What are some Key Components of Successful Budgeting?

Key Components of Budgeting

Most people have made a budget at least once. They sat down, wrote out their income, listed their bills, maybe used a spreadsheet or a budgeting app, and felt genuinely good about it. Then, three weeks later, they stopped looking at it.

This is not a discipline problem. It is a design problem. Budgets that fail do so because they are missing one or more of the core components that make them actually functional in real life. When those components are in place, a budget stops being a chore and starts being something that quietly works in your favor whether you are thinking about it or not.

This guide breaks down what those components are, why each one matters, and how they connect to each other. Whether you are building a personal budget from scratch, rethinking the way you manage business finances, or trying to figure out why your current budget keeps slipping, this is the foundation you need.

Why Budgeting Is More Than Just Tracking Numbers

Before getting into the components themselves, it helps to understand what a budget is actually doing. At the surface level, it tracks money coming in and money going out. But that description undersells it considerably.

A budget is a decision made in advance. Every time you sit down and allocate money toward rent, groceries, savings, debt, or anything else, you are making a choice about what matters to you before the emotion of the moment gets involved. That is what makes budgeting powerful. You are not reacting to your finances; you are directing them.

People who say they do not have enough money to budget often have things backwards. Budgeting is most important when money is tight because it forces clarity about priorities. When you have to choose between keeping a streaming subscription and contributing to an emergency fund, a budget makes that choice explicit. Without one, the subscription wins by default every time because it is the easier decision.

The same logic applies in business. A company that does not budget is constantly playing catch-up, unsure whether it can make payroll next month or afford a piece of equipment it genuinely needs. A company that budgets has already answered those questions before they become crises.

The Key Components of Successful Budgeting

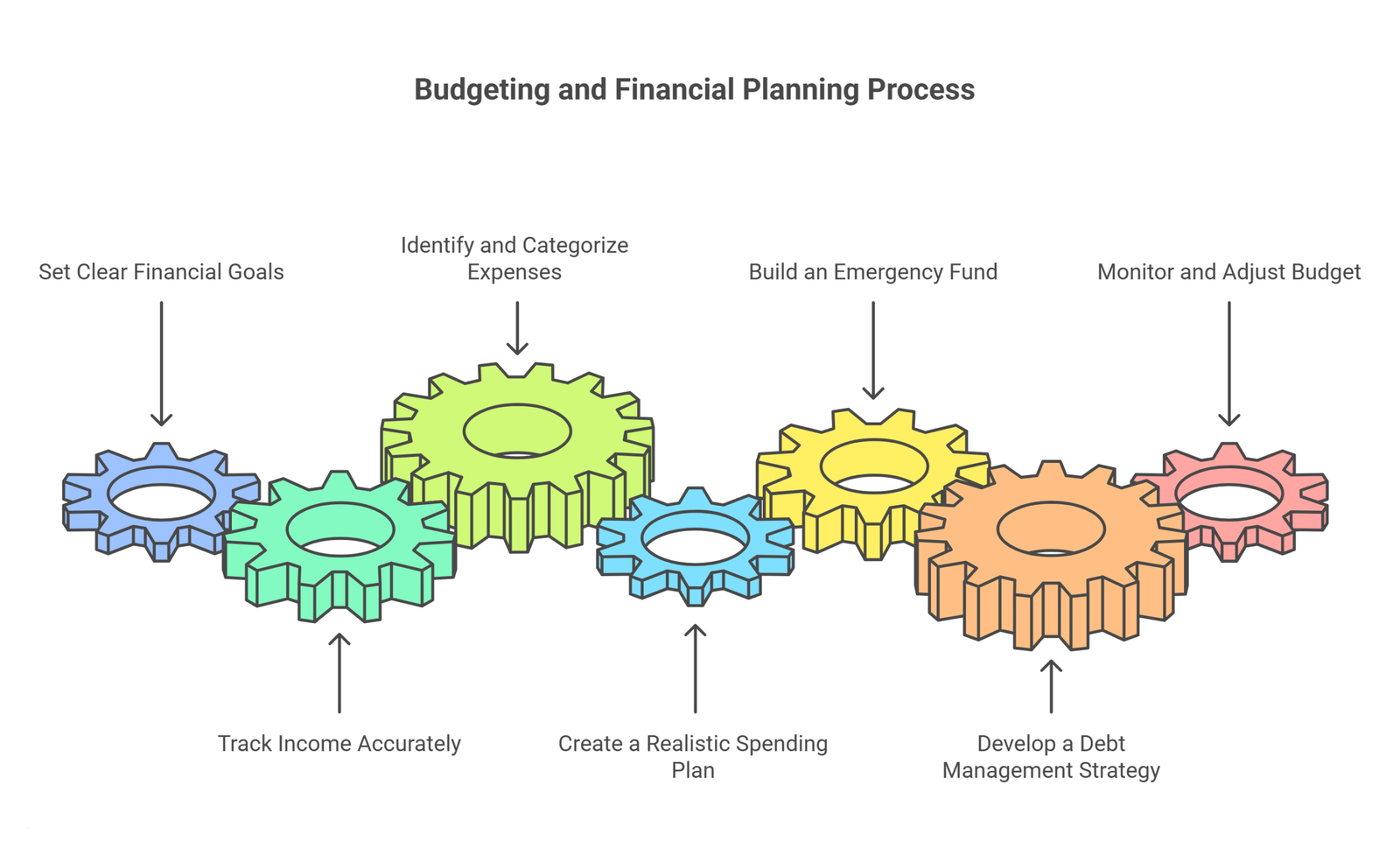

1. Clear, Specific Financial Goals

Every budget needs a reason to exist. Without goals, a budget is just an accounting exercise. With goals, it becomes a tool for building something you actually want.

The problem is that most people keep their goals vague. “Save more money” is not a goal. “I want to build a six-month emergency fund of $12,000 over the next two years” is a goal. The specificity is what makes it actionable because you can now calculate exactly how much you need to set aside each month ($500) and track your progress against a clear target.

Financial goals generally fall into three timeframes. Short-term goals are things you want to accomplish within about a year, such as paying off a credit card, building an initial emergency fund, or saving for a vacation. Medium-term goals take one to five years, like saving a down payment for a home, replacing a car, or clearing student loans. Long-term goals sit further out and include retirement savings, funding a child’s education, or building a business.

Most people need goals in all three categories because they serve different purposes psychologically. Short-term goals give you quick wins that keep you motivated. Long-term goals give you a sense of direction and meaning. Medium-term goals bridge the two.

One thing many budgeting guides miss is that your goals need to be genuinely yours. A goal that exists because someone else said you should have it will not survive the first month something tempting competes with it. If you actually want to take your family on a trip to Japan, that goal has emotional weight behind it. “I should probably save more” does not.

Write your goals down. Revisit them every few months. When your circumstances change, update them. Your budget should always be working toward something real.

2. Accurate, Complete Income Tracking

You cannot allocate money you have not counted. This sounds obvious, but income tracking is where a surprising number of budgets go wrong, usually not because of dishonesty but because of oversight.

For someone with a single salaried job, income tracking seems simple. But even then, there are things to watch: overtime pay, quarterly bonuses, tax refunds, occasional freelance income, rental income from a room or property, or interest earned on savings accounts. None of these are huge individually, but if you leave them out, your budget does not reflect your actual financial reality.

For people with variable income, whether freelancers, commission-based workers, small business owners, or anyone with irregular pay schedules, income tracking requires a slightly different approach. The safest method is to use a conservative baseline based on your lowest-earning months rather than your average. If you earn more than that baseline in a given month, you can treat the extra as bonus income to direct toward savings, debt, or other goals. This way, your budget remains functional even during lean months.

One thing worth emphasizing: always use net income, meaning what actually lands in your bank account after taxes, retirement contributions, health insurance premiums, and other deductions. Using gross income is a common mistake that leads to budgets that look fine on paper but consistently fall short in practice.

For businesses, income tracking also means understanding the difference between revenue and cash in hand. A business can look profitable on paper while struggling with cash flow if invoices are slow to be paid. A good business budget accounts for timing, not just amounts.

3. Thorough Expense Identification and Categorization

Once you know what comes in, you need a complete picture of what goes out. Most people underestimate their expenses by 20 to 30 percent when they try to recall them from memory. The only reliable way to get an accurate number is to look at actual transaction history, ideally for the past three months, and categorize every purchase.

Expenses generally split into two types. Fixed expenses are the costs that stay roughly the same every month regardless of what you do: rent or mortgage payments, loan repayments, insurance premiums, and regular subscription services. These are predictable and often hard to change in the short term, though they are worth reviewing periodically because many people are paying for things they have forgotten about or no longer use.

Variable expenses are where most of the real budgeting work happens. These fluctuate based on your behavior and circumstances: groceries, dining out, fuel, entertainment, clothing, home maintenance, and personal care. They tend to creep upward over time without anyone noticing, and they are also where you have the most flexibility to make adjustments when you need to.

There is a third category that both personal and business budgets frequently overlook: irregular or infrequent expenses. These are things that do not appear every month but are entirely predictable over the course of a year. Car registration, annual insurance payments, quarterly tax bills, holiday spending, back-to-school costs, and home maintenance repairs all fall here. When these are not budgeted for in advance, they feel like emergencies even though they are not. The solution is to estimate the annual cost of each irregular expense, divide by 12, and set that amount aside monthly into a dedicated savings bucket or sinking fund so the money is ready when you need it.

4. A Realistic Spending Plan

Having categorized your income and expenses, the next step is building the actual spending plan: deciding in advance how much goes to each category every month. This is the part most people think of when they say “making a budget,” but it works far better when the previous components are already in place.

A spending plan needs to be realistic above all else. The most common reason budgets fail is not a lack of willpower but the fact that the budget was built on wishful thinking. If you have been spending $600 a month on groceries and you set your grocery budget at $300 because you think you should spend less, you are not going to suddenly spend $300. You are going to hit $500, declare the budget a failure, and stop looking at it.

Several budgeting frameworks can help structure a spending plan. The 50/30/20 rule is widely cited and suggests allocating 50 percent of take-home income to needs, 30 percent to wants, and 20 percent to savings and debt repayment. This is a useful starting point but not a universal rule. Someone with a high debt load may need to direct 30 or 40 percent toward debt repayment. Someone living in an expensive city may find that needs alone consume 65 percent of income. Use frameworks as reference points, not rigid rules.

For businesses, a spending plan takes a slightly different form, usually built around revenue projections and cost budgets by department or category, with clear targets for gross margin and operating expenses. The principle is the same: decide in advance how money will be allocated so that spending decisions are made deliberately rather than reactively.

5. An Emergency Fund

An emergency fund is not optional. It is the component that separates a budget that is resilient from one that falls apart the first time anything unexpected happens.

The purpose of an emergency fund is straightforward: it is money set aside in an accessible account specifically for genuine, unplanned expenses. A sudden medical bill, an urgent car repair, an appliance that breaks down, or a period of reduced income all qualify. The emergency fund means these events do not become financial crises and do not require you to go into debt or raid other savings to cover.

The common recommendation is to maintain three to six months of essential living expenses in an emergency fund. For someone with very stable employment and low financial risk, three months may be sufficient. For someone who is self-employed, has variable income, or works in an industry prone to layoffs, six months or more makes sense.

If you are starting from zero, the immediate goal is to build a starter emergency fund of $500 to $1,000. This is enough to handle most minor unexpected expenses and buys you breathing room while you build toward a fuller cushion. From there, treat regular emergency fund contributions as a non-negotiable line in your budget until you reach your target.

One point many guides gloss over: the emergency fund only works if it is kept separate from your regular spending accounts and if you are disciplined about what counts as an emergency. A planned vacation is not an emergency. A sale on shoes is not an emergency. Using the fund for non-emergencies and not replenishing it leaves you exposed when a real emergency arrives.

6. A Debt Management Strategy

Debt is not just a financial burden. It is a budget burden, because every dollar going toward interest payments is a dollar that cannot go anywhere else. Having a clear strategy for managing and reducing debt is an essential part of any serious budget.

The first step is getting a complete picture of what you owe: every loan, every credit card balance, every line of credit, the outstanding balance, the interest rate, and the minimum payment. Most people have a rough sense of this but have not looked at the full picture in a single place.

From there, the two most widely discussed payoff strategies are the avalanche method and the snowball method. The avalanche method directs extra debt payments toward the highest-interest debt first while maintaining minimums on everything else. Mathematically, this is the most efficient approach because it minimizes total interest paid. The snowball method directs extra payments toward the smallest balance first, creating faster wins and psychological momentum. Research suggests the snowball method works better for people who struggle to stay motivated, even though it costs more in interest.

Beyond strategy, the key is to make debt repayment a budget line item rather than something you do with whatever is left over. When debt repayment is treated as a priority expense, it happens consistently. When it is an afterthought, it gets crowded out by other spending.

As debt decreases, the money previously going toward interest and repayment gets freed up to direct toward savings and goals. This is one of the most motivating parts of long-term budgeting: watching the monthly cash flow gradually improve as old debts disappear.

7. Consistent Monitoring and Regular Adjustment

A budget is not a document you create once and file away. It is a living tool that needs to be checked against reality on a regular basis.

The simplest monitoring habit is a monthly budget review, which does not need to take long. At the end of each month, compare what you planned to spend in each category against what you actually spent. Look for the gaps. Where did you overspend? Where did you underspend? What unexpected expenses came up? What worked and what did not?

This review process is not about judging yourself for overspending. It is about gathering information. If you consistently overspend on groceries, that tells you either the budget is unrealistic and needs to be raised, or there is a specific behavior pattern (impulse buying at the store, not planning meals, throwing out food) that can be addressed with a concrete change.

Beyond the monthly check, a more thorough quarterly review is useful for looking at bigger-picture questions: Are you on track toward your goals? Have your income or expenses changed significantly? Do your priorities need to shift? Has anything happened in your life that the budget has not caught up with yet?

Annual reviews are the time to look at the full year’s patterns, update your goals, reassess your emergency fund target, and think ahead to large expenses you know are coming in the next twelve months.

Life changes. Job changes, relationship changes, a new child, moving to a new city, a health event, a significant pay raise or cut: any of these can make a previously working budget obsolete almost overnight. The ability to adapt your budget quickly is what makes it durable over years rather than weeks.

What Most Budgeting Guides Leave Out: The Behavioral Side

The mechanics of budgeting are not complicated. Arithmetic is not the hard part. What makes budgeting difficult is the behavioral and psychological dimension, and most guides barely address it.

Spending is emotional. People buy things because they are stressed, bored, celebrating, socializing, or seeking comfort. None of those drives go away because you made a spreadsheet. A budget that ignores emotional spending patterns will keep being disrupted by them.

A few things help. First, building some breathing room into your budget matters more than most people think. A budget with zero discretionary money is one bad day away from collapse. Including a reasonable amount for things you enjoy and want means you are not constantly white-knuckling your way through the month.

Second, automating the high-priority pieces removes willpower from the equation entirely. If your savings contribution, emergency fund deposit, and debt payment all happen automatically on payday, they cannot be crowded out by other spending because the money is already gone before you make any other decisions.

Third, identifying your specific spending triggers helps you plan around them. If you tend to overspend when you shop for groceries while hungry, the solution is not more self-discipline. It is eating before you shop. Understanding the pattern makes the intervention obvious.

For families and couples, budgeting also requires genuine communication and shared ownership. A budget that only one person in a household manages and understands almost always creates tension. When both partners understand the financial picture and have agreed on priorities together, the budget becomes a shared tool rather than a source of conflict.

Putting It All Together: The Components Working as a System

Each of the components above does important work on its own, but the real power comes from how they connect.

Clear goals give your income tracking a purpose. Categorized expenses reveal where money is going and where your spending plan can be more intentional. Your spending plan turns goals into monthly actions. The emergency fund protects the whole system from unexpected disruptions. Your debt strategy clears away a drag on your cash flow that improves over time. And regular monitoring keeps everything aligned as life changes around you.

When any one component is missing, the system weakens in a specific way. Without goals, there is no motivation to stick to the plan. Without accurate income tracking, allocations are made on a false foundation. Moreover, without expense categorization, spending patterns stay invisible. Without an emergency fund, one unexpected event derails everything. Additionally, without a debt strategy, interest quietly erodes progress. Without regular monitoring, the budget drifts out of alignment with reality and gets abandoned.

The good news is that you do not need to build all of this perfectly from day one. Start with what you can do right now: write down your financial goals, look at three months of bank statements, and build a basic spending plan. Add the other components over the following months as you develop the habit. A budget that is 70 percent complete and actually being used is far more valuable than a perfect budget sitting untouched.

A Note on Budgeting for Businesses

Much of what is described above applies as directly to small business budgeting as it does to personal finance. The core logic is identical: know what comes in, know what goes out, make intentional decisions in advance, and review regularly.

Business budgets typically operate at a more complex level, with revenue broken down by product, service, or client; costs split between cost of goods sold and operating expenses; and projections that need to account for seasonality, growth, and market conditions. But the fundamental discipline is the same.

One area where business budgets differ from personal ones is in the relationship between budget and strategy. A personal budget is primarily a tool for stability and goal achievement. A business budget also serves as a planning document that reflects strategic priorities: where investment is being made, what growth is expected, and how performance will be measured. When a business budget is built well, it is not just a cost-control tool; it is a map for where the company is going.

If you are running a business and want to build financial systems that actually support growth, working with a CFO or financial consultant can bridge the gap between basic bookkeeping and genuine strategic financial planning.

Frequently Asked Questions

How often should I review my budget?

A monthly check-in is the minimum, comparing actual spending to planned amounts and noting where adjustments are needed. A more thorough quarterly review is useful for tracking progress toward goals and making larger changes. An annual review covers the full year’s patterns and sets up the coming year.

What is the best budgeting method?

There is no universal best method. The 50/30/20 rule is a useful framework. Zero-based budgeting, where every dollar is assigned a purpose, works well for people who want tight control. The envelope method helps with discretionary categories that tend to overspend. The right method is the one you will actually use consistently.

How do I budget when my income varies month to month?

Base your spending plan on a conservative estimate of your minimum expected income. When you earn more than that in a given month, direct the surplus toward your highest-priority goal: filling your emergency fund, accelerating debt repayment, or building savings. This way, your budget works even in low-income months and progress accelerates when income is higher.

Is budgeting only for people with financial problems?

Not at all. Budgeting is equally valuable at every income level. Higher income creates more options and more complexity, not less need for intentional planning. Without a budget, income growth often leads to lifestyle inflation rather than meaningful financial progress.

What role does an emergency fund play in a budget?

It is the safety net that protects everything else. Without one, any unexpected expense disrupts the budget and often forces debt. With one, minor crises are manageable inconveniences rather than financial disasters. The target is three to six months of essential living expenses, built gradually as part of the regular budget.

Conclusion

Budgeting done well is not restrictive. It is clarifying. It takes the daily noise of financial decisions and organizes them into a coherent picture of where you stand, what you are working toward, and what you need to do next. That clarity is worth far more than the time it takes to build and maintain.

The key components covered here, clear goals, accurate income tracking, complete expense categorization, a realistic spending plan, an emergency fund, a debt strategy, and consistent monitoring, work together as a system. Build them one at a time if you need to, but build them.At Oak Business Consultant, we work with businesses at every stage of this process, from setting up basic financial systems to complex financial modeling and CFO-level strategic planning. If you want support building a budgeting framework that actually holds up over time, our team is here to help. Contact us today for a free consultation.