The Fintech Financial Metrics You Need to Monitor

Fintech Financial Metrics For You to Track

Most fintech founders track too many metrics, the wrong metrics, or both. App downloads look impressive in a board deck, but they tell you nothing about whether the business survives its next funding round. The metrics that matter are the ones that show whether you’re acquiring customers profitably, keeping them, and generating enough cash to keep operating.

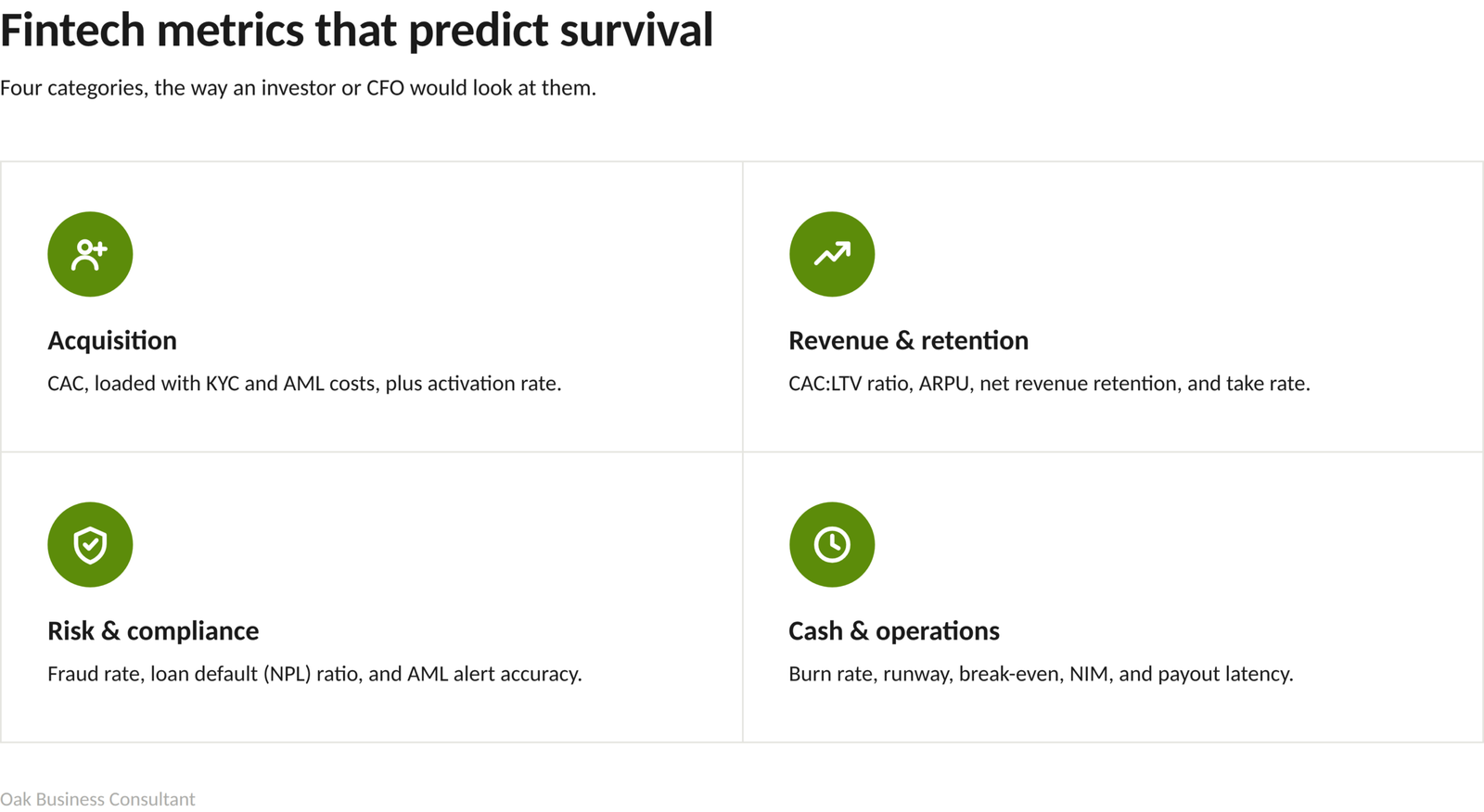

This guide walks through the financial metrics that actually move the needle for a fintech business, organized the way an investor or a CFO would look at them: acquisition, revenue and retention, risk, and cash. We’ll also flag where fintech metrics diverge from standard SaaS or e-commerce benchmarks, because they do, often in ways founders don’t expect until it costs them.

Why fintech metrics need their own playbook

Generic startup KPI lists treat customer acquisition cost (CAC), lifetime value (LTV), and churn as universal truths. They’re necessary, but not sufficient, for a fintech business.

Fintech CAC tends to run structurally higher than CAC for a typical SaaS company, mainly because of know-your-customer (KYC) and anti-money-laundering (AML) compliance costs baked into every signup. Depending on your market and product, that compliance overhead alone can add several dollars per customer before you’ve spent a cent on marketing.

Fintech also carries risk categories that most startups never have to think about: fraud rates, loan default rates, and regulatory alert volumes. A SaaS company that ignores fraud metrics loses some revenue. A fintech that ignores them can lose its operating license.

That’s why the right approach is to track fewer metrics, chosen deliberately for your specific product, rather than monitoring every number a generic dashboard template throws at you.

Acquisition metrics: what it actually costs to get a customer

Customer Acquisition Cost (CAC)

CAC is your total sales and marketing spend divided by the number of new customers acquired in that period. For fintech specifically, build your compliance and onboarding costs into this number, not just ad spend. If you’re paying $15 to $25 per customer in KYC and AML checks before you’ve run a single ad, your “real” CAC is meaningfully higher than what a marketing dashboard shows you.

CAC varies heavily depending on which channels and which sales process you use. Paid search tends to push CAC up fast for B2B fintech products. A direct sales force costs more per customer than a self-serve signup flow. None of this means avoid those channels, it means know the number before you scale spend on any one of them.

Activation rate

Signup is not the milestone that matters. Activation is. For a neobank, that’s the first funded account. Additionally, for a lending platform, it’s the first disbursed loan. For a payments company, it’s the first processed transaction. Whatever your product, define activation as the first action that reliably predicts a customer will keep using your service, not the easiest box to check during onboarding.

Tracking signups without tracking activation is how founders convince themselves growth is healthy when it isn’t. A spike in signups paired with a flat activation rate usually means your funnel is leaking, not converting.

Revenue and retention metrics: the unit economics that decide if you scale or stall

Customer Lifetime Value (CLV) and the CAC:LTV ratio

CLV estimates the total revenue a customer generates over the time they stay with you. On its own it’s an interesting number. Compared against CAC, it’s the single most important ratio in your business.

A CAC:LTV ratio that’s too tight, where you’re spending almost as much to acquire a customer as that customer will ever be worth, signals unsustainable growth no matter how fast your user count is climbing. Most healthy software and fintech businesses target an LTV at least three times their CAC, though the right ratio depends heavily on your specific margins and how capital-intensive your product is.

Average Revenue Per User (ARPU) and Net Revenue Retention (NRR)

ARPU tells you how much revenue each active customer generates on average, which matters most for subscription-style fintech products. NRR measures how your revenue from existing customers changes over time, accounting for upgrades, downgrades, and churn together, rather than tracking churn in isolation.

A business can have a low churn rate and still be shrinking its existing customer revenue if downgrades outpace upgrades. NRR catches that. Watching churn alone usually doesn’t.

Take rate or transaction-based revenue

If your fintech earns money per transaction rather than per subscription, your take rate, the percentage of transaction volume you keep as revenue, is your core revenue metric. Even a tiny take rate can compound into real revenue if transaction volume is high enough, but it also means a small shift in volume moves your top line more than it would for a flat-fee subscription business. Know which model you’re running before you benchmark against someone else’s numbers.

Risk and compliance metrics: the ones that protect the business, not just the P&L

This category doesn’t exist in a typical startup metrics guide, and that’s exactly why fintech founders underweight it.

Fraud rate

This is the percentage of transactions flagged as fraudulent relative to total transaction volume. A rising fraud rate erodes trust with payment processors and banking partners faster than almost anything else, and it can trigger account freezes that have nothing to do with your actual product quality.

Default rate or Non-Performing Loan (NPL) ratio

For any fintech in the lending space, this measures the share of your loan book that isn’t being repaid on schedule. Keeping this number low protects your balance sheet directly. It also affects your cost of capital, since lenders and investors price risk into how much they’ll charge you to fund future loan growth.

AML alert-to-conversion rate

This tracks how many anti-money-laundering alerts your system generates relative to how many actually warrant escalation. A high volume of false positives wastes compliance staff time and frustrates legitimate customers with unnecessary friction. A low volume that’s hiding real risk is worse. The goal is a system tuned tightly enough to catch real issues without drowning your team in noise.

Cash flow and operational metrics: the ones that decide how long you survive

Burn rate and runway

Burn rate is how fast you’re spending cash each month relative to what’s coming in. Runway is how many months of operating cash you have left at that burn rate. These two numbers together answer the only question that matters when things get tight: how much time do you actually have to fix a problem before the business runs out of money?

Time to break-even

This is the number of months until your revenue covers your total costs, fixed and variable combined. For fintech specifically, this matters more than it does for many startups because of how high fixed compliance and operational costs run from day one. A clear break-even analysis gives you and your investors a concrete timeline rather than a vague promise of eventual profitability.

Net Interest Margin (NIM), for lending and deposit-based fintechs

If your business takes deposits or makes loans, NIM measures the spread between what you earn on assets (like loan interest) and what you pay on liabilities (like deposit interest), relative to your earning assets. It’s the closest fintech equivalent to a gross margin, and for digital banks and peer-to-peer lenders specifically, it’s often the single number that determines whether the underlying business model actually works.

Reconciliation cycle time and payout latency

These operational metrics measure how long it takes to reconcile transactions and how fast you actually get money into a customer’s account after a transaction clears. With instant payment rails like FedNow, RTP, and UPI now standard in many markets, a 24-hour batch reconciliation process that was acceptable a few years ago now reads as a broken customer experience.

How many metrics should you actually track

Not all of the above. Pick five to seven metrics that map directly to your specific business model and your current stage, then track those consistently rather than monitoring a long list loosely.

A pre-revenue lending startup should prioritize NPL ratio, runway, and time to break-even. A payments company further along should weight take rate, fraud rate, and payout latency more heavily. The right mix changes as the business matures, so revisit your metric set every funding round or major product shift rather than locking it in once and forgetting about it.

Frequently Asked Questions

What’s the single most important metric for an early-stage fintech?

There isn’t one universal answer, but runway is the metric that determines whether you get to keep working on the others. If you don’t know how many months of cash you have left, every other metric is secondary.

Why is fintech CAC usually higher than SaaS CAC?

Compliance costs. KYC and AML checks add a real, often underestimated cost to every signup before any marketing spend even factors in, and that cost doesn’t show up in most generic CAC calculators.

How often should fintech founders review these metrics?

Cash and risk metrics like burn rate, fraud rate, and NPL ratio deserve weekly attention. Revenue and retention metrics like ARPU and NRR are usually reviewed monthly. Less frequent review on the fast-moving numbers is how small problems become expensive ones.

Is a high churn rate always a bad sign?

Not necessarily on its own. A high churn rate paired with strong NRR can mean you’re losing low-value customers while expanding revenue from the ones who stay. Look at the two together before drawing conclusions from churn alone.

What’s a healthy CAC to LTV ratio for a fintech startup?

A common target is LTV at roughly three times CAC, though capital-intensive fintech models, especially lending, often need a wider margin to account for default risk eating into that lifetime value.

Should a non-lending fintech still track NIM?

No. NIM is specific to businesses that earn interest income, like digital banks and peer-to-peer lenders. A payments or SaaS-style fintech should focus on take rate or ARPU instead.

Final thoughts

The fintech businesses that survive their first few years aren’t necessarily the ones with the flashiest growth numbers. They’re the ones whose founders know exactly which five or six metrics actually drive the business, and who look at those numbers often enough to catch problems while they’re still cheap to fix.

If you’d rather have an experienced finance team build out this tracking system properly, rather than guessing which metrics matter most for your specific model, Oak Business Consultant’s fractional CFO services and financial modeling work cover exactly this kind of fintech-specific setup, from choosing the right KPI set to building the dashboards your investors will actually want to see. Book a call and we’ll map out which metrics matter most for where your fintech business is right now.