorting to emergency borrowing at unfavorable rates or making panic-driven decisions.

Use Budgeting as a Decision Tool, Not Just a Tracker

A well-constructed budget is not a constraint. It is a framework for making better decisions faster. Breaking down expenditures by function, team, or project makes it easier to track what is working, communicate priorities to stakeholders, and reallocate funds when circumstances change. The budget should be a living document that gets revisited and updated as conditions evolve.

Track Return on Every Capital Deployment

Every significant capital allocation should be measured against a projected return. Marketing spend, equipment purchases, new hires, research investments, geographic expansion: all of these should have an expected ROI attached before the decision is made, and a review cycle to see how actual results compare. When returns fall short of projections, good financial managers act early rather than waiting for the gap to compound.

Common Mistakes and How to Avoid Them

Borrowing faster than revenue grows. Taking on debt at a pace that outstrips revenue growth creates a debt service burden that the business cannot reliably meet. The solution is to model debt capacity conservatively and stress-test it against a realistic downside scenario before committing.

Neglecting working capital in favor of long-term investments. Many businesses get focused on growth investments and let day-to-day liquidity management slide. Cash flow problems kill businesses even when they are technically profitable. Keeping a close eye on the cash conversion cycle is not optional.

Skipping regular financial reviews. A budget set at the start of the year does not automatically stay relevant. Markets shift, costs change, and revenue sometimes behaves very differently than projected. Regular financial reviews keep the plan grounded in reality rather than hope.

Treating all funds as interchangeable. Restricted funds, retained earnings, and borrowed capital each come with different obligations, costs, and appropriate uses. Treating them as one undifferentiated pool leads to misallocation and, often, compliance problems.

Overinvesting in fixed assets before revenue is stable. Purchasing expensive equipment or real estate before the business has demonstrated steady revenue ties up capital in assets that may not generate adequate returns, while simultaneously reducing the flexibility to respond to changing conditions.

Frequently Asked Questions

What is the difference between fund allocation and fund utilization?

Fund allocation is the decision about how to divide available capital across different categories, departments, or projects. Fund utilization is about how effectively that capital is actually deployed and put to work once allocated. A business can allocate funds thoughtfully on paper and still utilize them poorly in practice if there is no monitoring, accountability, or course correction built into the process.

How much should a company keep in cash reserves?

Most financial advisors recommend maintaining reserves that cover three to six months of critical operating expenses. The right level depends on the industry, how predictable revenue is, and whether the company has access to emergency credit facilities. Businesses in volatile sectors, or those without established credit lines, generally need larger buffers. Reserves that are too small leave the business exposed; reserves that are too large sacrifice returns that could be generated by putting that capital to work.

What happens when a business over-utilizes its funds?

Over-utilization typically means deploying capital beyond what the business can sustainably support from its cash flows. The practical consequences include excessive debt accumulation, rising financial risk, reduced control over business decisions as creditors gain influence, and in serious cases, an inability to raise additional funds. Projects funded through over-utilization also tend to be underplanned, which means they consume capital without generating adequate returns.

When should a business reconsider its fund utilization strategy?

Any significant change in business conditions warrants a review: a drop in revenue, a new market opportunity, a change in the competitive landscape, a shift in interest rates, or a transition from one growth stage to the next. Beyond reactive reviews, building a scheduled quarterly review of capital deployment into the business rhythm is good practice regardless of conditions.

Conclusion

Utilization of funds is not a back-office function or a technical detail to delegate to an accountant. It is a core strategic discipline that determines whether a business can grow, respond to challenges, build investor confidence, and create lasting value.

The most financially healthy businesses are not always the ones with the most capital. They are the ones that use whatever capital they have with clarity and intention: tracking returns, maintaining healthy liquidity, matching funding types to their appropriate uses, and staying close enough to their financial data to course-correct before small problems become expensive ones.

Whether you are managing retained earnings, leveraging debt to accelerate growth, or raising equity from outside investors, the underlying principles stay consistent. Plan carefully, monitor regularly, match the fund to the purpose, and never let capital sit without a reason.

Getting this right is one of the clearest separators between businesses that survive downturns and businesses that build something that lasts.

Once the money is in the bank, the real work begins. Don’t treat your funds utilization strategy like a guessing game. With Oak’s Fractional CFO services, you get a seasoned financial partner to help you balance big expansion plans with healthy cash reserves. We handle the heavy lifting—from tracking fund deployment to monthly financial reviews, so you can focus on scaling safely. Schedule your free CFO strategy session now.