Cash Flow Modeling: A Comprehensive Guide

What Is Cash Flow Modeling?

Think of cash flow modeling as a financial flight simulator. Before a pilot takes off, they run simulations to understand what happens if an engine fails, if the weather changes, or if they need to reroute. Cash flow modeling does the same thing for your money.

At its core, a cash flow model is a structured financial tool that maps out every dollar coming in and every dollar going out over a defined time period, and then helps you forecast what those numbers will look like in the future. It answers three deceptively simple questions:

- How much money do we have right now?

- How much will we have next month, next quarter, or next year?

- What decisions can we make today to be in a stronger position tomorrow?

Whether you are running a startup, managing a growing business, planning for retirement, or evaluating an investment, a cash flow model is the single most practical financial tool available to you. Unlike a profit and loss statement, which shows accounting earnings, a cash flow model shows real money moving in real time. Profitable companies go bankrupt because they run out of cash. A good cash flow model stops that from happening.

The Building Blocks of a Cash Flow Model

Every cash flow model, regardless of how simple or sophisticated, is built from the same core components.

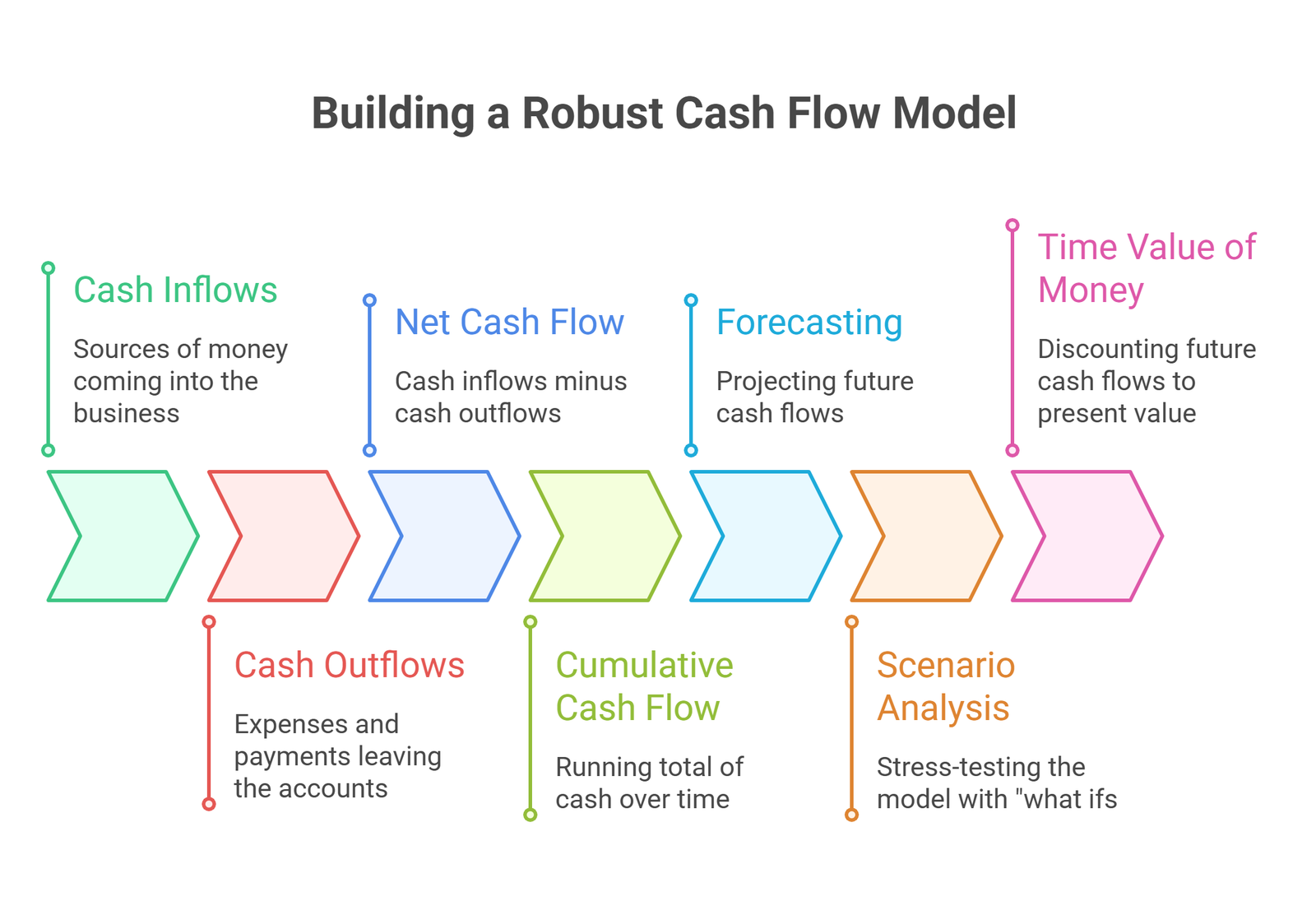

Cash Inflows

These are all the sources of money coming into your business or personal finances. For a business, inflows typically include:

- Revenue from sales or services

- Investment income and dividends

- Proceeds from asset sales or property disposals

- Loan disbursements

- Government grants or subsidies

- Accounts receivable collections (when customers actually pay)

The model estimates not just how much will come in, but when. Timing matters enormously. A sale made in January that gets paid in March does not help you cover your February payroll.

Cash Outflows

These are every expense or payment that causes cash to leave your accounts. Common outflows include:

- Payroll and benefits

- Rent and utilities

- Supplier and vendor payments

- Loan repayments and interest

- Tax payments

- Capital expenditures on equipment, technology, or infrastructure

- Marketing and advertising costs

The discipline of tracking outflows forces you to confront spending patterns you might otherwise ignore. Many businesses discover significant waste simply by modeling their cash flows for the first time.

Net Cash Flow

This is the heart of the model: cash inflows minus cash outflows for each period, typically measured monthly or quarterly. A positive number means you are generating more cash than you are spending. A negative number means you are burning through reserves, which is not always bad (early-stage startups often run negative for a period) but needs to be managed carefully.

Cumulative Cash Flow

This tracks your running total over time. It shows whether you are building reserves or drawing them down. A cumulative cash flow chart can visually reveal how long your current runway lasts before you hit zero, which is critical information for any business or individual managing a tight budget.

Forecasting

Good cash flow models do not just report the past. They project forward based on historical data, known commitments, market conditions, and reasonable assumptions about growth. This predictive layer is what turns a model from a record-keeping tool into an actual planning tool.

Scenario Analysis

Once a model is built, you can stress-test it. What happens if a major client pays 60 days late? What if revenue drops 20% for two quarters? And, what if you land that large contract you have been chasing? Scenario analysis lets you explore these “what ifs” safely, on paper, before they happen in real life.

Time Value of Money

For longer-range models and investment analysis, a sophisticated cash flow model will also discount future cash flows back to their present value. A dollar received three years from now is worth less than a dollar received today, because today’s dollar can be invested and grow. Discounted Cash Flow (DCF) analysis builds this logic directly into the model, making it invaluable for M&A transactions, project financing, and investment decisions.

How Cash Flow Modeling Actually Works

Cash flow modeling is not a one-time exercise. It is a continuous, living process. Here is how it works in practice.

Starting with a Financial Snapshot

The model always begins with where you are right now. That means pulling together:

- Current bank balances and cash on hand

- All outstanding invoices (money owed to you)

- All outstanding payables (money you owe others)

- Scheduled loan repayments

- Upcoming large expenses

This baseline gives you an accurate starting point. A model built on incorrect starting data will produce incorrect forecasts, so this step deserves real care.

Mapping Income Streams

Once you know where you stand, you map out your revenue sources with as much granularity as possible. For a business with multiple revenue streams, such as a subscription product, a services line, and licensing fees, each stream should be modeled separately. They behave differently, grow at different rates, and carry different levels of certainty.

For individuals, income streams might include salary, freelance income, rental income, investment distributions, and any side income. Again, modeling these separately gives you a cleaner picture.

Tracking Fixed vs. Variable Expenses

Expenses come in two flavors. Fixed expenses are predictable and do not change much month to month: rent, salaries, insurance premiums, software subscriptions. Variable expenses fluctuate with activity: materials, shipping, sales commissions, freelance labor.

A good model separates these because they respond differently to growth or contraction. If revenue doubles, your variable costs will likely rise proportionally. Your fixed costs probably will not.

Building in Key Drivers

Every business has a handful of variables that disproportionately influence cash flow. These are called cash flow drivers. For a retailer, it might be inventory turnover. For a SaaS company, it might be monthly churn rate and average contract value. Moreover, for a real estate developer, it might be draw schedules and pre-sale ratios.

Identifying and explicitly modeling your key drivers makes your model far more useful, because you can see exactly which levers to pull to improve your cash position.

Regular Reviews and Updates

A cash flow model that is built once and never updated is a historical document, not a planning tool. Effective cash flow modeling involves regular reviews, typically monthly, to compare actual results against the forecast. Where there are gaps, you investigate why and update your assumptions. Over time, this process makes your forecasts increasingly accurate.

Incorporating Capital Expenditures and Non-Cash Items

Capital expenditures (CapEx) represent large, infrequent cash outflows for assets like equipment, software, or buildings. These need to be planned for carefully since they can significantly strain cash reserves even when a business is otherwise profitable.

Non-cash expenses like depreciation do not directly affect cash flow, but they affect taxable income and therefore tax payments, which do affect cash. A thorough model accounts for this relationship.

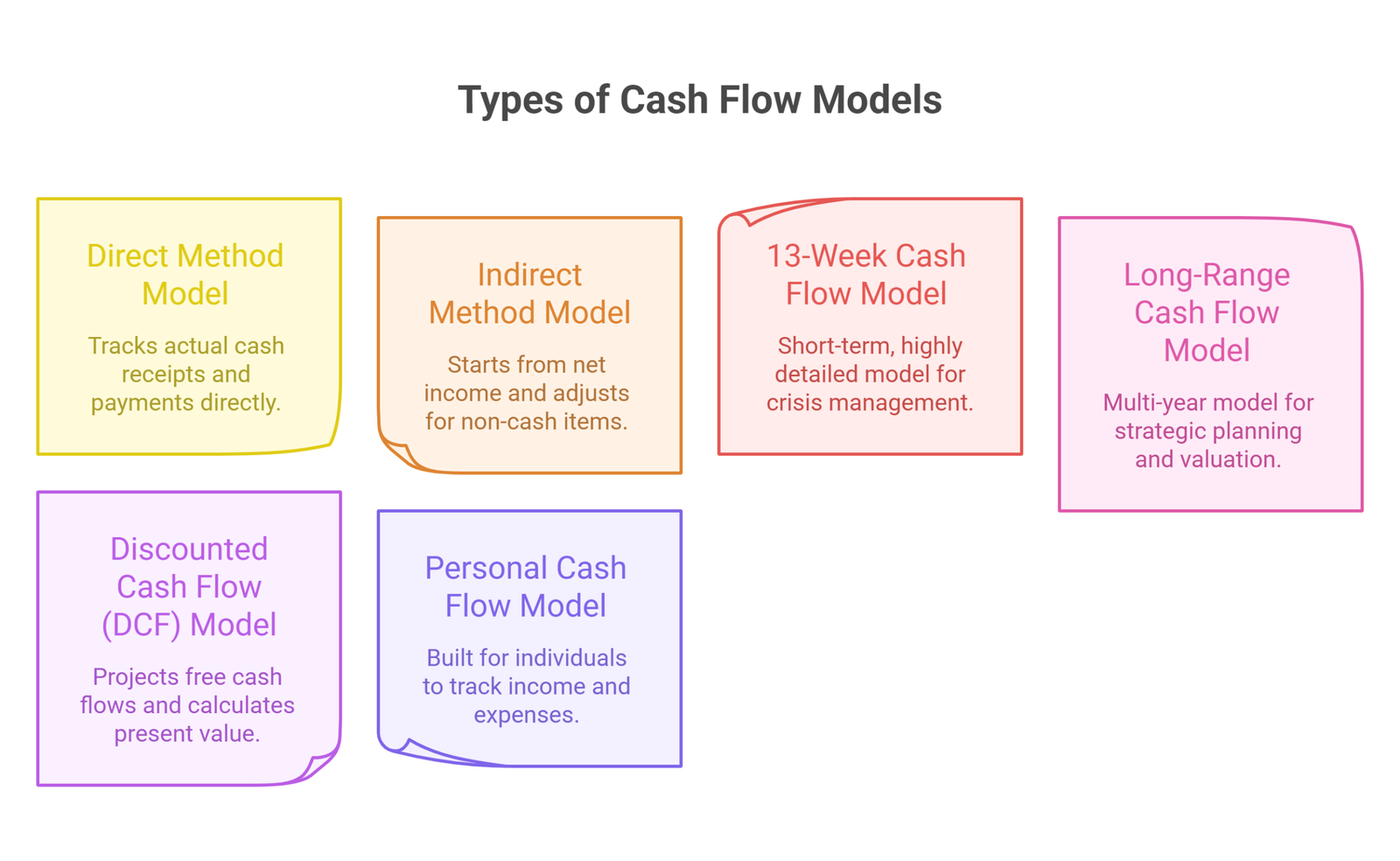

Types of Cash Flow Models

There is no single “correct” type of cash flow model. The right approach depends on your purpose, your business stage, and the complexity of your finances.

Direct Method Model

This approach tracks actual cash receipts and payments directly. It is straightforward and easy to understand, making it ideal for small businesses, startups, and individuals. Every line represents a real cash movement.

Indirect Method Model

Starting from net income and adjusting for non-cash items and working capital changes, the indirect method reconciles accounting profit to actual cash generated. This is the method most large companies use in their financial statements and is required for public company cash flow reporting.

13-Week Cash Flow Model

A short-term, highly detailed model covering 13 weeks (one quarter) at a time. This is the preferred tool in crisis management, turnarounds, and restructuring situations where visibility into the immediate future is critical. Private equity firms and lenders often require this from distressed borrowers.

Long-Range Cash Flow Model

A multi-year model built for strategic planning, valuation, and fundraising. These models incorporate revenue growth assumptions, margin improvement, CapEx schedules, and financing arrangements over a 3 to 10-year horizon. They are less precise in the out-years but essential for big-picture decision-making.

Discounted Cash Flow (DCF) Model

The gold standard for investment and business valuation. A DCF model projects free cash flows over a forecast period, applies a discount rate reflecting the risk of those cash flows, and calculates a present value. It is used in M&A, venture capital term sheets, and real estate underwriting.

Personal Cash Flow Model

Built for individuals rather than businesses. It tracks take-home income, monthly expenses, debt service, savings contributions, and investment distributions. An effective personal model reveals whether your current financial behavior will get you to your goals, whether that is paying off a mortgage, funding a child’s education, or retiring at a specific age.

Why Cash Flow Modeling Matters

It Tells the Real Story

Revenue figures look great on a pitch deck. But revenue does not pay salaries. Cash does. Cash flow modeling strips away accounting abstractions and shows you the real financial picture. Many businesses have filed for bankruptcy while technically profitable, because they could not collect receivables fast enough to meet their payroll and vendor obligations. A cash flow model would have flagged that risk well in advance.

It Puts You in Control of Timing

Most financial disasters are timing problems. A large tax bill hits the same month a major client pays late. A piece of critical equipment fails right before your slowest season. Cash flow modeling does not eliminate these events, but it gives you early warning so you can prepare. You can arrange a line of credit before you need it, negotiate better payment terms with suppliers, or time a capital expenditure for a stronger cash period.

It Guides Your Financial Goals

For individuals, a cash flow model is the link between where you are and where you want to be. It helps you understand exactly how much you can save each month, when you can realistically pay off debt, and how much lifestyle flexibility you actually have versus how much you think you have. Additionally, it makes abstract goals, like retiring at 55 or buying a vacation home, concrete and plannable.

It Is Required for Serious Capital Raising

If you are raising equity investment or applying for a meaningful bank loan, you will need to present a credible cash flow forecast. Investors and lenders use it to assess whether the business can generate enough cash to fund operations, service debt, and eventually return capital. A well-built cash flow model signals financial maturity and builds confidence.

It Catches Problems Before They Become Crises

A cash flow model essentially runs your business forward in time. If the model shows you running negative in month seven, you have seven months to fix it. That is time to close a new client, raise prices, reduce expenses, or arrange backup financing. Without the model, you discover the problem when it is already a crisis.

Key Benefits

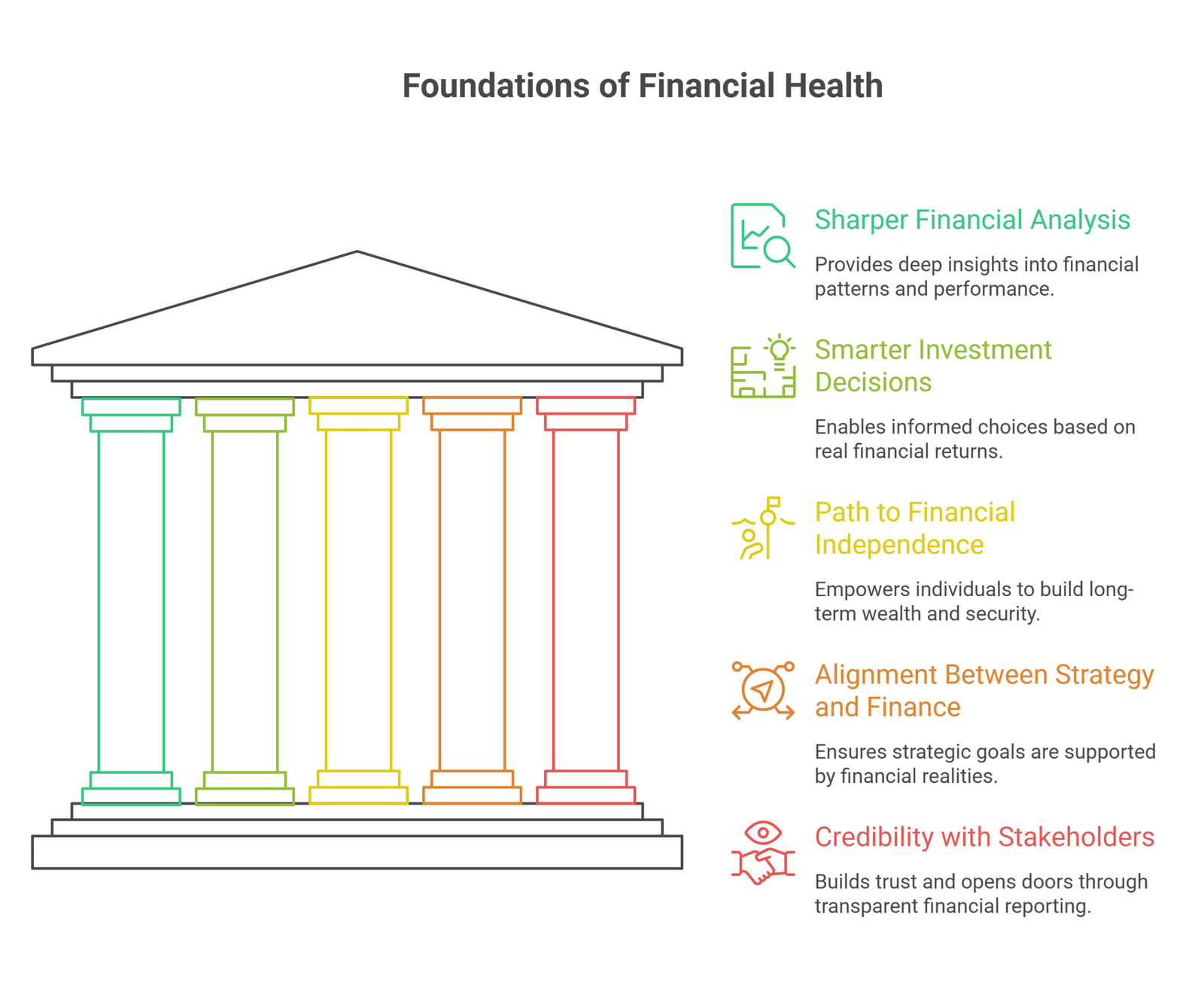

Sharper Financial Analysis

A cash flow model organizes your financial data in a way that makes patterns visible. You can see seasonality in your revenue. Additionally, you can see months where outflows consistently spike. You can identify which product lines or clients are generating the most cash versus which are consuming it. This kind of visibility is simply not available from a bank statement or a basic income report.

Smarter Investment Decisions

When evaluating an investment, whether it is a new piece of equipment, an acquisition, a marketing campaign, or a real estate purchase, a cash flow model lets you calculate the actual return in real money, not just projected profit. You can see how long it takes to pay back, what the ongoing cash impact is, and how it changes your overall liquidity position.

A Path to Financial Independence

For individuals, a cash flow model is arguably the most powerful tool available for building long-term wealth. By understanding exactly where every dollar goes, you can systematically direct more toward savings and investments. You can quantify the impact of paying off high-interest debt versus investing the difference. You can model retirement scenarios and understand exactly what savings rate you need to hit your target.

Alignment Between Strategy and Finance

For businesses, cash flow modeling ensures that strategic goals do not outrun financial reality. Ambitious growth plans require cash to execute. Hiring, marketing, inventory, and infrastructure all need funding. A cash flow model shows whether your growth plans are actually funded or whether they will create a crisis if not managed carefully.

Credibility with Stakeholders

Whether it is a board of directors, an investor, a lender, or a business partner, presenting a detailed and well-reasoned cash flow model signals that you understand your business at a deep level. It builds trust and opens doors that rough estimates and gut-feel projections simply cannot.

Common Mistakes to Avoid

Even experienced finance professionals make these errors. Knowing them in advance will save you significant pain.

Confusing profit with cash. These are not the same thing. A business can show a healthy net income while its cash account is running dry, especially when growth is rapid and working capital requirements are rising fast. Always model cash, not just profit.

Being too optimistic on revenue timing. Customers take longer to pay than you expect. Deals take longer to close than the pipeline suggests. Build in realistic collection periods and be conservative on when new revenue converts to actual cash received.

Forgetting lumpy expenses. Annual insurance premiums, quarterly tax payments, equipment replacements, and year-end bonuses are easy to forget in a model that focuses on monthly averages. Build them in explicitly.

Ignoring working capital changes. As revenue grows, so does the cash tied up in receivables and inventory. Fast-growing businesses often face a cash squeeze precisely because their success is outpacing their working capital. A good model explicitly tracks these changes.

Building the model once and abandoning it. A cash flow model provides value in proportion to how actively it is maintained. An outdated model breeds false confidence. Set a regular cadence for updates, at least monthly.

Over-engineering before you understand the basics. Start simple. A clean, well-understood model with 20 line items beats a complex spreadsheet with 200 line items that nobody trusts or updates.

Step-by-Step: Building Your First Cash Flow Model

You do not need specialized software to build a useful cash flow model. A spreadsheet works perfectly for most businesses and individuals.

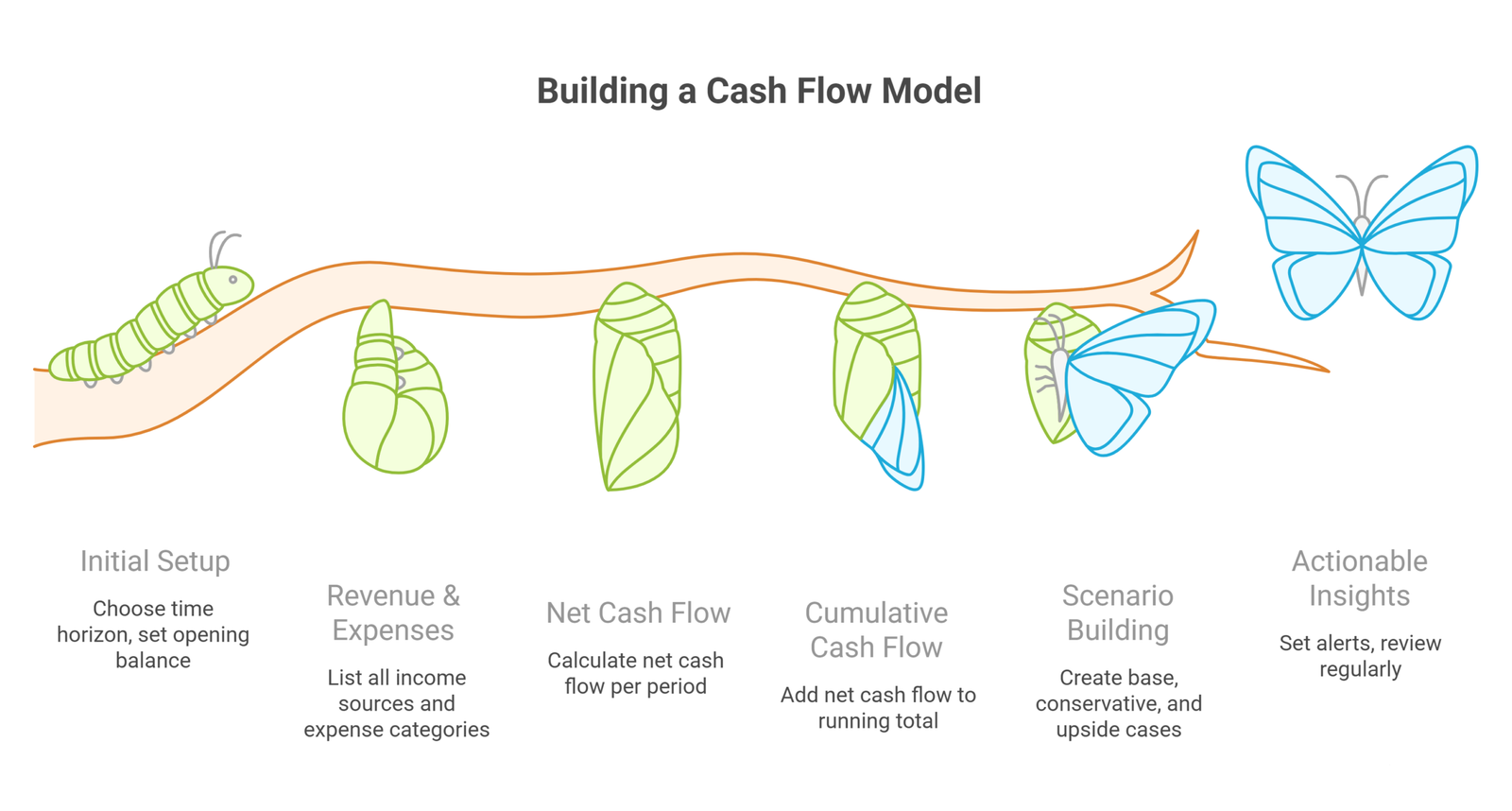

Step 1: Choose your time horizon and period length. For most businesses, a 12-month model with monthly periods is the right starting point. If you need more granularity (for example, during a cash-tight period), shift to weekly periods for the next 13 weeks.

Step 2: Set your opening balance. Enter your current total cash balance as of today. This is your starting point.

Step 3: List all revenue sources. For each source, estimate how much comes in and when. If you have historical data, use it. If not, be conservative.

Step 4: List all expense categories. Separate fixed expenses (same amount each period) from variable expenses (tied to revenue or activity levels). List every category you can think of, then add a miscellaneous buffer of 5 to 10 percent.

Step 5: Calculate net cash flow per period. Subtract total outflows from total inflows for each column (month or week).

Step 6: Calculate cumulative cash flow. Add each period’s net cash flow to the running total. This tells you at a glance whether you are building up or drawing down.

Step 7: Build your scenarios. Create a “base case,” a “conservative case” (revenue 15 to 20 percent lower than expected), and an “upside case” (revenue 15 to 20 percent higher). Each scenario helps you understand your range of possible outcomes.

Step 8: Set alerts and review dates. Identify the cash balance at which you need to take action (for example, if cumulative cash drops below three months of expenses) and schedule monthly reviews to update actuals versus forecast.

Tools and Software

The best tool is the one you will actually use consistently. Here are the most common options at different levels of sophistication.

Microsoft Excel or Google Sheets. The universal starting point. Highly flexible, widely understood, and perfectly adequate for most cash flow modeling needs. The main limitation is that as the model grows, version control and error risk can become real problems.

Xero, QuickBooks, or Wave. Accounting software with built-in cash flow reporting and basic forecasting features. Great for pulling actual data automatically, though the forecasting features are limited for complex modeling.

Float, Pulse, or Dryrun. Purpose-built cash flow forecasting tools designed for small to medium businesses. They connect to your accounting software and make scenario modeling much easier than a spreadsheet, with better visualizations.

Adaptive Insights, Anaplan, or Vena. Enterprise-grade financial planning platforms with powerful cash flow modeling capabilities, collaboration features, and scenario management. Appropriate for mid-size to large organizations with complex financial structures.

Custom financial models. For complex transactions, M&A, project finance, or investor presentations, a purpose-built custom Excel model built by a financial modeling professional often provides the most precision and credibility.

Frequently Asked Questions

How far into the future should I model?

For operational planning, a 12-month rolling forecast is standard. For strategic planning and fundraising, a three to five-year model is typical. Moreover, for investment valuation and long-term financial planning (retirement, for example), 10 to 30-year models may be appropriate, though projections beyond five years should be treated as directional rather than precise.

Can a business be profitable but still have cash flow problems?

Absolutely, and this is one of the most important concepts in finance. When a business sells on credit, it books revenue before it collects cash. If it is growing fast, the gap between revenue recognized and cash received can become very large. Similarly, businesses with long payment cycles, heavy inventory requirements, or lumpy CapEx schedules can be highly profitable on paper while struggling with day-to-day cash. Cash flow modeling reveals these disconnects before they become emergencies.

How often should I update my cash flow model?

At minimum, monthly. After recording actual results for the prior month, update your forecast for the months ahead. In periods of volatility, uncertainty, or rapid growth, update it more frequently. Many finance teams in high-growth businesses update their 13-week model every week.

What is the most common reason cash flow models fail?

Inconsistent updates. A model that is built with care and then abandoned quickly becomes useless or, worse, misleading. The second most common reason is overly optimistic revenue assumptions, particularly around the timing of cash collection. Be conservative on inflows, thorough on outflows, and disciplined about keeping the model current.

Conclusion

Cash flow modeling is not a finance department luxury or a tool only for large corporations. It is one of the most practical, high-impact financial habits that any business or individual can develop. It turns an abstract financial situation into something concrete, visual, and actionable.

The businesses and individuals who build and maintain good cash flow models share a common trait: they are rarely surprised. They see problems coming with enough time to respond. They make investment and spending decisions from a position of clarity rather than guesswork. And they are able to pursue growth with confidence, because they know exactly how much runway they have and what it will take to extend it.

Start simple. A 12-month spreadsheet with your main income sources and expense categories is enough to generate real insight. Update it monthly. Add complexity as you understand your financial patterns better. Over time, you will build a model that genuinely reflects your business or personal financial reality, and that is one of the most valuable tools you can have.

If you want to go deeper, whether building a sophisticated model for a fundraising round, stress-testing a major investment decision, or getting your first-ever cash flow model off the ground, working with an experienced financial consultant can compress years of trial and error into weeks.

Profit is a Guess. Cash is a Fact. Is Your Business Protected? Don’t let a sudden timing gap or a late-paying client freeze your operations. At Oak Business Consultant, we build custom, dynamic cash flow models and 13-week rolling forecasts designed to give you total visibility over your capital. Eliminate the guesswork and take control of your runway today. Schedule Your Free Cash Flow Strategy Session.