Cash Flow Issues for Small Businesses & How to Fix Them

Managing Cash Flow Issues in Small Businesses: Causes and Remedies

Running a small business is hard enough. But when money stops moving the way it should, everything else starts to break down too. Cash flow issues for small businesses are not just a financial inconvenience. They are one of the leading reasons businesses close their doors for good.

According to research by U.S. Bank, 82% of small businesses that fail do so because of poor cash flow management. Not bad products. Not weak marketing. Cash. This one fact alone tells you how critical this topic is for every small business owner, whether you are just starting out or have been operating for years.

This guide breaks down what causes cash flow issues for small businesses, how to spot the warning signs early, and what practical steps you can take to stabilize your finances and grow with confidence.

What Is Cash Flow and Why Does It Matter So Much

Cash flow is the movement of money in and out of your business. Money coming in includes payments from customers, loans, and other income. Money going out includes payroll, rent, supplier payments, taxes, and everyday operating expenses.

Positive cash flow means more money is coming in than going out. Negative cash flow means the opposite. And here is the uncomfortable truth: a business can be profitable on paper and still run out of cash. That gap between what you are owed and what you actually have in the bank is where most small businesses get into trouble.

Cash flow issues for small businesses are especially painful because small companies rarely have large reserves to fall back on. A survey by Relay found that 70% of small businesses hold less than four months of cash reserves. That leaves almost no room for error when a payment is late or an unexpected expense arrives.

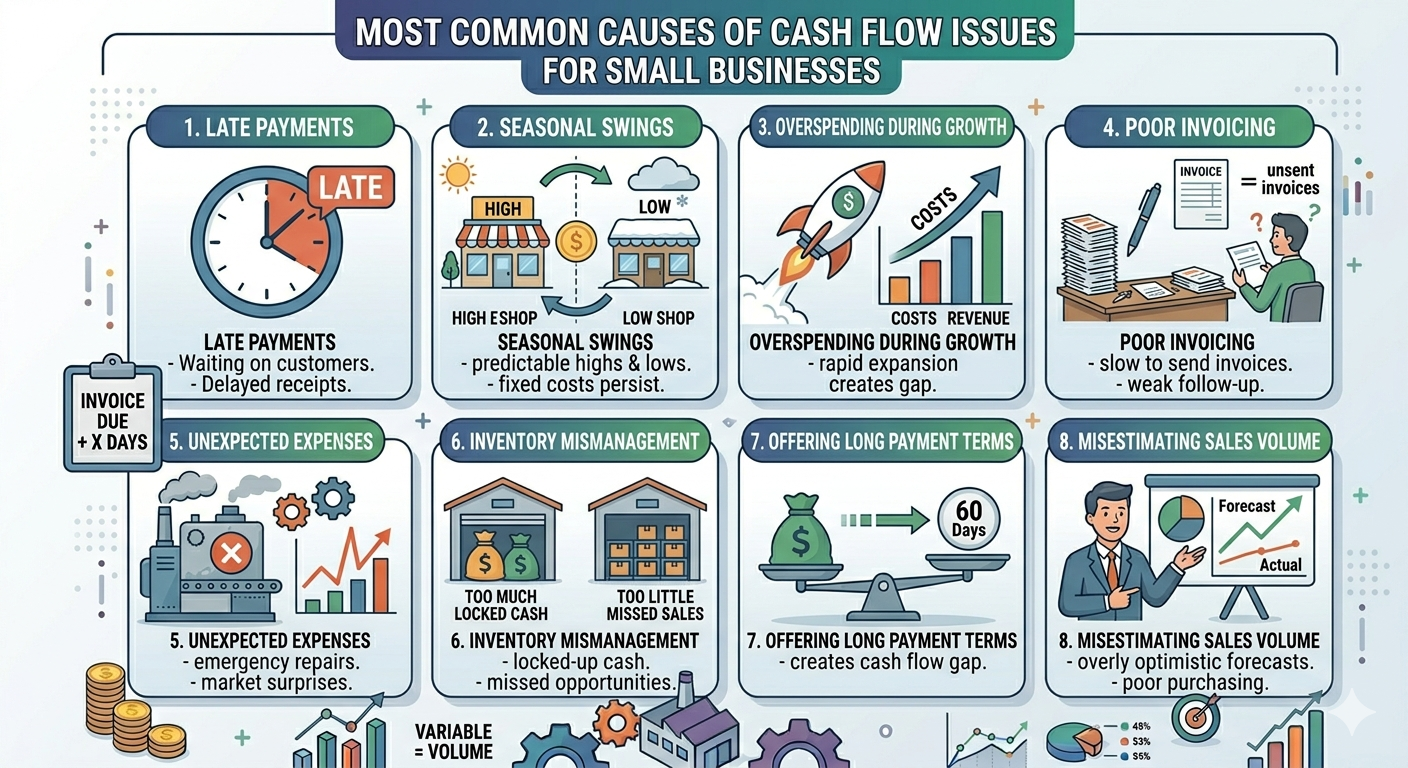

The Most Common Causes of Cash Flow Issues for Small Businesses

Understanding where cash flow problems come from is the first step toward fixing them. Most issues trace back to a handful of recurring patterns.

Late Payments from Customers

This is the single biggest driver of cash flow stress for small businesses. You have delivered the work or the product. You sent the invoice. And now you wait. Small businesses are now waiting an average of 29 days to get paid, according to data from accounting software provider Xero. Nearly half of outstanding invoices are more than 30 days overdue.

When you are waiting on money that should already be in your account, you still have to pay your own bills. That timing mismatch creates real pressure fast.

Seasonal Revenue Swings

Many small businesses experience predictable ups and downs throughout the year. A retail shop may earn 60% of its revenue in the final quarter. A landscaping company may go quiet in winter. The problem is that expenses do not pause during slow seasons. Rent, insurance, utilities, and payroll continue regardless of whether customers are buying.

Without a cash buffer or a plan for the slow months, seasonal businesses are especially vulnerable to cash flow issues for small businesses at predictable times of year.

Overspending During Growth

Growth feels exciting. New equipment, extra staff, a bigger office. But rapid expansion without careful financial planning is one of the fastest ways to drain cash. When businesses take on new costs before the revenue to support those costs actually arrives, they create a gap that can be difficult to close.

Poor Invoicing and Billing Practices

If you are slow to send invoices, offer overly generous payment terms, or do not follow up on unpaid bills, you are essentially lending money to your customers interest-free. Businesses that offer 90-day payment terms experience cash flow disruptions at twice the rate of businesses that require payment on receipt.

Simple changes to how and when you invoice can have a significant impact on your cash position.

Unexpected Expenses

Equipment breaks. A supplier increases prices. A key employee leaves and you need to replace them quickly. These surprises happen in every business. The difference between businesses that handle them well and those that do not usually comes down to how much of a cash cushion they have and how closely they monitor their finances.

Inventory Mismanagement

For businesses that carry physical products, inventory can tie up significant amounts of cash. Ordering too much stock locks money in a warehouse instead of your bank account. Ordering too little means missed sales and rushed reorders at higher cost. Either way, poor inventory management is a slow drain on cash that many business owners do not notice until things get serious.

Warning Signs You Are Heading Toward a Cash Flow Crisis

Cash flow issues for small businesses rarely appear without warning. They tend to build slowly. Knowing what to watch for gives you time to act before a problem becomes a crisis.

You may be heading toward trouble if you notice any of the following patterns. Paying suppliers later than usual, or asking for extensions more often. Relying on a line of credit to cover routine operating expenses. Struggling to make payroll on time. Avoiding opening your bank statements or financial reports. Turning down new business because you cannot afford to fulfill the orders. Feeling constant anxiety about whether there is enough money to get through the week.

These are not signs of a failing business necessarily. They are signs that your cash flow needs attention right now.

How Cash Flow Issues for Small Businesses Affect More Than Just Finances

The effects of cash flow problems go well beyond the balance sheet. A 2024 survey by Relay found that more than 71% of small business owners say cash flow issues have had a negative personal impact on them. This includes stress, anxiety, burnout, and disrupted sleep.

When you are preoccupied with survival, it is almost impossible to focus on growth, team culture, customer relationships, or strategic planning. Cash flow issues for small businesses have a way of consuming all your attention and energy, leaving little room for anything else.

Beyond the personal toll, financial strain can damage supplier relationships, reduce your ability to negotiate good terms, and make lenders less willing to work with you. The longer cash flow problems persist, the harder they become to fix on your own.

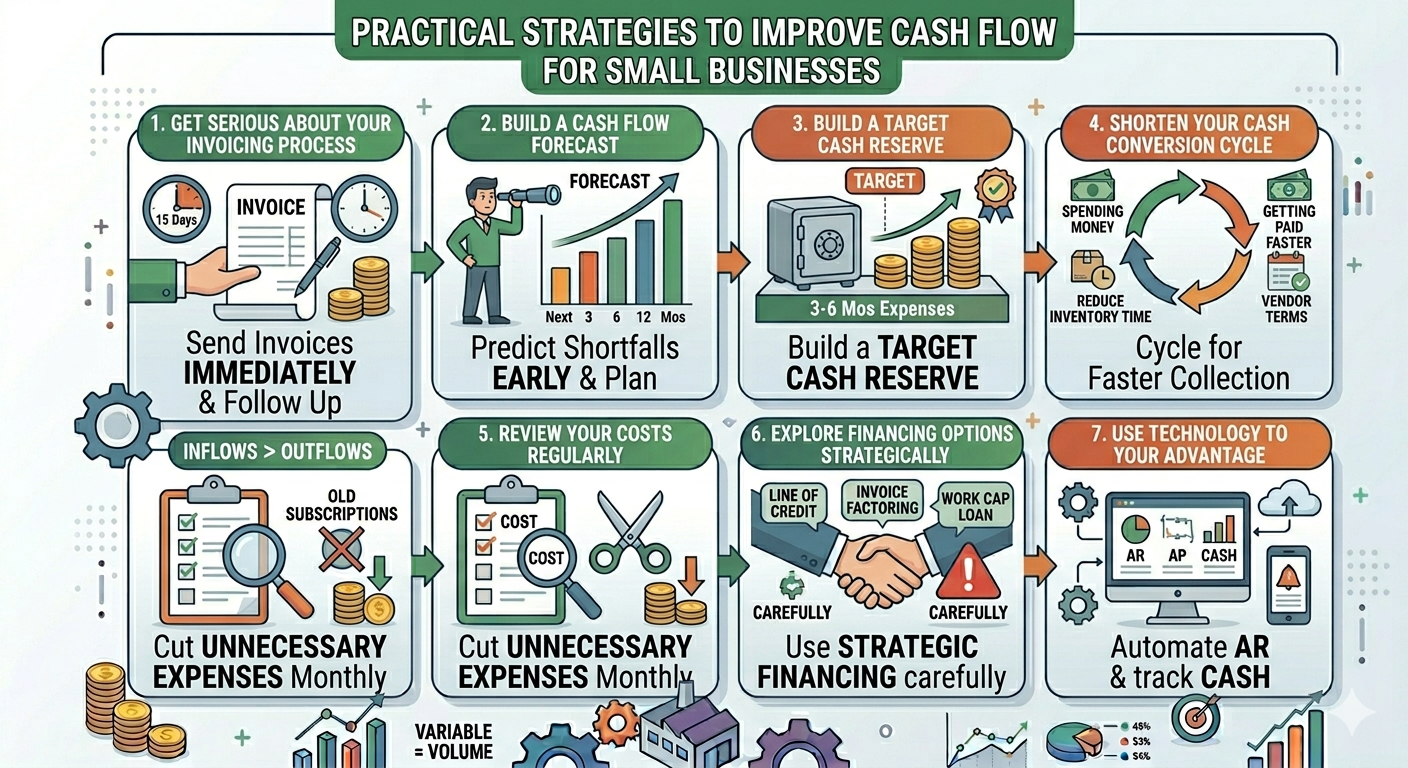

Practical Strategies to Improve Cash Flow

The good news is that most cash flow issues for small businesses are solvable. You do not always need more revenue. Sometimes you just need better systems and a clearer view of what is happening financially.

Get Serious About Your Invoicing Process

Send invoices immediately when work is complete. Set clear payment terms, ideally 15 to 30 days rather than 60 or 90. Follow up on overdue invoices promptly and consistently. Consider offering a small early-payment discount to encourage faster payment. The faster your customers pay, the healthier your cash position.

Build a Cash Flow Forecast

A cash flow forecast is simply a projection of money coming in and going out over the next 3, 6, or 12 months. It helps you see potential shortfalls before they happen so you can plan around them rather than react in panic. This does not need to be complicated. Even a basic monthly forecast built in a spreadsheet is far better than no forecast at all.

Create a Cash Reserve

Set a target of keeping 3 to 6 months of operating expenses in reserve. This is not easy to achieve quickly, but even a small buffer makes a big difference. Treat building this reserve as a fixed business priority, the same way you would treat paying rent or making payroll.

Shorten Your Cash Conversion Cycle

This is the time it takes from spending money to getting money back. You shorten it by getting paid faster, by reducing the time inventory sits unsold, and by negotiating longer payment terms with your own suppliers. Even small improvements here free up meaningful amounts of cash.

Review Your Costs Regularly

Many businesses are paying for services, subscriptions, or overhead they no longer need. A regular review of your expenses, even quarterly, often reveals opportunities to cut costs without affecting operations. The money you save goes directly to improving your cash position.

Explore Financing Options Strategically

A business line of credit, invoice factoring, or short-term working capital loan can bridge temporary cash gaps when used carefully. The key word is carefully. Borrowing to cover a short-term mismatch between revenue and expenses can make sense. Borrowing to cover structural losses or ongoing operational deficits rarely solves anything and often makes things worse.

Use Technology to Your Advantage

Digital invoicing tools, automated reminders, and accounting software give you real-time visibility into your cash position. Businesses that use automated accounts receivable processes report significantly better cash flow outcomes than those still relying on manual processes. The investment in a good accounting or finance platform usually pays for itself quickly.

The Role of Financial Expertise in Solving Cash Flow Problems

Many small business owners are experts in their product or service. They are not necessarily trained financial managers. And that is completely normal. The challenge is that cash flow issues for small businesses often require financial expertise to diagnose properly and fix sustainably.

This is where having access to experienced financial guidance makes a real difference. A skilled CFO, whether in-house or on a fractional basis, can build the forecasting systems, identify the root causes, and put the structures in place that prevent cash flow problems from recurring.

The difference between a business that struggles with cash flow year after year and one that manages it well usually comes down to having the right financial strategy and the right people helping to execute it.

Industry-Specific Considerations

Cash flow issues for small businesses look different depending on your industry.

In construction and contracting, long project timelines and milestone-based billing mean cash can be tied up for months. Managing draws, subcontractor payments, and material costs requires precise timing.

In retail, inventory planning and seasonal demand make cash flow forecasting especially important. Buying too much at the wrong time can leave you cash-poor heading into a slow period.

In professional services, the main issue is usually the gap between delivering work and getting paid. Retainer arrangements and deposit requirements can help close this gap.

In hospitality and food service, thin margins and high labor costs mean there is very little room for error. Even a week of slow business can create serious pressure.

Understanding the cash flow patterns that are specific to your industry helps you plan more accurately and avoid problems that catch others off guard.

What a Proactive Cash Flow Strategy Looks Like

Businesses that manage cash flow well do not just react to problems. They build systems that give them advance warning and clear options when challenges arise.

A proactive approach includes reviewing cash flow reports at least weekly. It includes a rolling 90-day cash forecast that is updated regularly. It includes clear payment policies for customers and a process for following up on overdue accounts. It includes a credit facility in place before it is needed, not after. And it includes a financial advisor or CFO who is actively engaged in the business, not just available when something goes wrong.

This kind of proactive financial management is what separates businesses that grow steadily from those that are constantly fighting fires.

Frequently Asked Questions

What are the most common cash flow issues for small businesses?

The most common causes are late payments from customers, poor invoicing practices, seasonal revenue fluctuations, unexpected expenses, rapid growth without adequate capital, and weak financial forecasting. Most cash flow problems can be traced back to one or more of these root causes.

How much cash reserve should a small business keep?

Most financial advisors recommend maintaining at least 3 to 6 months of operating expenses in reserve. This gives you a buffer to handle slow periods, unexpected costs, or delayed customer payments without disrupting operations.

Can a profitable business still have cash flow problems?

Yes, absolutely. A business can be profitable on paper and still run out of cash. This happens when revenue is tied up in unpaid invoices, excess inventory, or when money is going out faster than it is coming in. Profitability and positive cash flow are not the same thing.

How do I fix cash flow problems quickly?

Quick wins include sending invoices immediately, following up on overdue payments, delaying non-essential purchases, and reviewing expenses for immediate cuts. For more lasting improvement, you need better forecasting, tighter payment terms, and ideally, financial expertise to help you build the right systems.

When should a small business hire a CFO?

If cash flow issues are recurring, if you are making major financial decisions without a clear picture of your finances, or if you are growing faster than your current financial systems can handle, it is time to bring in CFO-level expertise. Fractional CFO services offer access to that level of guidance without the cost of a full-time hire.

Conclusion

Cash flow issues for small businesses are common. But they do not have to be permanent. With the right strategy, the right tools, and the right financial expertise, you can move from constant financial stress to a position of clarity and control.

If you are ready to stop reacting and start planning, Oak Business Consultant offers expert CFO services designed specifically for small and growing businesses. From cash flow forecasting and financial modeling to full fractional CFO support, the team at Oak helps business owners build the financial foundation they need to grow with confidence.

Reach out today to learn how their CFO services can help you take control of your cash flow for good.

{kind=link}