The Impact of Tax Planning on Business Strategies

Tax Planning: What You Need to Know?

Tax planning is not just an annual ritual that businesses rush through before tax season. It is one of the most powerful levers a business owner can pull to shape long-term financial outcomes, protect profit margins, and fund sustainable growth. When done right, tax planning becomes an integral part of every major business decision from hiring and equipment purchases to retirement planning and business succession.

This guide breaks down exactly how tax planning influences business strategies, what tools and approaches are available to you, and why getting proactive about your tax situation is one of the smartest investments you can make.

What Is Tax Planning — and Why Does It Go Far Beyond Filing Returns?

Most business owners think about taxes reactively. They gather financial records, hand them to an accountant, and hope for the best. But that approach leaves significant money on the table.

Tax planning is the ongoing process of analyzing your financial situation through the lens of current tax laws to minimize your tax obligations legally and strategically. It considers your business structure, revenue timing, investment decisions, retirement planning goals, and long-term exit strategy all at once.

The businesses that grow fastest are rarely the ones with the highest revenue. They are the ones that keep the most of what they earn. That is the promise of effective tax planning.

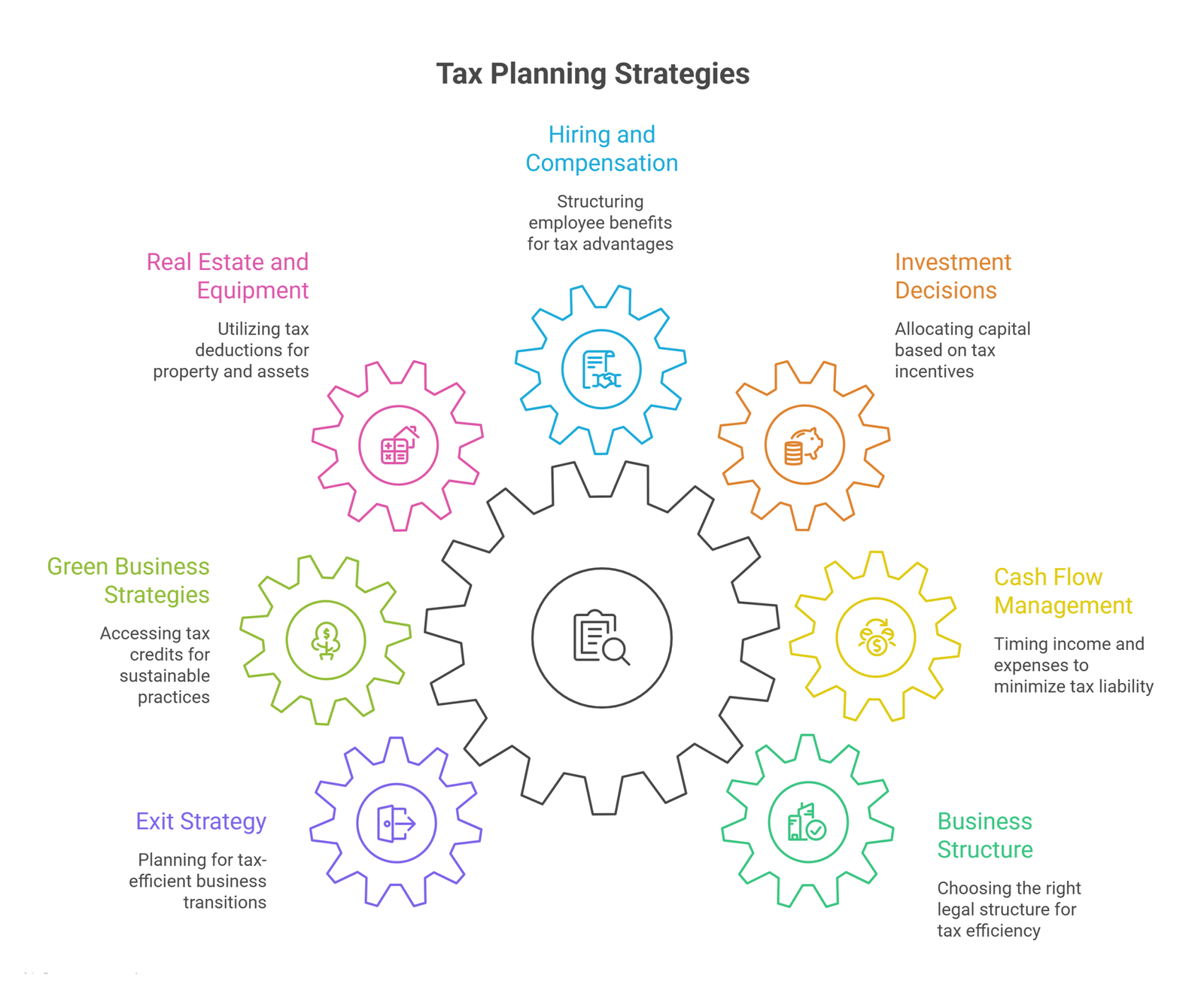

How Tax Planning Shapes Core Business Strategies

1. Business Structure Decisions

The business structure you choose sole proprietorship, partnership, S-Corp, C-Corp, or LLC has profound tax implications that ripple through every year of operations. A C-Corp faces double taxation on dividends, while an S-Corp passes income through to shareholders and avoids that layer. An LLC offers flexibility in how it is taxed.

Tax planning forces business owners to evaluate these structures not just at formation but as the company evolves. A small business that starts as a sole proprietorship might benefit enormously from converting to an S-Corp once net profits exceed a certain threshold, reducing self-employment tax significantly. A growing company considering outside investment might choose a C-Corp structure specifically to take advantage of Qualified Small Business Stock (QSBS) exclusions under the Internal Revenue Code.

Choosing or changing your business structure is not just a legal decision, it is a tax planning decision with multi-year financial consequences.

2. Cash Flow Management and Timing

Cash flow management and tax planning are deeply connected. When you recognize income, when you pay expenses, and how you time major financial transactions can shift your taxable income between years, and that timing can be the difference between a lower or higher tax bracket.

For example, a business expecting a higher-income year might accelerate deductible expenses into that year and defer invoicing until January to push revenue into the next tax year. This is a classic form of income deferral that directly affects cash flow management strategy.

Businesses using accrual accounting have different timing flexibility than those using cash-basis accounting. Understanding these nuances is a core part of tax-efficient strategies for growing companies. Proactive quarterly estimated tax payments also prevent cash flow shocks and penalties, keeping the business financially stable throughout the year.

3. Investment Decisions and Capital Allocation

Tax planning heavily influences investment decisions. Business owners who understand the tax code make very different choices about where to allocate capital.

Take Section 179 expensing. Under current tax laws, businesses can immediately deduct the full cost of qualifying equipment purchases rather than depreciating them over many years. This dramatically changes the calculus of whether and when to invest in new assets. A business that plans its equipment purchases in a high-income year can use Section 179 to slash its taxable income significantly.

Bonus depreciation provisions, cost segregation studies on commercial real estate, and the R&D tax credit are other examples where understanding the tax code directly shapes investment strategies. A manufacturer who overlooks the R&D tax credit might be leaving tens of thousands of dollars in unclaimed tax credits on the table each year.

Similarly, opportunity zone investments offer powerful tax incentives for businesses willing to deploy capital into designated low-income communities. These investment strategies are only viable when a business is actively doing tax planning and identifying these options in advance, not after the year closes.

4. Hiring, Compensation, and Retirement Planning

How you pay yourself and your employees is a tax planning decision. Owner compensation in an S-Corp must be a “reasonable salary”, too low and the IRS may reclassify distributions, too high and you eliminate the tax savings of pass-through income.

Beyond compensation, retirement planning vehicles like a SEP IRA, SIMPLE IRA, Solo 401(k), or Traditional IRA offer powerful ways to reduce taxable income while building long-term wealth. A self-employed business owner contributing the maximum to a SEP IRA can deduct up to 25% of net self-employment income, a significant tax reduction strategy that also builds financial stability.

For small business owners, these retirement planning strategies can reduce taxable income by tens of thousands of dollars annually. Yet many owners forgo them simply because no one has sat down and done the tax planning analysis.

Employee benefit programs health insurance, HSAs, dependent care FSAs also generate tax deductions for the business while reducing employees’ taxable income. A tax-savvy small business can structure compensation packages that are more valuable to employees at a lower after-tax cost to the company.

5. Real Estate and Equipment Strategy

Businesses that own real estate have access to powerful tax planning tools like cost segregation studies. Rather than depreciating a commercial building over 39 years, a cost segregation study reclassifies components of the property flooring, fixtures, land improvements into shorter depreciation schedules of 5, 7, or 15 years. The result can be hundreds of thousands of dollars in accelerated deductions in the early years of ownership.

Similarly, deliberate timing of equipment purchases around Section 179 and bonus depreciation limits allows businesses to manage their tax obligations strategically. A business that buys $500,000 in machinery in December rather than January can dramatically shift its current-year taxable income.

These are not loopholes, they are legitimate provisions in the tax code designed to encourage business investment. But they only benefit you if your business strategy incorporates tax planning from the beginning.

6. Green and Environmental Business Strategies

Tax incentives are increasingly tied to sustainability. Businesses investing in solar panels, wind turbines, or geothermal systems may qualify for the Investment Tax Credit (ITC) or Production Tax Credit (PTC). Companies pursuing environmental initiatives can access federal and state tax credits that meaningfully reduce operational costs.

For businesses aligned with green business strategies, tax planning is not just about minimizing liability, it can fund the environmental transformation of your operations. These incentives make sustainable business growth financially accessible in ways that many owners do not realize.

7. Exit Strategy and Business Succession

The way you exit your business is one of the most consequential tax planning decisions you will ever make. Whether you plan to sell, transfer to family, or wind down, the structure of that transaction determines how much of the value you actually keep.

In a stock sale, the seller typically pays capital gains tax on the appreciation. In an asset sale, different assets are taxed at different rates, some as ordinary income, some as capital gains. Choosing the wrong structure could cost you hundreds of thousands of dollars.

Estate planning and business succession also intersect with tax planning. Setting up the right ownership structures, gifting strategies, and trusts well in advance of a sale can significantly reduce estate and gift tax exposure.

Tax modeling, running projections across multiple exit scenarios, is essential for any business owner within five to ten years of a planned exit. The earlier you start, the more options you have.

Tax Planning Tools Every Business Should Know

Tax Deductions and Credits

Deductions reduce your taxable income. Common deductions include home office, vehicle use, business travel, meals (subject to limits), professional development, insurance premiums, and charitable contributions. Tax credits are even more valuable because they reduce your tax bill dollar-for-dollar rather than just reducing taxable income. The R&D tax credit, Work Opportunity Tax Credit (WOTC), and energy-related tax credits are among the most impactful for businesses.

Understanding which tax deductions and tax credits apply to your business requires ongoing engagement with your tax professional, not just a year-end conversation.

Tax Projections and Modeling

Tax projections involve estimating your current-year tax liability based on year-to-date financials and expected year-end results. Done quarterly, tax projections allow you to make strategic decisions before the year closes, timing purchases, deferring income, maximizing contributions.

Tax modeling takes this further, stress-testing major strategic decisions (hiring key employees, acquiring real estate, changing business structure) against different tax scenarios to identify the most financially efficient path.

Loss Harvesting

For businesses with investment portfolios or multiple entities, loss harvesting, selling underperforming investments to realize a capital loss that offsets capital gains is a tax-efficient strategy that reduces tax obligations without sacrificing long-term investment positions. Paired with thoughtful investment strategies, it is a valuable tool in any sophisticated tax plan.

Accounting Software and Automation Tools

Modern accounting software and automation tools make tax planning far more accessible. When your books are clean, accurate, and up to date, your tax professional can focus on strategy rather than cleanup. Integrated systems that track expenses by category, flag deductible items, and generate real-time financial reports give business owners the visibility they need to make tax-informed decisions year-round.

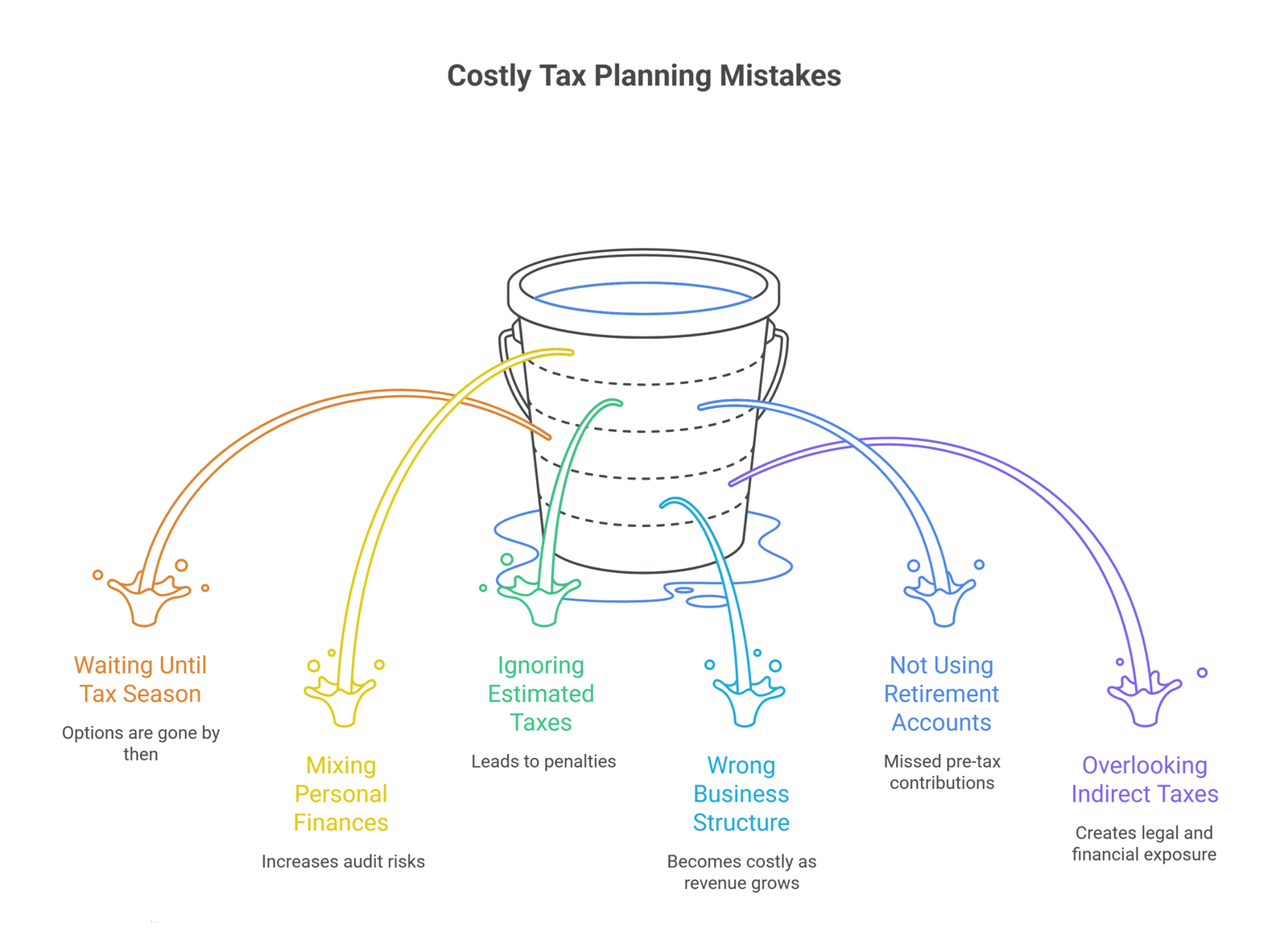

Common Tax Planning Mistakes That Cost Businesses Money

Waiting until tax season to think about taxes. By the time December 31 passes, most of your options are gone. Effective tax planning is a year-round activity.

Mixing personal and business finances. Separate financial records are essential for claiming legitimate business deductions and surviving audit risks without stress.

Ignoring estimated taxes. Missing quarterly estimated tax payments leads to penalties and cash flow disruptions. A good tax plan accounts for these obligations proactively.

Choosing the wrong business structure and never revisiting it. As revenue grows, the optimal structure may change. What worked at $200,000 in revenue may be costly at $2 million.

Not using retirement accounts. Leaving pre-tax retirement contributions on the table is one of the most common and costly small business tax planning mistakes.

Overlooking indirect taxes. Sales tax, payroll tax, and other indirect taxes can represent significant tax obligations that, when mismanaged, create legal and financial exposure. A full tax plan accounts for direct and indirect taxes alike.

The Role of a Tax Professional in Business Strategy

A qualified tax professional does more than prepare returns. The right advisor serves as a strategic partner who understands your business model, anticipates changes in tax laws, and proactively identifies opportunities to reduce your tax situation before it becomes a problem.

With ongoing tax reform, including potential changes to corporate rates, pass-through deductions, and capital gains taxes, businesses need professionals who monitor tax laws in real time and update their strategies accordingly. The tax code is not static, and neither should your business strategy be.

The best tax professionals bring together tax risk management, financial planning, and business strategy into a unified advisory relationship. They help you make investment decisions, evaluate business structure options, optimize retirement planning, and navigate tax authorities with confidence.

Industry-Specific Tax Planning Considerations

Real estate and construction: Cost segregation studies, depreciation timing, opportunity zone investments, and like-kind exchanges under Section 1031 are core tools.

Manufacturing and technology: The R&D tax credit, Section 179, and bonus depreciation are among the highest-value opportunities. Supply chain decisions can also have indirect tax implications.

Professional services: Business structure choice, retirement plan design, and the qualified business income (QBI) deduction are critical planning areas.

Healthcare: Complex tax situations involving both professional and entity income require specialized strategies for income deferral, retirement planning, and entity structuring.

Frequently Asked Questions (FAQs)

What is the difference between tax planning and tax preparation?

Tax preparation is the process of filing your return after the year ends. Tax planning is the proactive, year-round process of analyzing your financial situation and making decisions that legally minimize your tax obligations. Planning happens before the year closes; preparation happens after.

How often should a business review its tax strategy?

At minimum, quarterly. Significant business events — a major contract, an equipment purchase, a new hire, a restructuring — should trigger an immediate review. Many growing businesses benefit from monthly check-ins with their tax advisor.

What are the most valuable tax deductions for small businesses?

Retirement plan contributions, home office deductions, health insurance premiums, vehicle expenses, Section 179 expensing, and the qualified business income (QBI) deduction are consistently among the highest-value tax deductions for small businesses.

Can tax planning reduce my business’s audit risks?

Yes. A well-documented, consistent tax plan — with clean financial records, proper categorization of expenses, and reasonable positions taken on your return — significantly reduces audit risks. Working with a qualified tax professional further reduces exposure.

How does business structure affect tax planning?

Enormously. Each business structure — sole proprietorship, LLC, S-Corp, C-Corp — has different tax treatment of income, self-employment taxes, capital gains, and distributions. Choosing the right structure for your revenue level, industry, and growth plans is one of the most impactful tax planning decisions you can make.

What is income deferral and how does it help businesses?

Income deferral is the strategy of delaying the recognition of revenue into a future tax year, typically to avoid a higher tax bracket in the current year or to take advantage of anticipated lower rates. It is a legitimate and common component of cash flow management and tax planning strategy.

Conclusion

The most successful businesses do not treat tax planning as a compliance obligation. They treat it as a strategic advantage. Every dollar saved in taxes is a dollar available to reinvest, hire, expand, or distribute to owners. Over a decade, smart tax-efficient strategies can generate more value than many marketing campaigns or operational improvements.

Whether you are a small business just getting started or a mid-market company preparing for a major capital raise or exit, the time to build a proactive tax strategy is now, not at year-end, and not after a problem arises.

At Oak Business Consultant, our fractional CFO services bring strategic financial leadership to businesses that need high-level guidance without the overhead of a full-time executive. Our team helps integrate tax planning into your broader financial planning and business strategy, so that your tax situation works for you, not against you.

Ready to turn your tax strategy into a competitive advantage? Explore our Fractional CFO Services and let’s build a financial strategy that keeps more of your hard-earned revenue where it belongs, in your business.

{kind=link}