Mastering Tomorrow: A Deep Dive into Financial Risk Modeling

Mastering Financial Risk Modeling: Techniques, AI & Regulatory Compliance

Financial risk modeling is the critical engine powering modern risk management within financial institutions. It’s far more than just crunching numbers; it’s the process of using mathematical and statistical techniques to quantify and predict potential losses arising from uncertainty in financial markets. This crucial practice allows for informed Decision Making regarding capital allocation, trading strategies, and regulatory compliance. Effective financial risk modeling provides the foundation for sound Financial Risk Management and resilience in an increasingly complex and interconnected global economy.

The Pillars of Financial Risk

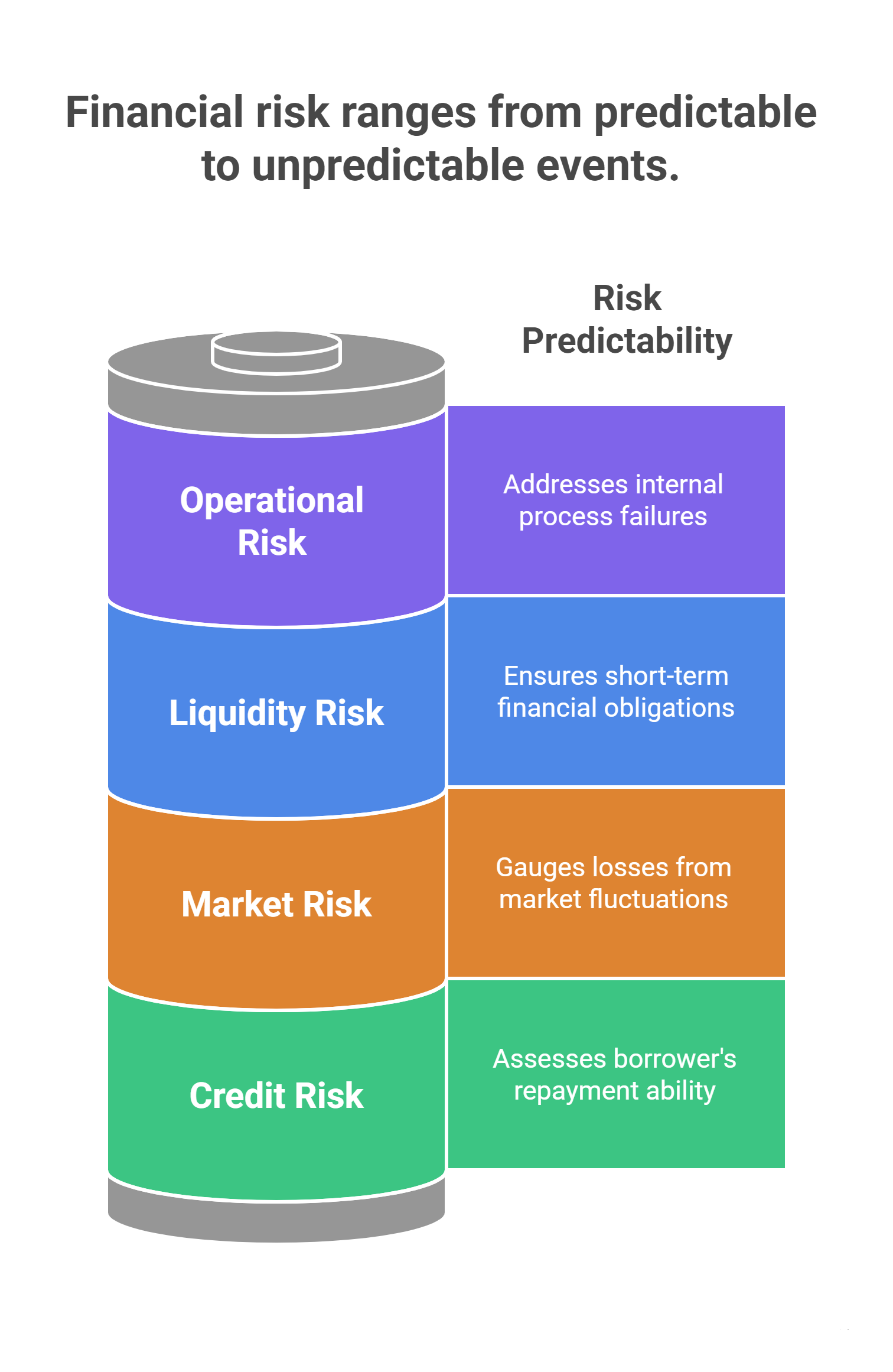

To build robust risk models, we first need to understand the main categories of Financial Risk:

- Credit Risk: This is the risk of loss due to a borrower’s failure to repay a loan or meet contractual obligations. Credit risk models use inputs like FICO scores, debt-to-income ratios, and historical default probability to estimate potential losses. The objective here is to manage the exposure to default risk.

- Market Risk: This is the risk of losses on financial assets arising from adverse movements in market trends or interest rates. Key areas include changes in asset prices, currency rates, and commodity prices. Market risk models frequently employ metrics like Value at Risk (VaR) and Expected Shortfall (ES), often relying on techniques such as historical simulation and the GARCH family of models to capture volatility clusters.

- Liquidity Risk: The risk that an institution cannot meet its short-term financial demands, or the risk that an asset cannot be sold quickly enough without suffering a significant loss.

- Operational Risk: This covers losses resulting from inadequate or failed internal processes, people, and systems, or from external events.

Techniques and Methodologies in Financial Risk Modeling

Financial risk modeling employs a diverse toolkit of methodologies, each designed to tackle different aspects of uncertainty:

- Monte Carlo Simulation: A powerful technique that uses random sampling to model the probability distribution of potential outcomes. It’s especially useful for complex problems, such as Derivatives Pricing or estimating extreme losses in a portfolio, and is a staple for stress testing.

- Stress Testing: This is a forward-looking risk management strategy that assesses the resilience of a portfolio or an entire financial institution. It evaluates performance under extreme yet plausible hypothetical scenarios, such as a severe financial crisis or extreme shifts in economic indicators.

- Extreme Value Theory (EVT): This branch of statistics is dedicated to modeling the probability of rare, severe events. It offers a strong theoretical basis for calculating metrics like Expected Shortfall that go beyond the limitations of normal distributions.

- Advanced Analytics and AI/ML: The rise of Big Data and massive computing power has revolutionized financial risk modeling. Modern risk models are increasingly leveraging machine learning and artificial intelligence. This includes deep learning and even Generative AI, which enhances predictive power. Techniques like random forest and artificial neural networks can uncover complex, non-linear patterns in data that traditional linear models might miss.

The Challenge of Model Risk Management

While sophisticated risk models are essential, they are not infallible. The reliance on models introduces model risk, which is the potential for adverse consequences from decisions based on incorrect or misused model outputs. Managing this risk is paramount, making model risk management a distinct and vital discipline.

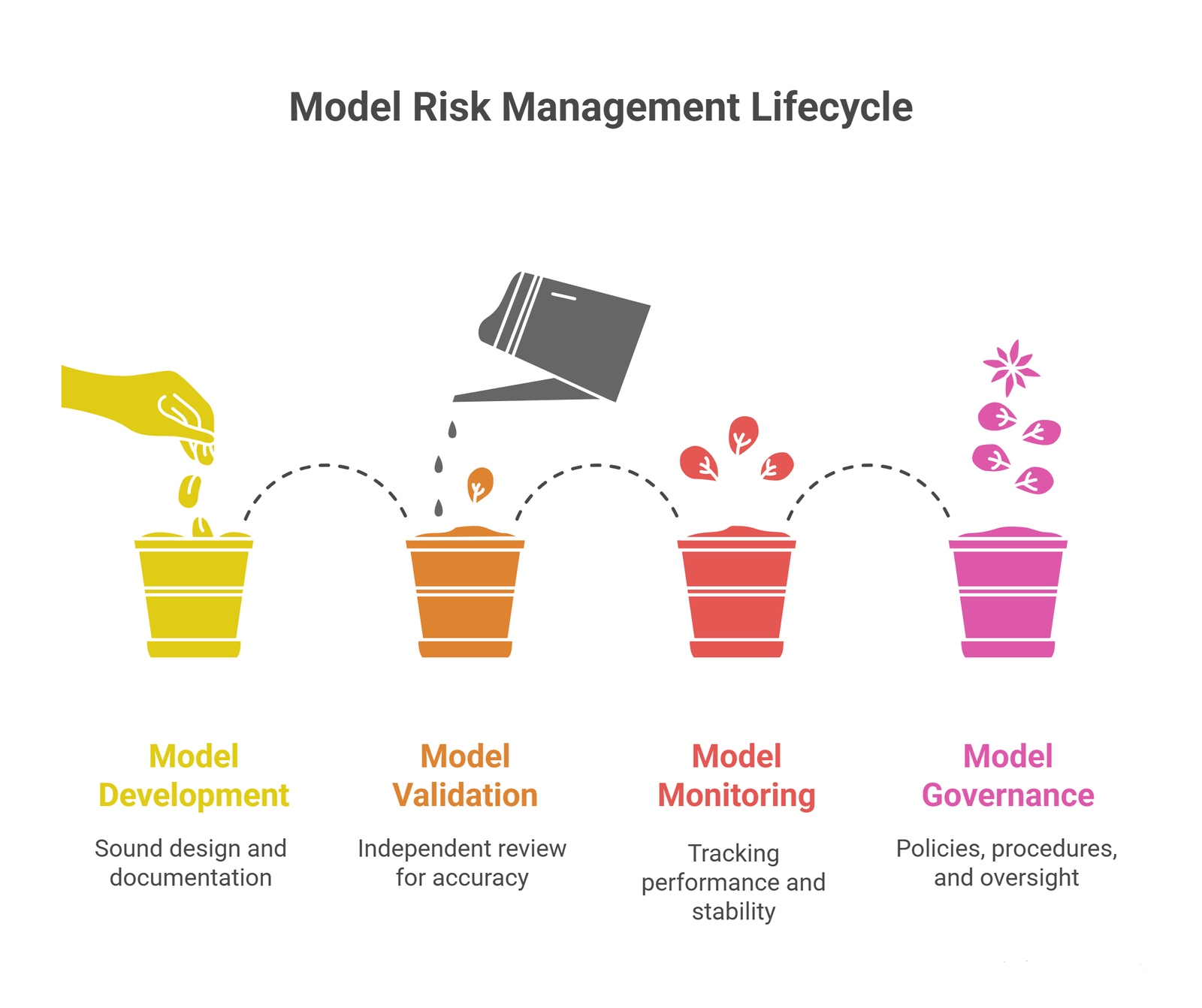

A robust model risk management framework encompasses the entire model lifecycle:

- Model Development: Ensuring sound design, methodology, and thorough documentation.

- Model Validation: An independent review process to confirm the model is functioning as intended, accurately, and without material bias. Model validation is a regulatory requirement.

- Model Monitoring: Continuously tracking the model’s performance and stability in production to detect any drift or degradation in predictive power.

- Model Governance: Establishing a formal system of policies, procedures, and oversight. This includes maintaining an up-to-date model inventory and formal model approval to ensure models are used appropriately and comply with regulatory requirements.

This strict oversight, particularly mandated by frameworks like Basel II and guidance from bodies like the Federal Reserve, is crucial. The complexity and ‘black box’ nature of some AI/ML models introduce unique regulatory challenges related to transparency and explainability. Strong data governance is also critical, as the output of any financial risk modeling is only as good as the input data.

Ultimately, successful financial risk modeling is about providing clearer insights into uncertainty. It allows institutions to take calculated risks for growth while safeguarding against existential threats. This approach helps achieve better regulatory compliance and more effective risk management strategies.

Frequently Asked Questions

What is the primary goal of financial risk modeling?

The primary goal is to provide quantitative estimates of potential future losses and exposures across various types of Financial Risk (like Credit risk, market risk, and Liquidity risk). It helps financial institutions make better-informed Decision Making around capital reserves, pricing, and strategic direction. This is part of their broader risk management efforts.

How have machine learning and artificial intelligence impacted financial risk modeling?

Machine learning and artificial intelligence have brought immense improvements in speed and predictive power to financial risk modeling. They allow for the processing of Big Data and the identification of complex, non-linear relationships that were previously too difficult to model. They are increasingly used in areas like fraud detection, default probability forecasting, and optimizing stress-testing scenarios.

What is “model risk” and why is it so important to manage?

Model risk is the potential for adverse consequences, including financial loss and reputational damage, resulting from decisions based on an incorrect or misused risk model. It’s important to manage because virtually all critical functions in a modern financial institution rely on risk models. A comprehensive model risk management program, including independent model validation, is essential for stability and meeting regulatory requirements.

Is Value at Risk (VaR) still the main metric used in financial risk modeling?

Value at Risk (VaR) is still widely used in financial risk modeling, particularly for reporting under regulatory frameworks. However, it has limitations, such as its inability to capture “tail risk” (extreme losses) and its lack of subadditivity. These limitations have led to the increasing adoption of more robust measures like Expected Shortfall (ES). ES is often considered a better metric for capturing the loss expected in worst-case scenarios.

Conclusion

Financial risk modeling is the indispensable cornerstone of modern finance. By harnessing the power of advanced techniques from Monte Carlo Simulation to sophisticated machine learning, financial institutions can accurately quantify and manage risks like Credit risk and market risk. Effective model risk management and strict regulatory compliance ensure these powerful tools are used wisely. Embracing cutting-edge financial risk modeling is not optional. It is the definitive strategy for navigating global uncertainty and securing long-term financial resilience. Ready to elevate your risk strategy? Contact us today to deploy expert-level risk models that drive superior Decision Making and growth.