Mastering the Flow: A Deep Dive into the Waterfall Financial Model

The waterfall financial model: who gets paid first when a deal exits

When a private equity fund sells a portfolio company, or a real estate syndication refinances a property, the exit proceeds do not simply get divided evenly. They flow through a strict sequence of payment tiers called a distribution waterfall, and the order of that sequence determines whether an investor sees their money in month one or waits years for a general partner’s carried interest to clear first.

Understanding how a waterfall financial model actually works, tier by tier, with real numbers, is the difference between reading a fund’s offering documents and understanding what they mean for an investor’s cash.

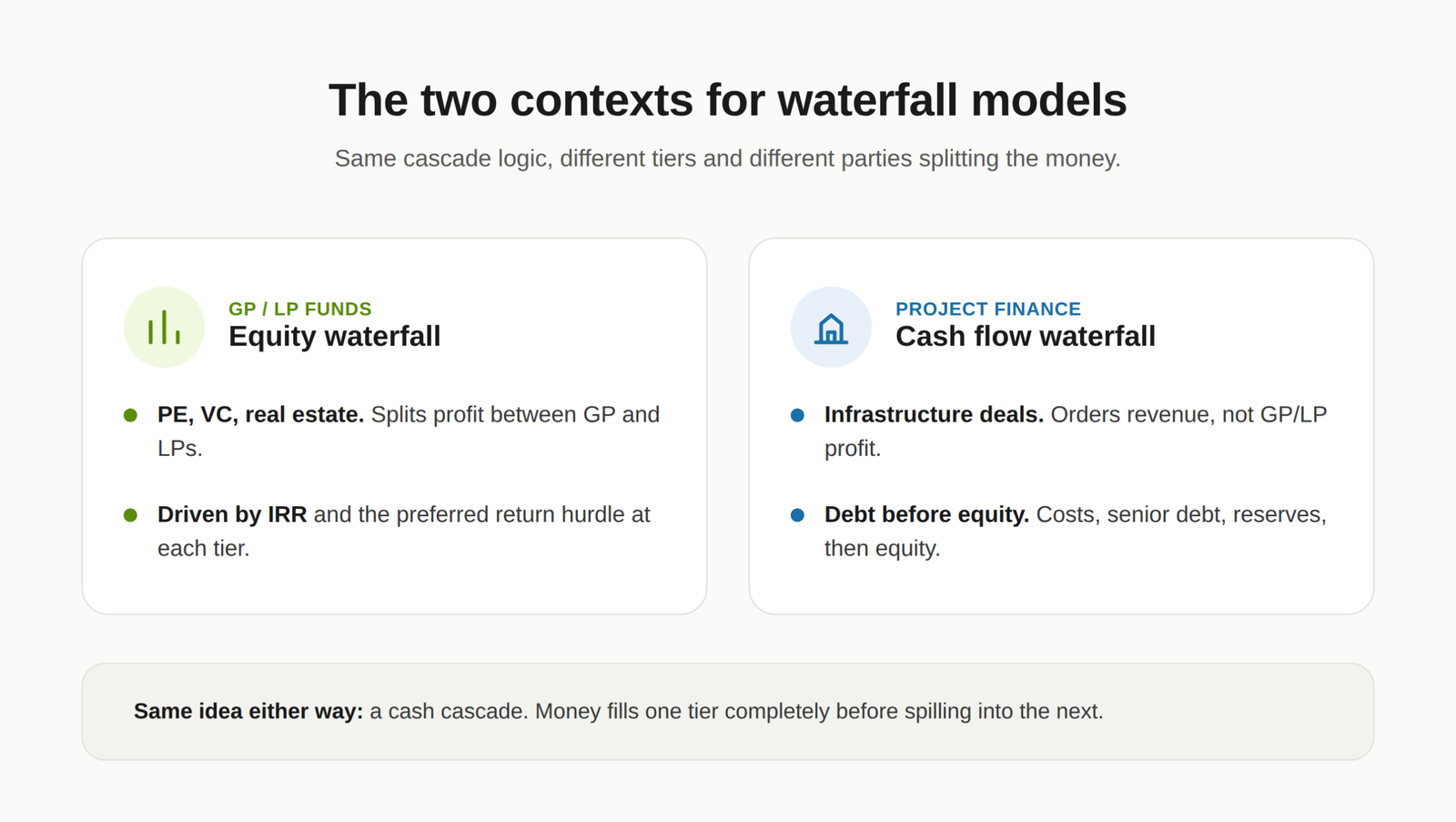

The two contexts where waterfall models show up

Finance professionals build waterfall models in two distinct settings, and the mechanics differ meaningfully between them.

Equity waterfalls govern private equity, venture capital, and real estate funds. They define how profits split between the general partner (GP), who manages the fund, and the limited partners (LPs), who supply the capital. Performance metrics like the internal rate of return (IRR) and the preferred return hurdle drive every tier.

Cash flow waterfalls show up in project finance and infrastructure deals. Instead of splitting profit between GP and LP, they dictate the order in which project revenue satisfies operating costs, senior debt, reserve accounts, and finally equity holders. Debt gets paid before equity sees a cent.

Both are often called a cash cascade, since money fills one tier completely before spilling into the next.

Equity waterfall tiers, in order

A standard private equity or real estate equity waterfall runs through four tiers.

| Tier | What happens | Purpose |

| 1. Return of capital | LPs receive 100% of distributions until their full initial investment is returned | Protects investor principal before anyone discusses profit |

| 2. Preferred return | LPs continue receiving 100% until they hit a pre-agreed annual return, typically 8% | Guarantees LPs a minimum return before the GP shares in profit |

| 3. GP catch-up | The GP receives most or all of the proceeds until their cumulative share matches their target carry percentage | Lets the GP “catch up” to their negotiated split, usually 20% |

| 4. Carried interest split | Remaining profit splits by an agreed ratio, commonly 80/20 LPs to GP | The final profit-sharing mechanism that rewards GP performance |

The catch-up tier is where most confusion happens, so a worked example makes it concrete.

A worked example: $100 million exit

Assume a fund sells a portfolio company for $100 million in proceeds, LPs contributed $80 million, the preferred return is 8% (simplified to one year), and the carry split is the standard 80/20 with a 100% catch-up.

| Step | Amount | What it covers |

| Return of capital to LPs | $80.0M | LPs recover their full contributed capital |

| Preferred return to LPs | $6.4M | 8% preferred return on the $80M contributed |

| GP catch-up | $1.6M | GP receives 100% until its cumulative share equals 20% of profit |

| Remaining 80/20 split | $12.0M | $9.6M to LPs, $2.4M to GP |

Result: LPs walk away with $96 million total. The GP earns $4 million in carried interest, all of it concentrated in tiers 3 and 4. Every dollar in tiers 1 and 2 went to protecting LP capital first. That sequencing, not the final split, is what a distribution waterfall actually models.

Not every LPA sets the catch-up at 100%. Some negotiate a 50% catch-up, which slows how quickly the GP reaches its target carry percentage and leaves more of the interim profit with LPs. This single term can shift outcomes by hundreds of thousands of dollars on a mid-sized exit, which is why it belongs on any due diligence checklist.

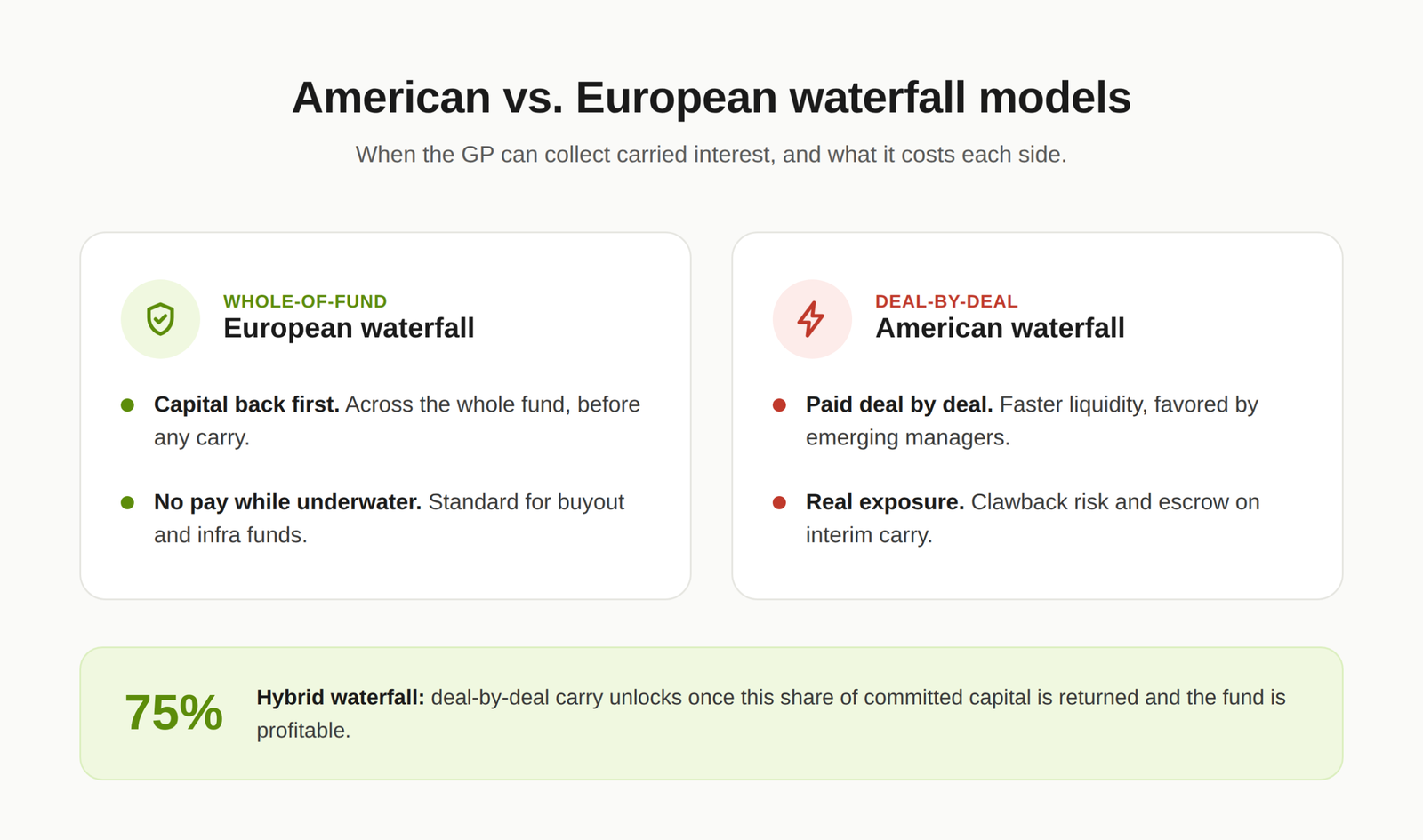

American vs. European waterfall models

The two structures differ in when the GP is allowed to collect carried interest, and the difference has real consequences for both sides.

European waterfall (whole-of-fund): LPs must receive their full return of capital and preferred return across every investment in the fund before the GP collects any carry. This is more investor-friendly because the GP cannot get paid while the fund overall is underwater, and it is now the standard for large buyout, infrastructure, and secondary funds.

American waterfall (deal-by-deal): The GP can collect carry on a single profitable deal as soon as that deal clears its hurdle, regardless of how other investments in the fund are performing. This gets the GP paid faster, which matters for emerging managers who need earlier liquidity, but it creates real exposure: clawback risk if later deals underperform, escrow locks on 20 to 30% of interim carry, and added tax-timing complexity.

Because of that exposure, most large institutional LPs push for European or hybrid structures. A hybrid waterfall releases deal-by-deal carry only after a threshold, commonly 75% of committed capital, has been returned and the fund overall is profitable, balancing early GP liquidity against LP protection.

Clawback provisions and how they actually get enforced

A clawback is the legal mechanism that forces a GP to return excess carried interest if, by the fund’s end, LPs did not receive their full agreed share. It matters most in American waterfalls, where a GP can be paid early on a strong deal only to see later deals disappoint.

Enforcement varies more than most people expect. Industry surveys on European buyout fundraising found that roughly 42% of funds escrow none of the GP’s interim carry, 25% escrow the full 100%, and the rest fall somewhere between 10% and 100%. That spread means “there’s a clawback provision” tells an LP very little on its own. The questions that matter are how often the clawback is tested, whether it’s capped at the lesser of excess carry or total carry received, and whether the GP provides an escrow account or a letter of credit as security.

Tiered carry and other structural variations

Flat 20% carry is common but no longer universal. Some LPAs now build in tiered carry, where the GP’s percentage steps up, to 25% or even 30%, once the fund clears a stronger performance threshold, such as a 2.5x or 3x multiple on invested capital. The logic is straightforward: reward outsized performance beyond what the base 20% already compensates for, without inflating the GP’s take on an average-performing fund.

Waterfalls also come into play when assets roll into a continuation fund during a secondary transaction. The original waterfall freezes, prior carry gets offset against the new vehicle’s terms, and secondary buyers typically insist on a full fund-level waterfall even for a single-asset continuation deal, to keep the GP’s incentives aligned over the extended hold period.

Cash flow waterfall: project finance and debt

Project finance waterfalls follow a different logic entirely, one built around debt seniority rather than profit sharing.

| Tier | Payment priority | Purpose |

| 1. Operating expenses | Day-to-day costs of running the project | Keeps operations funded |

| 2. Senior debt service | Interest and principal on the most senior loans | Protects the most senior lenders first |

| 3. Reserve accounts | Funds a debt service reserve account | Cash buffer against future shortfalls |

| 4. Subordinated debt | Interest and principal on junior debt | Repays lower-priority obligations |

| 5. Distributions | Remaining cash to equity sponsors | Final equity return, paid only after every debt tier clears |

Equity holders in a project finance deal are last in line by design. That structure is what makes senior debt in infrastructure and large-scale projects comparatively low-risk: five tiers of protection sit ahead of any equity distribution.

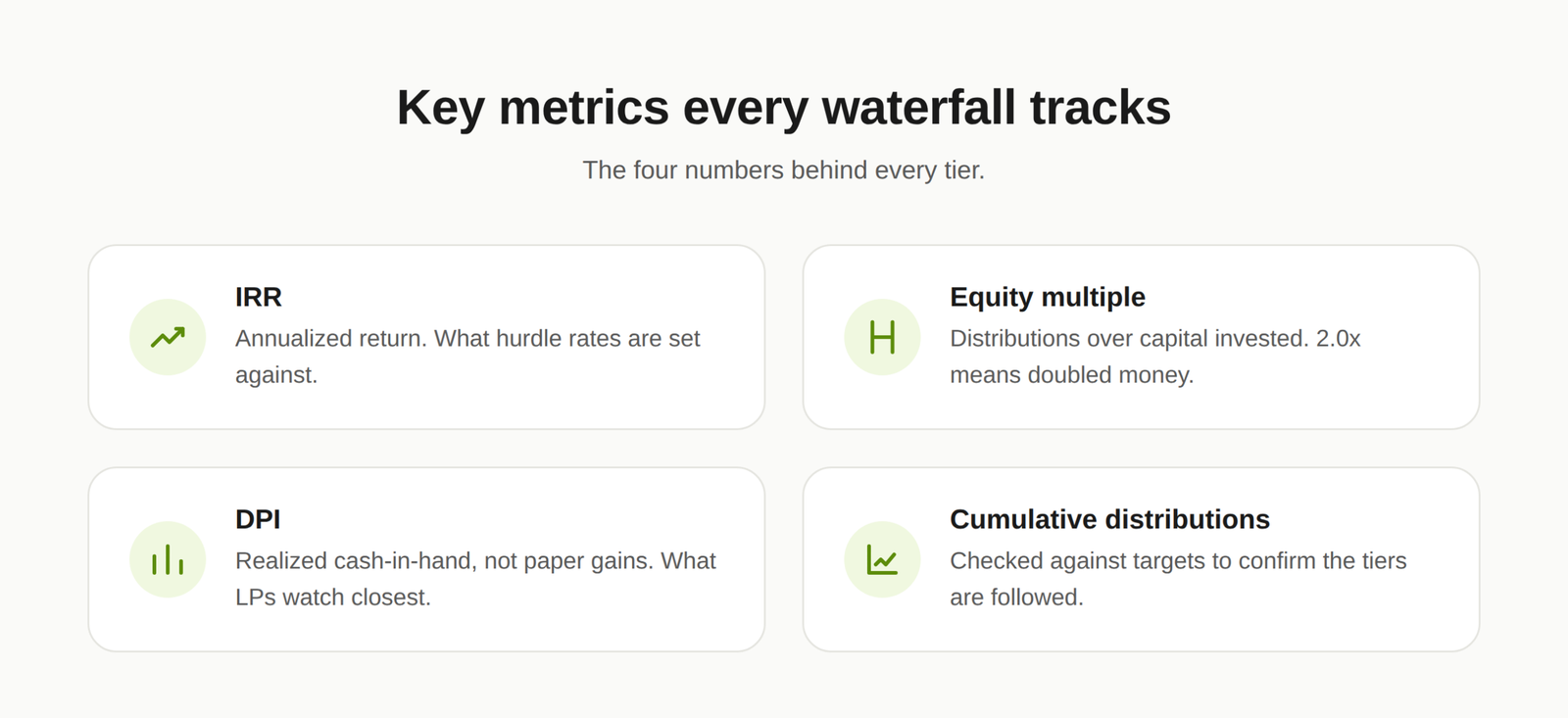

Key metrics every waterfall model tracks

- Internal rate of return (IRR): the annualized return on invested capital, and the basis most hurdle rates are set against.

- Equity multiple: total distributions received divided by total capital invested. A 2.0x multiple means an investor doubled their money, independent of how long it took.

- Distributions to paid-in capital (DPI): the ratio LPs watch most closely for realized, cash-in-hand performance, since it strips out unrealized, on-paper gains.

- Cumulative distributions: tracked against fund targets at every tier to confirm the waterfall is actually being followed as agreed.

Questions worth asking before signing an LPA

A waterfall’s fairness lives in details that are easy to skim past in a lengthy limited partnership agreement:

- Is the preferred return compounded annually, or calculated on a simple basis that quietly favors the GP?

- Is the catch-up set at 50% or 100%, and how much does that shift the GP’s early economics?

- What percentage of interim carry is escrowed, and for how long?

- Are broken-deal costs and fund expenses included in the clawback calculation, or excluded in the GP’s favor?

- Does recycled capital reset the hurdle calculation, or count as fresh capital?

Vague or missing answers to any of these are a legitimate reason to push back before capital gets committed.

Frequently Asked Questions

Why do funds use a preferred return and hurdle rate?

The preferred return protects LP capital by guaranteeing a minimum annual return, commonly 8%, before the GP can share in profit through carried interest. It aligns the GP’s incentives with actually growing LP capital, not just generating any return.

What is a GP catch-up, and why does the percentage matter?

The catch-up lets the GP receive a disproportionate share of profit after the preferred return is paid, until their cumulative take matches their target carry, typically 20%. A 100% catch-up gets the GP there faster than a 50% catch-up, which materially changes how much of the interim profit LPs keep.

Is a European or American waterfall better for investors?

European (whole-of-fund) waterfalls are generally more LP-friendly, since the GP cannot collect carry until the entire fund clears its hurdle. American (deal-by-deal) waterfalls pay the GP earlier but expose LPs to clawback risk if later deals underperform.

What is DPI, and why do LPs track it separately from IRR?

DPI, distributions to paid-in capital, measures actual cash returned to LPs relative to capital invested. Unlike IRR, which can be inflated by unrealized valuations, DPI only counts money that has actually been distributed.

Do clawback provisions guarantee LPs get overpaid carry back?

Not automatically. Enforcement depends on escrow terms negotiated in the LPA. Some funds escrow none of the GP’s interim carry, others escrow the full amount, and a clawback is only as reliable as the security backing it.

What is a hybrid waterfall structure?

A hybrid waterfall blends elements of both models, commonly releasing deal-by-deal carry only after a set percentage of committed capital, often 75%, has been returned and the fund is showing an overall profit. It’s a middle ground between GP liquidity and LP protection.

Conclusion

The waterfall model is the mechanism that turns a fund’s profit into an actual sequence of payments, and the specific terms embedded in each tier, the catch-up percentage, the escrow terms, the American-versus-European choice, determine who bears risk and who gets paid first. Getting the model built correctly, with every tier and hurdle reflecting the actual LPA language, is not optional if a fund wants clean, defensible reporting to its investors.

Building a waterfall model by hand in a spreadsheet leaves too much room for a broken formula to misstate a GP’s carry or an LP’s distribution. Oak Business Consultant builds investor-ready financial models with the scenario analysis and formula integrity that complex distribution structures require, including models built specifically for real estate and venture capital funds. Contact us to build a waterfall model your investors can trust.