Tax Planning Strategies for Small Businesses

Smart Tax Planning Strategies Every Small Business Owner Must Know

Most small business owners are still tax planning off last year’s numbers. The retirement contribution limit you remember, the QBI threshold you have in your head, the mileage rate you use for a quick estimate. All of it moved for 2026, and some of it moved by a lot.

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, rewrote several of the provisions small business owners rely on most. The qualified business income deduction is now permanent instead of set to expire. Bonus depreciation is back to 100%. The SALT cap nearly quadrupled. If your tax plan was built on 2023 or 2024 figures, it is not just outdated. It is leaving money on the table.

This guide walks through what actually changed, with the correct 2026 numbers, and the planning moves that still matter regardless of what year it is.

What Is Tax Planning and Why Does It Matter for Small Businesses?

Tax planning is the process of arranging your financial affairs so you legally minimize what you owe to the IRS and your state. It goes beyond filing a return. It means making deliberate decisions throughout the year about income timing, expenses, entity structure, and retirement contributions.

Unlike employees, business owners do not have taxes withheld automatically. You face self-employment tax, quarterly estimated payments, and a web of rules around deductions, credits, and entity elections. Get it wrong and you overpay. Get it right and you fund your retirement, your growth, and a lower tax bill all at once.

Tax planning happens before December 31, when you can still change the outcome. Tax preparation happens after, when you are just documenting what already occurred. The first saves money. The second reports it.

What Changed in 2026: The OBBBA Effect

The OBBBA made several previously temporary provisions permanent and adjusted others. Here is the short version of what matters for a small business owner.

| Provision | Before OBBBA | 2026 Under OBBBA |

| QBI deduction | Scheduled to expire after 2025 | Permanent, plus a new $400 minimum deduction |

| QBI phase-in range | $50,000 single / $100,000 MFJ | $75,000 single / $150,000 MFJ (wider, more gradual) |

| Section 179 limit | $1.25M (2025) | $2.56 million |

| Bonus depreciation | Phasing down toward 40% | 100%, restored |

| SALT deduction cap | $10,000 | $40,000, rising 1% annually through 2029 |

| Domestic R&D expenses | Amortized over 60 months | Immediately deductible again |

None of these change the fundamentals of good tax planning. They change the dollar amounts you are planning around, and a plan built on old numbers will misfire even if the strategy behind it is sound.

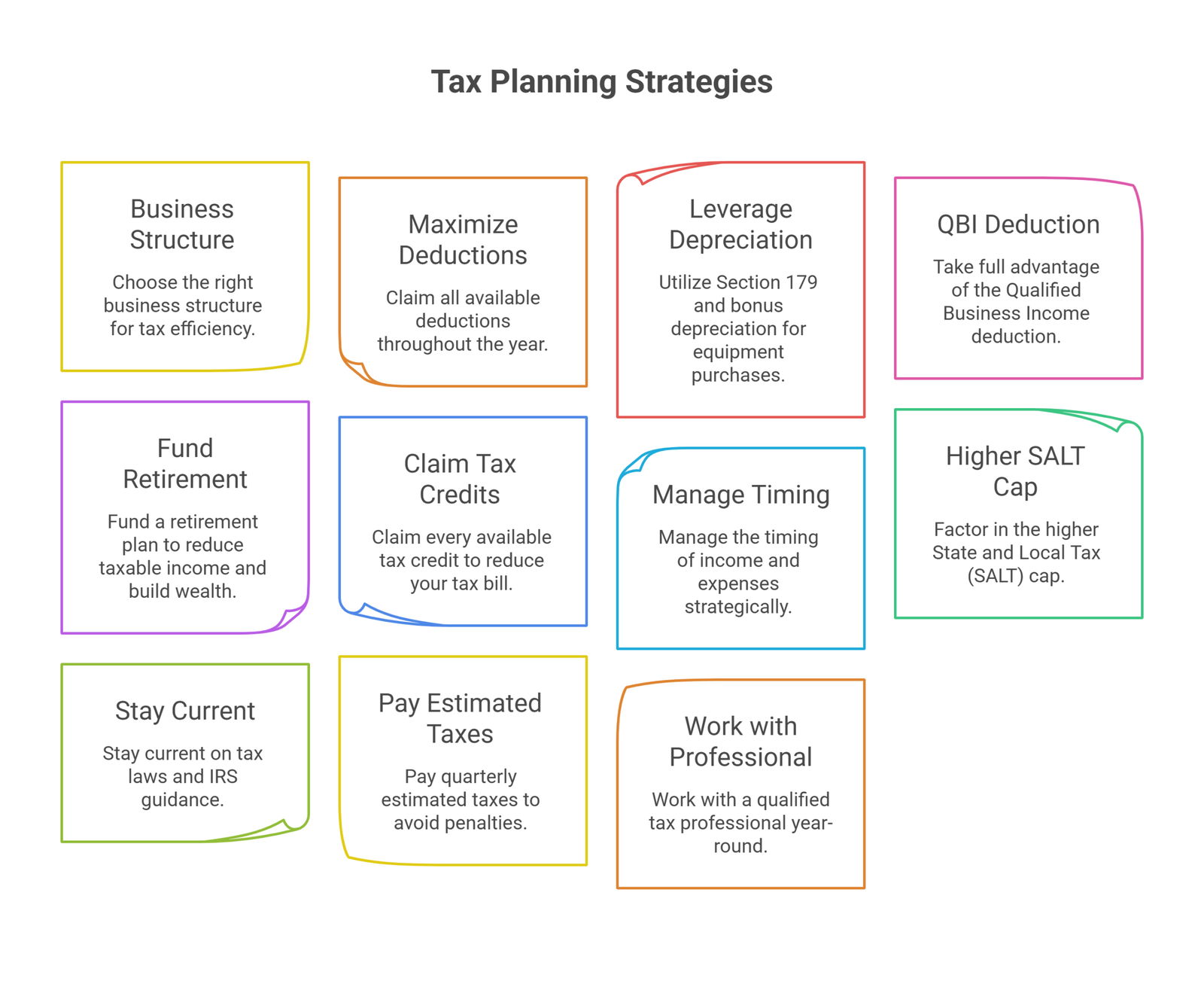

1. Choose the Right Business Structure from the Start

Your business structure is the foundation of your entire tax situation. It determines your tax rate, how profits are distributed, what deductions are available, and your exposure to self-employment tax.

- Sole proprietorship: the simplest structure. Business income flows to your personal Form 1040 and is subject to self-employment tax on the full net profit.

- LLC: a single-member LLC is taxed like a sole proprietorship by default, a multi-member LLC like a partnership. Either can elect S corporation tax treatment, which opens up real planning opportunities.

- S corporation: often the most tax-efficient structure once profits are consistent and meaningful. As an owner-employee, you pay yourself a reasonable salary (subject to employment tax) and take remaining profits as distributions, which are not subject to self-employment tax.

- C corporation: taxed at a flat 21% federal rate, but dividends face double taxation. Usually only worth it if you are retaining significant earnings or raising venture capital.

Here is why the S-Corp election matters in dollar terms for 2026. The Social Security wage base rose to $184,500 this year, so a sole proprietor pays 15.3% self-employment tax on net income up to that amount, then 2.9% above it. An S-Corp owner only pays that 15.3% on the salary portion.

Example: $200,000 in net business income.

- As a sole proprietor: $200,000 x 15.3% = $30,600 in self-employment tax.

- As an S-Corp paying an $80,000 reasonable salary: $80,000 x 15.3% = $12,240 in FICA tax.

That is roughly $18,360 in annual savings from the entity election alone. The IRS requires “reasonable compensation” for the work you actually do, so you cannot set the salary near zero and take the rest as distributions. Setting it too low invites reclassification and penalties. Reviewing your structure annually with a tax advisor keeps you from over- or under-paying as your income changes.

2. Maximize Deductions Throughout the Year

Most small business owners claim the obvious expenses (software, office supplies) and miss the rest.

Home office deduction: deduct a portion of your home’s rent or mortgage interest, utilities, and insurance if part of your home is used regularly and exclusively for business. The simplified method is $5 per square foot up to 300 square feet, or you can calculate actual expenses.

Vehicle expenses: the IRS standard mileage rate for 2026 is 72.5 cents per mile, up 2.5 cents from 2025. Alternatively, track actual vehicle expenses. Either way, keep a contemporaneous mileage log. The IRS does not accept reconstructed logs during an audit.

Business meals: 50% deductible when meeting with clients or prospects. Travel, professional development, industry subscriptions, and advisor fees are generally fully deductible.

Bad debt: income you previously reported that later becomes uncollectible may be deductible in the year it goes bad. Service businesses that invoice clients often overlook this one.

3. Leverage Section 179 and Bonus Depreciation

When your business buys equipment, machinery, vehicles, or technology, the IRS normally requires you to depreciate the cost over several years. Two provisions let you accelerate that.

Section 179: lets you immediately expense the full cost of qualifying property in the year of purchase. For 2026, the maximum deduction is $2,560,000, phasing out once total equipment purchases exceed $4,090,000. It applies to equipment, computers, off-the-shelf software, and certain qualified improvement property. The equipment has to actually be placed in service by December 31, not just ordered.

Bonus depreciation: provides an additional first-year deduction. Under the OBBBA, 100% bonus depreciation is restored for qualifying property acquired and placed in service after January 19, 2025, covering both new and used property. Unlike Section 179, bonus depreciation is not limited by business income and can create a loss.

Domestic R&D expensing: also worth knowing if you develop software, products, or processes. The OBBBA reversed the requirement to amortize domestic research costs over 60 months. Those costs are immediately deductible again in the year incurred.

4. Take Full Advantage of the Qualified Business Income Deduction

The qualified business income (QBI) deduction, also called the Section 199A deduction, lets eligible pass-through owners deduct up to 20% of their qualified business income. The OBBBA made it permanent, so it is now a long-term planning cornerstone rather than a benefit you had to race to use before it expired.

2026 thresholds (per IRS Rev. Proc. 2025-32):

- Full deduction, no limitations: taxable income below $201,750 (single, HOH) or $403,500 (MFJ)

- Phase-in range: widened to $75,000 above the threshold for single filers, $150,000 for MFJ (up from $50,000 and $100,000)

- Full phase-out: $276,750 (single) or $553,500 (MFJ)

- New minimum deduction: if you have at least $1,000 of QBI and materially participate in the business, you are guaranteed at least $400, even if the standard calculation would produce less

If you operate as a sole proprietorship, partnership, S-Corp, or certain trust, you may be eligible. Above the threshold, the deduction becomes limited by W-2 wages paid and qualified property. Certain service businesses, including law, health, consulting, and financial services, face additional restrictions once income exceeds the threshold.

The wider phase-in range under OBBBA is genuinely useful: it means the transition from full deduction to a limited one is more gradual than it used to be, so a business that would have lost the deduction entirely in the old $50,000 window now retains a partial benefit for longer.

5. Fund a Retirement Plan to Reduce Taxable Income

Contributions to qualified retirement plans reduce your taxable income dollar for dollar and build long-term wealth at the same time. The contribution limits increased across the board for 2026.

Solo 401(k): for self-employed individuals with no employees other than a spouse. The employee deferral limit is $24,500 for 2026 (plus $8,000 catch-up if 50 or older, or $11,250 if 60 to 63). Combined with employer contributions, the total limit reaches $72,000 (up from $70,000 in 2025). The plan itself must be established by December 31 of the year you want to contribute, though contributions can be made until your tax filing deadline.

SEP-IRA: simpler to administer, with no annual reporting requirement. The 2026 limit is 25% of net self-employment income, up to $72,000. It can be opened and funded as late as your filing deadline, including extensions.

SIMPLE IRA: employee contributions up to $17,000 for 2026 (or $18,100 under the higher-limit SIMPLE plans some employers can offer), with a required employer match. Best suited to businesses with employees where administrative simplicity matters more than maximizing the contribution ceiling.

Traditional or Roth IRA: $7,500 for 2026, or $8,600 if you are 50 or older.

Funding a qualified plan is one of the highest-leverage tax moves available to a profitable business owner who has not yet maximized retirement savings, and the right advisor can help you pick the plan that fits your income pattern and whether you have employees.

6. Claim Every Available Tax Credit

Deductions reduce taxable income. Credits reduce your tax bill dollar for dollar, which makes them more valuable, and owners routinely miss them.

- Small Business Health Care Tax Credit: up to 50% of health insurance premiums paid (35% for tax-exempt organizations), for businesses with fewer than 25 full-time equivalent employees and average wages below roughly $56,000.

- Work Opportunity Tax Credit: $1,200 to $9,600 per eligible new hire from certain target groups, including veterans and long-term unemployed workers.

- Disabled Access Credit: 50% of eligible expenditures between $250 and $10,250, for a maximum credit of $5,000 a year, for making facilities more accessible.

- Research and Development credit: available to businesses investing in qualifying research, including new products, processes, software, or formulas. Many small businesses in technology, manufacturing, and engineering qualify without realizing it.

- Electric Vehicle Tax Credit: applies to qualified clean energy vehicles purchased for business use, and can be combined with Section 179.

7. Manage Timing of Income and Expenses Strategically

If you use cash-basis accounting, which most small businesses do, you have real control over when income and expenses land for tax purposes.

Additionally, if you expect higher income next year, consider deferring invoicing until January so payment lands in the following tax year. If you expect this year to be the higher-income one, prepay deductible expenses like rent, insurance, or professional subscriptions before December 31 to accelerate the deduction.

This is the same flexibility that comes up throughout cash-basis accounting: you recognize income when received and expenses when paid, which gives you a genuine lever accrual-basis taxpayers do not have.

8. Factor In the Higher SALT Cap

This is new for 2026 and worth its own section, because it changes the math for owners in high-tax states. The state and local tax deduction cap rose from $10,000 to $40,000, and is scheduled to increase 1% annually through 2029 before reverting toward the old cap in 2030.

For S-Corp and partnership owners, most states now offer a pass-through entity (PTE) tax election, letting the business pay state income tax at the entity level instead of the individual level. Entity-level state taxes are deductible on the federal return without the SALT cap applying at all. With the cap now at $40,000, some owners in moderate-tax states may find the PTE election less necessary than it was when the cap sat at $10,000. Owners in high-tax states with pass-through income well above $40,000 will often still benefit. The right answer depends on your state and income level, so this is worth modeling with an advisor rather than assuming either way.

9. Stay Current on Tax Laws and IRS Guidance

Tax law moved more in the past year than in most of the prior decade. The QBI deduction, Section 179, bonus depreciation, the SALT cap, and mileage rates all changed for 2026 under the OBBBA. A plan built on last year’s assumptions is not just slightly off, it can be materially wrong.

Monitoring IRS guidance, or working with someone who does it for you, means you catch new opportunities instead of finding out about them after the deadline has passed. Clean bookkeeping matters here too: you cannot capture a deduction you cannot document.

10. Pay Quarterly Estimated Taxes to Avoid Penalties

Business owners typically do not have taxes withheld from income, so you are responsible for estimated payments four times a year: April 15, June 15, September 15, and January 15 of the following year.

Underpaying triggers a penalty that functions like an interest charge. To avoid it, pay either 100% of last year’s tax liability (110% if your adjusted gross income exceeded $150,000) or 90% of the current year’s expected liability, whichever is smaller. Setting aside 25 to 30% of every payment received into a dedicated tax savings account is a simple habit that prevents a nasty surprise in April.

11. Work with a Qualified Tax Professional Year-Round

The most effective tax planning is not developed in April. It is developed in October, refined in November, and executed before December 31.

A tax advisor or fractional CFO does more than file your return. They model scenarios, flag opportunities specific to your entity and industry, and help you time major decisions before the window closes. If your accountant only contacts you during filing season, the planning window has already passed for the year.

A useful rhythm looks like this:

- October: run income projections based on nine months of actuals. Check how close you are to the QBI phase-in threshold or an SSTB cutoff. If you want a Solo 401(k), it needs to be established by year-end.

- November: finalize equipment purchase decisions for Section 179 and bonus depreciation. Review charitable giving strategy.

- December: max out retirement deferrals, place any Section 179 equipment in service, and handle final S-Corp salary adjustments before the year closes.

Frequently Asked Questions

What changed for small business taxes in 2026?

The One Big Beautiful Bill Act made the QBI deduction permanent, raised Section 179 to $2.56 million, restored 100% bonus depreciation, increased the SALT cap to $40,000, and made domestic R&D expenses immediately deductible again. The 2026 mileage rate also rose to 72.5 cents per mile.

What are the 5 D’s of tax planning?

The 5 D’s are legal methods to lower tax liability: Deduct (claim every eligible expense), Defer (delay tax through retirement contributions or income timing), Divide (split income among entities or family members), Disguise (convert ordinary income into lower-taxed capital gains), and Dodge (use credits to legally reduce what you owe).

How much can small business owners save through tax planning?

It depends heavily on income level and entity structure, but proper entity election alone can save tens of thousands annually for profitable S-Corp candidates, and maximizing retirement contributions can shelter tens of thousands more from current-year tax. The combination of entity structure, retirement contributions, and QBI optimization is where most of the real savings live.

Do I need an S-Corp to save on taxes?

Not necessarily. The S-Corp election tends to make sense once net income is consistently above roughly $75,000 to $80,000, but it adds payroll administration and requires paying yourself a defensible reasonable salary. Below that income level, the added complexity often is not worth the savings.

What is the difference between tax planning and tax preparation?

Tax preparation files your return based on what already happened. It is backward-looking. Tax planning changes what happens so you owe less, and it only works if you act before the tax year ends.

Conclusion

Tax planning for small businesses is not a once-a-year exercise, and in a year with this many rule changes, treating it that way is more costly than usual. The QBI deduction is now permanent, Section 179 and bonus depreciation are both more generous, and the SALT cap gives high-tax-state owners real room to work with. None of that helps if your plan is still running on old numbers.

If you are ready to move from reactive filing to a proactive strategy, Oak Business Consultant’s accounting and bookkeeping team can get your records ready for planning, and our fractional CFO services can help you build a plan around the current rules rather than last year’s. Reach out today to see what a proactive approach could mean for your 2026 tax bill.