All About Chart of Accounts and Bookkeeping for the Education Industry

Beyond Bookkeeping: Optimizing the Chart of Accounts for Educational Industry

The education sector is one of the fastest-growing industries in the world, and it comes with a unique set of financial challenges that most other industries simply don’t face. Schools, colleges, universities, and private institutions all operate under tight scrutiny from boards, governments, donors, and parents. Everyone wants to know where the money is going. That’s exactly why getting your chart of accounts right isn’t just good housekeeping. It’s the foundation of every financial decision your institution will make.

This guide walks you through everything you need to know: what a chart of accounts is, how it works in the education context, what to include in it, and the bookkeeping practices that keep educational institutions financially healthy and compliant.

What Is a Chart of Accounts?

A chart of accounts (COA) is a structured list of every account your institution uses in its general ledger to record financial transactions. Think of it as the master index of your school’s financial life. Every dollar that comes in or goes out gets assigned to a specific account, and those accounts collectively tell the story of your institution’s financial health.

Each account in a COA has three key elements: a name that identifies what it tracks, a brief description of its purpose, and a unique numeric code that makes categorization fast and consistent. Those codes typically follow a five-digit format where each digit signals the account type and department, making it easier for anyone on your accounting team to locate and log transactions quickly.

Companies and institutions use a COA to separate revenues, expenses, assets, and liabilities. This separation is what allows financial statements to meet disclosure requirements and gives stakeholders, including investors, board members, auditors, and government agencies, a clear view of financial performance.

The Education Industry: A Quick Overview

Education is no longer a static sector. It spans pre-kindergarten through postgraduate study and includes private schools, public schools, charter schools, vocational training centers, language institutes, online learning platforms, and large research universities. In the United States alone, postsecondary education generates more than $400 billion in annual revenue. The private elementary and secondary school market adds another $86 billion to that figure.

Fast-growing markets in China, India, and Southeast Asia are expanding the global footprint of education even further, though many of these regions still struggle with literacy rates below 60 percent, which creates both a challenge and a massive opportunity for the sector.

Unlike a typical business, educational institutions don’t always measure success in profit. They measure it in outcomes, such as graduation rates, student performance, and community impact. That mission-focused orientation shapes how they track money, and it’s a core reason why education accounting differs from traditional business accounting.

Education Industry Sectors

The education sector is made up of four primary segments, and each one has distinct bookkeeping needs.

Schools and Service Providers cover elementary and secondary education, alternative school services, education management organizations, community colleges, virtual schools, and proprietary schools.

Supplementary Educational Services include higher education institutions, vocational training providers, academic advising firms, and assessment services.

Educational Products refers to companies producing and distributing textbooks, curriculum materials, software, and supplementary learning tools.

Educational Services covers support organizations such as education consultants, research bodies, policy experts, and technology providers that serve the broader sector.

Private Schools

Private schools operate independently from local, state, and federal governments. They select their own students and fund operations primarily through tuition fees rather than tax revenues. Some offer partial or full scholarships, but tuition remains the primary income stream. Private schools include religious institutions, military academies, international schools, and elite boarding schools. According to the National Association of Independent Schools, average US private day school tuition exceeded $26,000 in recent years, with boarding school tuition climbing to $60,000 or more per year.

Public Schools

Public schools are government-operated and funded through public tax revenue. They are open to all students within their jurisdiction and governed by a school board or equivalent body. Their mission is to provide universal access to quality education. Public schools report to government standards, including those set by the Governmental Accounting Standards Board (GASB), and many must submit data annually to the Integrated Postsecondary Education Data System (IPEDS).

In fiscal year 2017, the 50 US states reported $705.3 billion in revenues for public elementary and secondary education, with state and local governments providing approximately 92 percent of that total.

Traditional and Higher Education

Traditional university degrees require full-time enrollment at an accredited institution. Online degree programs typically don’t qualify under conventional definitions. Higher education institutions operate under complex financial structures that include endowment management, research grant accounting, federal financial aid administration, and multi-department budgeting, all of which demand a well-organized chart of accounts.

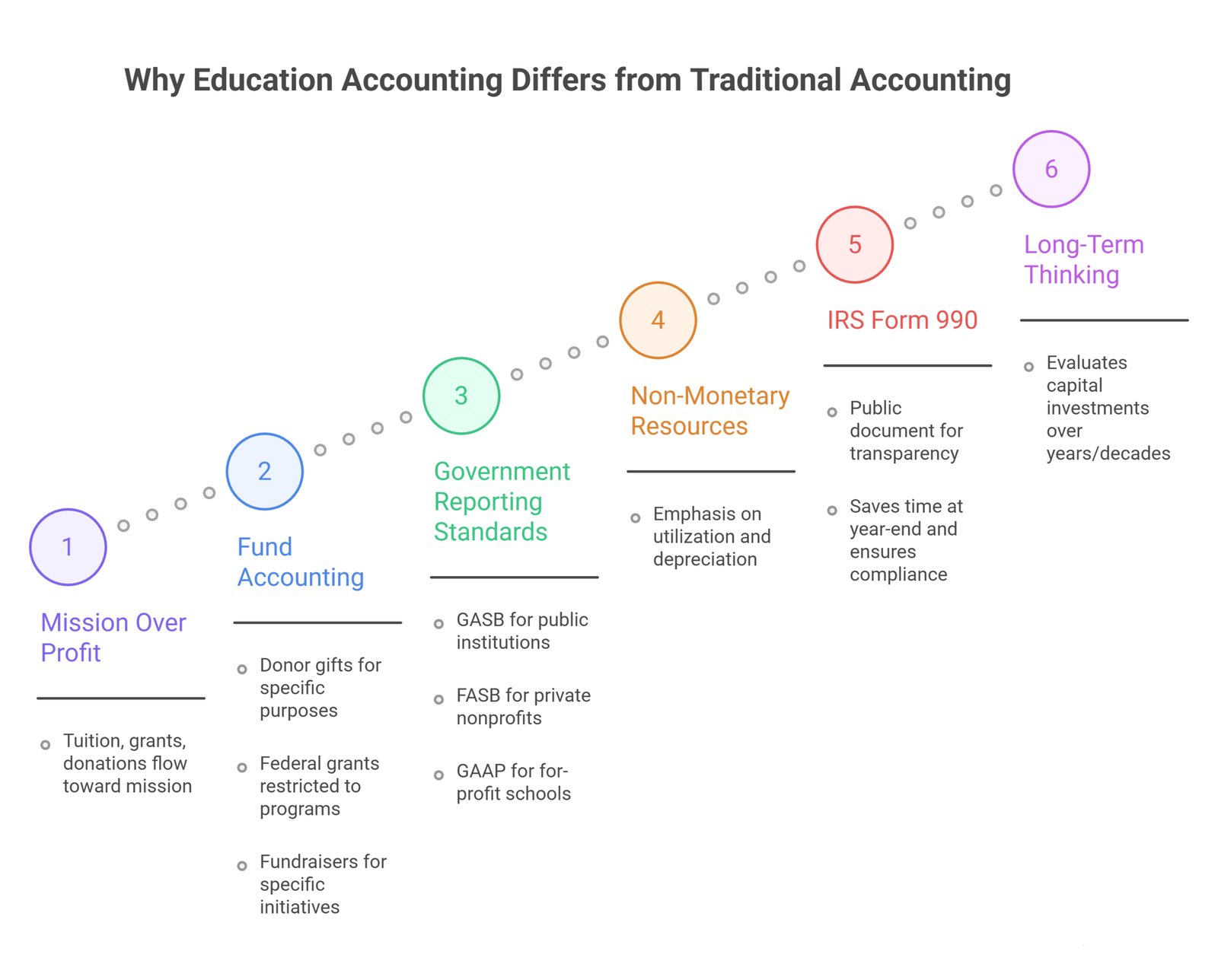

Why Education Accounting Differs from Traditional Accounting

If you’re coming from a standard business accounting background, a few things about education finance will catch your attention quickly.

Mission Over Profit: In traditional accounting, revenue exists to generate profit. In education accounting, revenue exists to fund a mission. Tuition, grants, and donations all flow toward educational programming rather than shareholder returns. This changes how income is prioritized and reported.

Fund Accounting: This is the most distinctive feature of education bookkeeping. Schools regularly receive money that’s earmarked for specific purposes: a donor’s gift designated for the computer lab, a federal grant restricted to Title I programs, or a fundraiser specifically for athletics. Fund accounting tracks these restricted funds separately from unrestricted operating funds, ensuring the money gets used exactly as intended and that the institution can demonstrate compliance.

Government Reporting Standards: Public schools and universities that receive federal or state funding must comply with GASB reporting guidelines. Private nonprofit institutions typically follow Financial Accounting Standards Board (FASB) standards. For-profit schools may follow generally accepted accounting principles (GAAP) similar to regular businesses. Understanding which framework applies to your institution is essential before building your chart of accounts.

Non-Monetary Resources: Schools manage classrooms, libraries, labs, athletic facilities, and specialized equipment. These assets are tracked differently than cash, with an emphasis on utilization rates and depreciation schedules rather than market value.

IRS Form 990: Nonprofit educational institutions are required to file Form 990 annually with the IRS. This public document reports income, expenses, and key organizational information. Accurate bookkeeping that maps directly to Form 990 categories saves enormous time at year-end and keeps the institution compliant.

Long-Term Thinking: Education accounting tends to favor decisions with long-term institutional impact over short-term financial performance. Capital investments in buildings or curriculum are evaluated over years and decades, not quarters.

The Chart of Accounts for Educational Institutions

The COA is, in simplest terms, a management tool. A well-built one makes it easier for your team to locate accounts, reconcile transactions, and generate meaningful reports. Crucially, your school’s COA doesn’t need to look like anyone else’s. Every institution has unique revenue streams, funding sources, and expense structures. A public school in a rural district looks nothing like a private boarding school or an online university, and the COA should reflect those differences.

That said, a solid framework applies to virtually every educational institution.

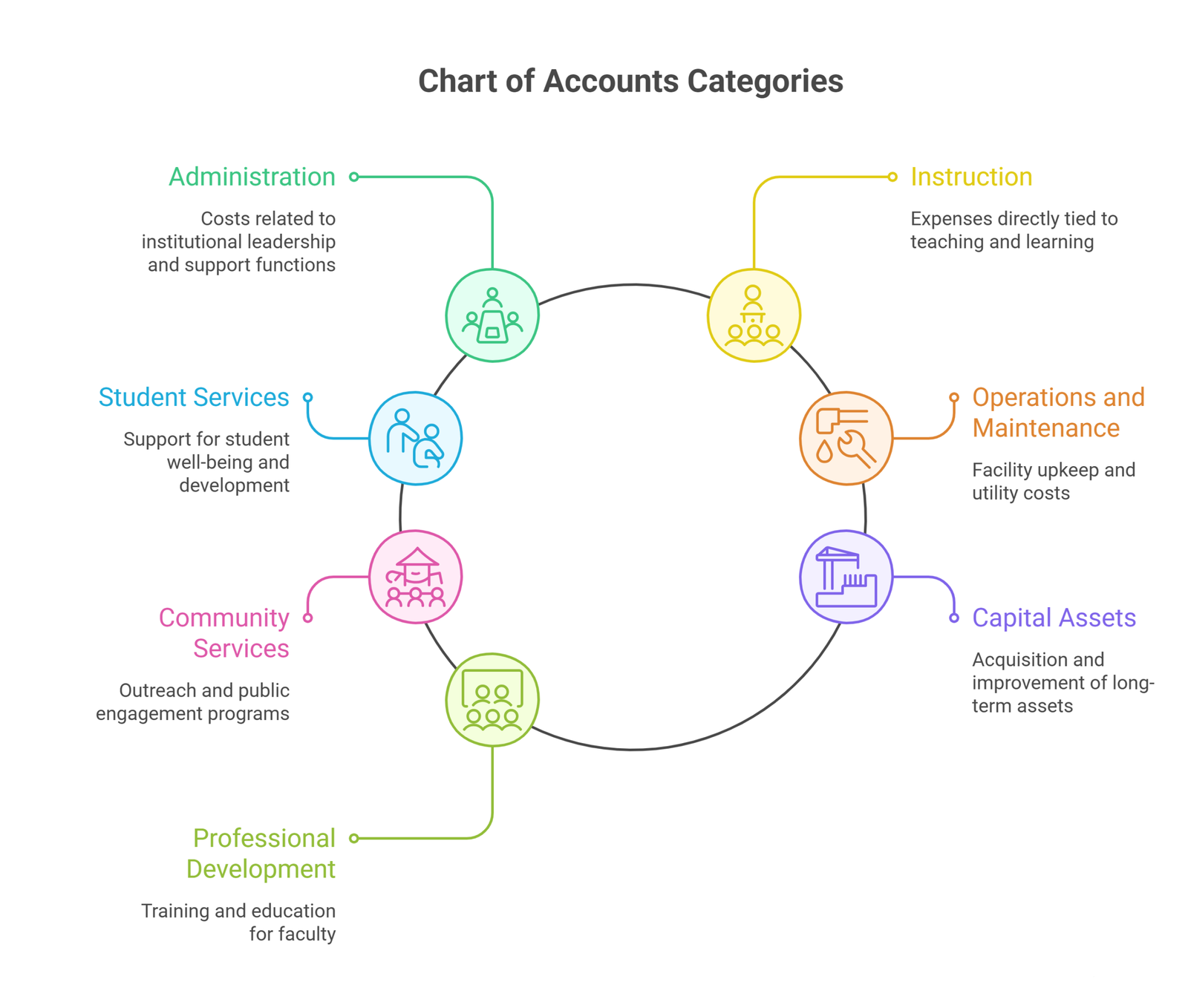

What to Include in the Chart of Accounts

The most effective COAs for schools are organized into clear categories that mirror the structure of standard financial statements. A typical education COA covers the following areas:

Administration tracks costs related to institutional leadership, HR, legal, and finance functions.

Instruction captures all costs directly related to teaching, including faculty salaries and classroom materials.

Student Services covers counseling, admissions, financial aid administration, and extracurricular support.

Operations and Maintenance records facility upkeep, utilities, janitorial services, and capital repairs.

Community Services tracks outreach programs, continuing education, and public events.

Capital Assets covers the acquisition, improvement, and replacement of long-term assets.

Professional Development captures faculty training, conferences, and continuing education costs.

Each account entry should include an account name that reflects its purpose, a brief description of what belongs in it, and a unique reference code. Five-digit codes are standard, with the first digit indicating the account category (1 for assets, 2 for liabilities, 3 for equity, 4 for revenue, 5 for expenses).

Chart of Accounts Groups

Balance Sheet Accounts

Current Assets

- 1010 Cash and Cash Equivalents

- 1020 Short-Term Investments and Marketable Securities

- 1030 Accounts Receivable (tuition owed, grants receivable)

- 1040 Prepaid Expenses

- 1050 Inventory (if applicable, such as school store or cafeteria)

Long-Term Assets

- 1510 Land

- 1520 Buildings and Facilities

- 1530 Furniture and Equipment

- 1540 Accumulated Depreciation (contra asset)

- 1550 Intellectual Property and Software

- 1560 Endowment Investments

Current Liabilities

- 2010 Accounts Payable

- 2020 Accrued Salaries and Wages

- 2030 Deferred Revenue (tuition paid in advance for future terms)

- 2040 Accrued Expenses

- 2050 Notes Payable (short-term)

Long-Term Liabilities

- 2510 Mortgage Payable

- 2520 Bonds Payable

- 2530 Long-Term Notes Payable

Equity

- 3010 Unrestricted Net Assets

- 3020 Temporarily Restricted Net Assets

- 3030 Permanently Restricted Net Assets (endowment principal)

- 3040 Retained Earnings (for for-profit institutions)

Income Statement Accounts

Revenue / Income

- 4010 Tuition and Fees

- 4020 Government Grants and Appropriations

- 4030 Private Grants and Contracts

- 4040 Contributions and Donations (unrestricted)

- 4050 Restricted Donations and Gifts

- 4060 Endowment Income

- 4070 Auxiliary Revenue (cafeteria, housing, bookstore)

- 4080 Interest and Investment Income

- 4090 Other Revenue

Operating Expenses

- 5010 Faculty Salaries and Wages

- 5020 Administrative Salaries

- 5030 Staff and Support Salaries

- 5040 Employee Benefits and Payroll Taxes

- 5050 Professional and Contracted Services

- 5060 Instructional Supplies and Materials

- 5070 Technology and Software

- 5080 Rent and Lease Payments

- 5090 Utilities

- 5100 Insurance

- 5110 Depreciation and Amortization

- 5120 Repairs and Maintenance

- 5130 Travel and Conference Expenses

- 5140 Marketing and Recruitment

- 5150 Financial Aid and Scholarships Awarded

- 5160 Research and Development

- 5170 Community Outreach and Programs

- 5180 Other Operating Expenses

Other Income and Expenses

- 6010 Gain or Loss on Sale of Assets

- 6020 Interest Expense

- 6030 Unrealized Investment Gains or Losses

Fund Accounting in Education

Fund accounting deserves its own section because it’s where most general-purpose bookkeeping systems fall short for educational institutions. The concept is straightforward: when money comes in with strings attached, it lives in a separate “bucket” from your regular operating funds, and you must track spending within that bucket to prove compliance.

There are three primary fund types in education:

Unrestricted Funds can be used for any operating purpose at the institution’s discretion. General tuition revenue typically flows here.

Temporarily Restricted Funds must be used for a specific purpose or within a specific time period. A grant to build a new science lab is temporarily restricted until the lab is complete and all funds are spent.

Permanently Restricted Funds are endowment principals that must remain intact. Only the investment income generated by these funds can be spent, and often only on designated purposes.

Your chart of accounts needs to accommodate this structure. Many institutions add a dimension or segment to each account code to indicate the fund it belongs to, keeping all activity organized without creating an unmanageable number of individual accounts.

Revenue Streams: What Education Institutions Track

Understanding your revenue sources is critical before you set up the income side of your COA. Education institutions typically draw from a broader range of income streams than most businesses.

Tuition and fees are the most visible source, but they’re rarely the only one. Grants from federal and state governments carry specific compliance requirements and must be tracked separately. Private grants from foundations come with their own reporting obligations. Endowment income is distributed according to a spending policy, usually a percentage of the portfolio’s three-year rolling average value. Auxiliary enterprises, which include student housing, food service, and campus bookstores, generate revenue that’s separate from academic operations. Donations from alumni and community members may be unrestricted or designated for specific programs.

Each of these income streams needs its own line in the chart of accounts, both to simplify reporting and to ensure the institution can demonstrate stewardship to every stakeholder group.

Deferred Revenue: A Common Bookkeeping Challenge

One area that often trips up education bookkeepers is deferred revenue. When a student pays tuition for the spring semester in December, that payment has been received but not yet earned. Under accrual accounting, which is the standard for most educational institutions, you don’t record it as revenue until the semester actually begins.

This means your COA needs a deferred revenue account under current liabilities. As the semester progresses and the service is delivered, amounts shift from deferred revenue to earned tuition revenue. Getting this right matters not just for accurate reporting, but for cash flow management and audit readiness.

Accounting Rules for Recording Expenses

In accrual-basis accounting, which the majority of educational institutions use, expenses are recorded when they’re incurred, not when they’re paid. If your faculty earn salaries in June but payroll doesn’t process until July 1, those salaries belong in June’s financials as an accrued liability.

This approach gives a much more accurate picture of your institution’s financial position at any given point than a cash-based method would. It’s also what most regulatory frameworks and auditors expect to see.

A few general rules worth keeping in mind:

Salaries are the single largest expense for most educational institutions, often accounting for 65 to 75 percent of total operating costs. Getting payroll coding right across departments and programs is critical.

Depreciation must be applied to all long-term assets. Equipment, buildings, and vehicles lose value over time, and that decline in value is a real expense that shows up on the income statement each year through depreciation.

Scholarships and financial aid awarded by the institution reduce net tuition revenue and should be tracked carefully. Many institutions net them against gross tuition, while others show them as a separate expense line. Either approach is acceptable, but consistency matters.

Operating Expense Accounts in Detail

Most of the interesting (and complex) action in education bookkeeping happens on the expense side. Here’s how the main categories typically break down in practice.

Instruction costs include faculty salaries and benefits, curriculum development, instructional technology, classroom materials, and lab supplies. These costs represent the core mission of any educational institution and usually receive the largest share of the operating budget.

Student services cover everything that supports students outside the classroom, including academic advising, counseling, career services, health services, tutoring programs, and student activity administration.

Institutional support captures the overhead of running the organization: executive leadership, legal and audit fees, human resources, financial management, and general administrative operations.

Facilities and operations account for maintaining the physical campus, including custodial services, utilities, security, groundskeeping, and routine repairs.

Technology has become a major and often underestimated expense category. Learning management systems, student information systems, cybersecurity infrastructure, and device management all belong here.

Practical Bookkeeping Tips for Educational Institutions

- Running clean books in an education environment takes more than a well-organized COA. A few practices make a meaningful difference.

- Reconcile accounts monthly without exception. Bank statements, payroll records, grant accounts, and investment holdings should all be reconciled every month. Catching discrepancies early prevents small errors from becoming audit findings.

- Use accounting software designed for fund accounting or at least one that can be configured for it. QuickBooks is widely used in smaller private schools and works well when set up correctly. Larger institutions often use more specialized platforms like Blackbaud Financial Edge, Sage Intacct, or PowerSchool.

- Maintain documentation for every restricted fund. For each grant or restricted donation, keep a file that includes the original award letter, the spending requirements, budget versus actual reports, and any required progress reports. Auditors will ask for this.

- Separate purchasing authority from payment authority. This basic internal control prevents fraud and errors by requiring two different people to approve and process each expenditure.

- Review your chart of accounts annually. Programs change, funding sources shift, and departments reorganize. Your COA should evolve with the institution. Accounts that haven’t seen any activity in two or three years can often be archived, and new ones may need to be added as operations grow.

- Train your staff. Bookkeeping accuracy depends on people coding transactions correctly the first time. A short training session on the COA and expense categories, especially for department budget managers, pays off quickly in cleaner financials.

Why a Solid Chart of Accounts Matters

A chart of accounts is more than an administrative necessity. It’s the foundation of every financial report your institution will produce, every budget decision your leadership will make, and every compliance filing your team will submit. For public institutions, it supports GASB reporting and IPEDS submissions. Moreover, for private nonprofits, it underpins FASB statements and Form 990 filings. For all institutions, it gives board members, accreditors, donors, and parents the transparency they need to trust that their investment in education is being managed responsibly.

Getting it right from the start is far easier than trying to clean it up later. Whether you’re setting up accounts for a new institution or restructuring an existing one, the investment of time in building a clear, purpose-built COA is one of the highest-return activities a school’s finance team can undertake.

Frequently Asked Questions

What is a standard chart of accounts for a school?

It is a structured index of every financial category in a school’s ledger. Using a numeric coding system, such as 1000s for Assets and 5000s for Expenses, it organizes money by department and fund type to ensure every dollar is traceable.

Why do schools use fund accounting?

Schools use fund accounting to track restricted money. Because donors and governments often earmark funds for specific uses like a new gym or a scholarship, fund accounting separates these financial buckets from general cash to prove the money was spent legally and as intended.

How is tuition recorded in the accounts?

Tuition is recorded via accrual accounting. When billed, it enters Accounts Receivable and Deferred Revenue. As classes are held over the semester, the money is moved to Earned Revenue. This accurately reflects income over the academic term rather than just when the check is signed.

What is the best bookkeeping software for schools?

Small schools often use QuickBooks Online for its affordability and ease of use. Mid-to-large institutions typically prefer Blackbaud Financial Edge or Sage Intacct because they are specialized for complex fund accounting. Enterprise-level universities often rely on Oracle NetSuite or PowerSchool to integrate financials with student data.

What is the difference between restricted and unrestricted funds?

Unrestricted funds are general income used for daily expenses like utilities or staff pay. Restricted funds come with specific requirements; temporarily restricted funds are for specific projects, while permanently restricted funds, such as endowments, stay in the bank forever with only the interest being spent.

Final Thoughts

The education sector will keep growing, and the financial complexity that comes with that growth will only increase. More revenue streams, more regulatory requirements, more stakeholder expectations. The institutions that navigate this landscape successfully are the ones that build strong financial systems early and maintain them with discipline.

A robust Chart of Accounts is the backbone of financial integrity. It is the difference between a school that simply ‘tracks spending’ and one that leverages data to secure its mission. If your current accounting structure is hindering your reporting or failing to meet compliance standards, it’s time for a professional recalibration.

Get a Free Accounting Consultation. Let our experts audit your current system and design a COA that delivers total transparency and audit-ready precision.