Top 10 Types of Financial Models Explained

Understanding the 10 Key Types of Financial Models

Every business eventually needs a financial model, but not the same one. A startup raising its first round needs something very different from a private equity firm structuring a buyout, and a company forecasting next quarter’s budget needs something different again. Building the right model in Excel starts with knowing which of these types actually answers the question in front of you, not with picking the most impressive-looking template.

Before going through each one, it helps to sort them into two buckets. Some models are built for people inside the company: budgets, forecasts, and internal planning tools that never leave the finance team. Others are built to show outside stakeholders, investors, lenders, or acquirers, what the business is worth or whether a deal makes sense. Keeping that distinction in mind makes it easier to see why a startup’s first model looks nothing like a private equity firm’s.

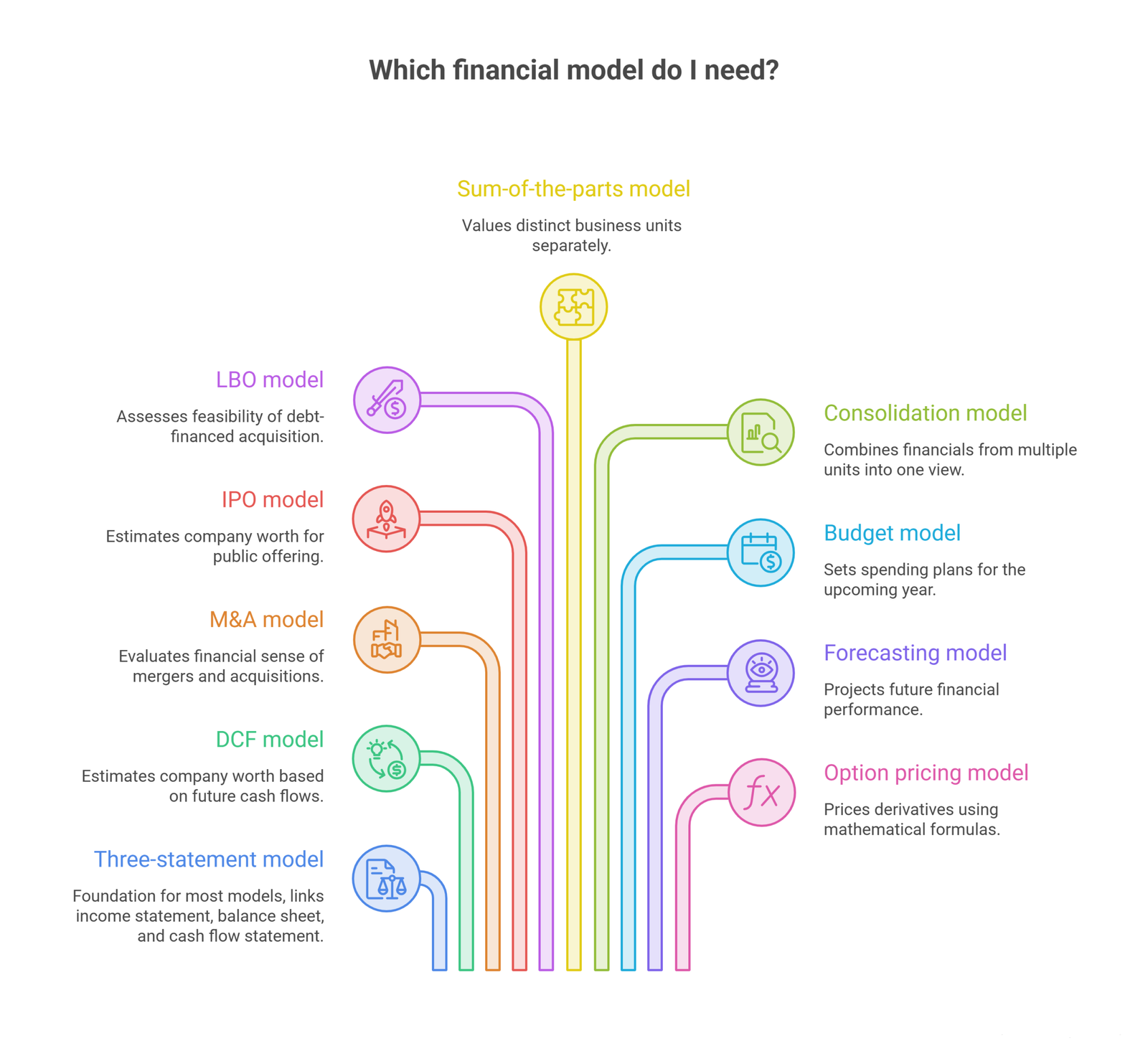

1. Three-statement model

The three-statement model is the foundation almost every other model on this list is built on. It links the income statement, balance sheet, and cash flow statement in Excel so a single change in one assumption flows through all three automatically.

The income statement shows revenue and expenses over a period, based on historical performance and current assumptions. The balance sheet shows assets, liabilities, and shareholder equity at a single point in time. The cash flow statement tracks cash inflows and outflows on top of what the income statement records on an accrual basis.

Almost every business builds some version of this model, regardless of size, and it is usually the first one a startup financial model should include before layering on anything more advanced. For a closer look at how the three statements actually connect line by line, see this walkthrough of building an integrated three-statement model.

2. DCF (discounted cash flow) model

The discounted cash flow model estimates what a company is worth today, based on the cash it is expected to generate in the future. It is one of the most widely used valuation methods in equity research and investment analysis.

It starts with the three-statement model’s output, then forecasts free cash flow using assumptions about revenue growth, margins, working capital, and capital spending. Those future cash flows get discounted back to today’s value using the weighted average cost of capital (WACC), which reflects the risk associated with the investment. Getting that discount rate right is one of the harder parts of building a credible DCF, since it drives the entire valuation. A solid financial analysis practice usually catches an unrealistic WACC before it quietly wrecks the output.

Two faster alternatives sit in the same family:

- Comparable company analysis (CCA) values a business by comparing it to similar public companies’ multiples, such as EV/EBITDA, instead of forecasting cash flows directly.

- Precedent transaction analysis (PTA) does something similar but looks at actual past acquisitions of similar companies instead of public trading multiples, which makes it useful when a real deal, not just public market pricing, is the closest comparison.

Neither accounts for the time value of money the way a DCF does, but both work well as a quick sanity check on a DCF’s output.

3. Merger and acquisition (M&A) model

When one company is acquiring or merging with another, this model evaluates whether the deal actually makes financial sense. It is complex enough that most businesses bring in a CFO or financial modeling specialist to build it properly.

The model combines both companies’ financials into a pro forma view, factors in projected synergies and deal terms, and calculates whether the transaction is accretive or dilutive to earnings per share. Financial ratios like EPS and internal rate of return (IRR) get scrutinized closely, alongside operational factors like integration costs and market conditions.

4. Initial public offering (IPO) model

An IPO model helps investment bankers and company leadership estimate what a business will be worth once it goes public. It borrows from comparable company analysis to gauge how the market is likely to price similar businesses, then applies an IPO discount to help the stock trade well once it hits the secondary market.

This model also incorporates sales growth forecasts, key financial ratios, and cash flow projections to give a fuller picture of the company’s financial health heading into the offering.

5. Leveraged buyout (LBO) model

An LBO model evaluates whether a company can be acquired mainly using debt, then still generate enough cash flow to pay that debt down over time. It is one of the most technically demanding models on this list, largely because the layered financing structures create circular references that require careful handling in Excel.

Private equity firms build LBO models to test a target’s debt capacity, structure the acquisition’s financing, and estimate the potential return once the investment is exited. The model weighs projected cash flows against the cost of debt financing and typically includes sensitivity analysis across different exit scenarios, since even small changes in exit multiple or holding period can swing the projected return significantly. Outside private equity and investment banking, this model shows up far less often, but it is essential for anyone evaluating a debt-financed acquisition. Oak’s custom financial model builds include LBO structures for exactly this reason.

6. Sum-of-the-parts model

This model fits businesses with multiple, fairly distinct divisions or subsidiaries, rather than a single unified revenue stream. Instead of valuing the company as one entity, each business unit gets valued separately, often using a DCF or comparable company approach best suited to that unit.

The individual valuations are then added together, and liabilities are subtracted, to arrive at the company’s overall net asset value. This approach gives more transparency into which segments are actually driving value and which might be dragging on it, which makes it useful for identifying where to invest further or where to consider restructuring.

7. Consolidation model

Where the sum-of-parts model values each division separately, the consolidation model brings them together into one unified financial picture. Each business unit typically gets its own tab in Excel, with a consolidation tab that totals everything up.

This is standard for any multi-divisional or multi-subsidiary company that needs a single, accurate view of overall financial performance, particularly for external reporting or when preparing for a broader corporate transaction. Firms managing several service lines or subsidiaries often lean on outside financial modeling consulting to keep the consolidation tab accurate as new units get added.

8. Budget model

The budget model is built primarily by financial planning and analysis (FP&A) professionals to set spending plans for the year ahead. Unlike models built for investors or acquirers, budget models are typically kept internal and never shared outside the company.

Most of the detail here sits in the income statement, and the model is usually organized monthly or quarterly rather than annually, which makes it easier to track actual spending against plan and adjust course during the year.

9. Forecasting model

The forecasting model works alongside the budget model, using historical financial data to project where the business is headed. Sometimes the two are combined into a single workbook, sometimes they are kept separate.

Three methods cover most forecasting work:

- Straight-line method: applies a historical growth rate forward, the simplest approach and a reasonable starting point for stable, predictable businesses.

- Moving average method: smooths out short-term noise by averaging recent periods, commonly using a three-month or five-month window, which works better for businesses with seasonal swings.

- Simple linear regression: projects a variable based on its relationship to another, such as marketing spend and revenue, and suits businesses with a clear, measurable driver behind growth.

Where a budget sets the target, a forecast tests whether the business is actually on track to hit it, and by how much the underlying assumptions might need to shift. Pairing the two gives a business an early warning system for when reality starts to diverge from the plan.

10. Option pricing model

The option pricing model prices derivatives using one of three approaches: Black-Scholes, the binomial model, or Monte Carlo simulation. This one leans more technical than the others on this list, built on defined mathematical formulas rather than the layered assumptions a DCF or LBO relies on.

Black-Scholes works well for European-style options with a single exercise date. The binomial model handles American-style options that can be exercised early by breaking the option’s life into discrete time steps. Monte Carlo simulation runs thousands of randomized price paths and suits more complex derivatives where the payoff depends on the underlying asset’s path, not just its final price.

Financial analysts use these models to determine fair value for options, which supports risk management strategies and investment decisions involving derivative instruments. Excel has built-in functions that make it possible to build the simpler versions without specialized software, though an experienced modeler should still be the one setting it up.

Internal vs. external models at a glance

| Model | Built for | Typical audience |

| Three-statement | Internal + external | Nearly everyone |

| Budget | Internal | FP&A, leadership |

| Forecasting | Internal | FP&A, leadership |

| Consolidation | Internal + external | Multi-division companies |

| DCF | External | Investors, equity research |

| CCA / PTA | External | Investors, bankers |

| M&A | External | Investment bankers, corp dev |

| IPO | External | Investment bankers |

| LBO | External | Private equity |

| Sum-of-the-parts | External | Analysts, PE firms |

| Option pricing | External | Derivatives, risk teams |

Frequently Asked Questions

How does the forecasting model work?

It uses historical financial data, typically through the straight-line, moving average, or regression method, to project future performance, helping the business plan strategically and catch developing risks before they become serious problems.

How does the leveraged buyout model work?

An LBO model tests whether a company can be acquired mainly through debt financing and still generate enough cash flow to service that debt while delivering a return once the investment is exited. It is heavily used in private equity and investment banking.

What’s the difference between a DCF model and comparable company analysis?

A DCF values a company based on its own projected future cash flows, discounted to present value. CCA instead values a company by comparing it to similar public companies’ valuation multiples. CCA is faster to build but does not account for the time value of money the way a DCF does.

What’s the difference between comparable company analysis and precedent transaction analysis?

CCA compares a company to similar public companies’ current trading multiples. PTA compares it to the actual prices paid in past acquisitions of similar companies. PTA often reflects a control premium that CCA does not, which tends to make it produce a higher valuation.

Which financial model should a startup build first?

Almost always the three-statement model. It is the foundation every other model, including a DCF for fundraising conversations or a budget model for internal planning, gets built on top of.

Do all businesses need an LBO or M&A model?

No. These are specialized models mainly relevant to private equity, investment banking, and companies actively pursuing an acquisition, merger, or debt-financed buyout. Most SMEs will never need to build one.

Conclusion

All ten of these models solve a different problem, and the skill is not in knowing every formula, it is in knowing which model actually answers the question the business is asking. A startup preparing to raise capital and a private equity firm structuring a buyout need entirely different tools, even though both are technically “financial models.”

Building any of these correctly takes a solid grasp of accounting, corporate finance, and Excel, which is exactly where a second set of expert eyes pays for itself. Oak Business Consultant’s financial modeling services build custom models tailored to your specific business decision, whether that is a valuation ahead of fundraising, an acquisition model, or ongoing budgeting and forecasting support. Contact us to get started.

{kind=link}

{kind=link}