Some Practical Budget Examples to Help You with Financial Budgeting

Practical Budget Examples to Help with Budgeting

A financial budget is only useful if you can see it applied to real numbers. Definitions of “operating budget” or “cash budget” are easy to find; what’s harder to find is a worked example that shows how those numbers actually move through a real budgeting cycle. This guide covers the core types of business budgets, walks through a full numeric example for a small business, and shows how the pieces connect into a master budget.

What a financial budget is

A financial budget is a projection of a business’s income, expenses, and capital needs over a defined period, usually a quarter or a year. It’s built after the operating budget, since a financial budget depends on figures the operating budget produces first, like expected sales and production costs. A financial budget centers on two components: a capital expenditure budget and a cash budget, which together feed into a budgeted balance sheet showing where the business expects to stand financially at the end of the period.

The main types of business budgets

Most businesses work with some combination of the following. None of these exist in isolation; together they roll up into what’s called a master budget.

| Budget type | What it covers | Typical owner |

| Operating budget | Day-to-day revenue, cost of goods sold, and operating expenses | Finance / department heads |

| Sales budget | Projected sales volume and revenue by product or period | Sales leadership |

| Production budget | Units to produce based on sales forecasts and inventory targets | Operations |

| Labor budget | Staffing costs, including wages, benefits, and overtime | HR / department heads |

| Cash budget | Cash inflows and outflows over the period, used to catch liquidity gaps | Finance |

| Capital expenditure (CapEx) budget | Planned spending on long-term assets like equipment or property | Finance / leadership |

| Static budget | Fixed regardless of sales volume or activity changes | Finance |

| Flexible budget | Adjusts line items (like commissions) based on actual sales volume | Finance |

| Master budget | Consolidates every individual budget into one overall financial plan | Finance / CFO |

Static vs. flexible, in practice: if sales fall short of target, a static budget leaves every line item unchanged, which works fine for costs like rent that don’t move with sales. A flexible budget instead adjusts variable items proportionally. If a sales team’s commission budget assumes $200,000 in revenue at a 5% commission rate ($10,000), and revenue instead comes in at $150,000, a flexible budget adjusts the commission line down to $7,500 rather than leaving a stale $10,000 figure on the books.

Three more budget types worth knowing

Beyond the core set above, three additional approaches show up often enough to be worth naming directly:

- Zero-based budget. Instead of adjusting last year’s numbers up or down, every expense is built from zero and has to be justified fresh each period. It takes more effort to build than a standard incremental budget, but it catches costs that have quietly become “just how we’ve always spent” rather than something anyone actively decided on.

- Overhead budget. A dedicated line for fixed and variable overhead costs (utilities, admin support, facilities) that don’t tie directly to a specific product or project. Useful for businesses where overhead is a large enough share of spending to warrant its own visibility rather than being buried inside the operating budget.

- Project budget. A standalone budget scoped to a single initiative, like a product launch or a systems implementation, combining labor, materials, and overhead specific to that project so it can be tracked separately from ongoing operations.

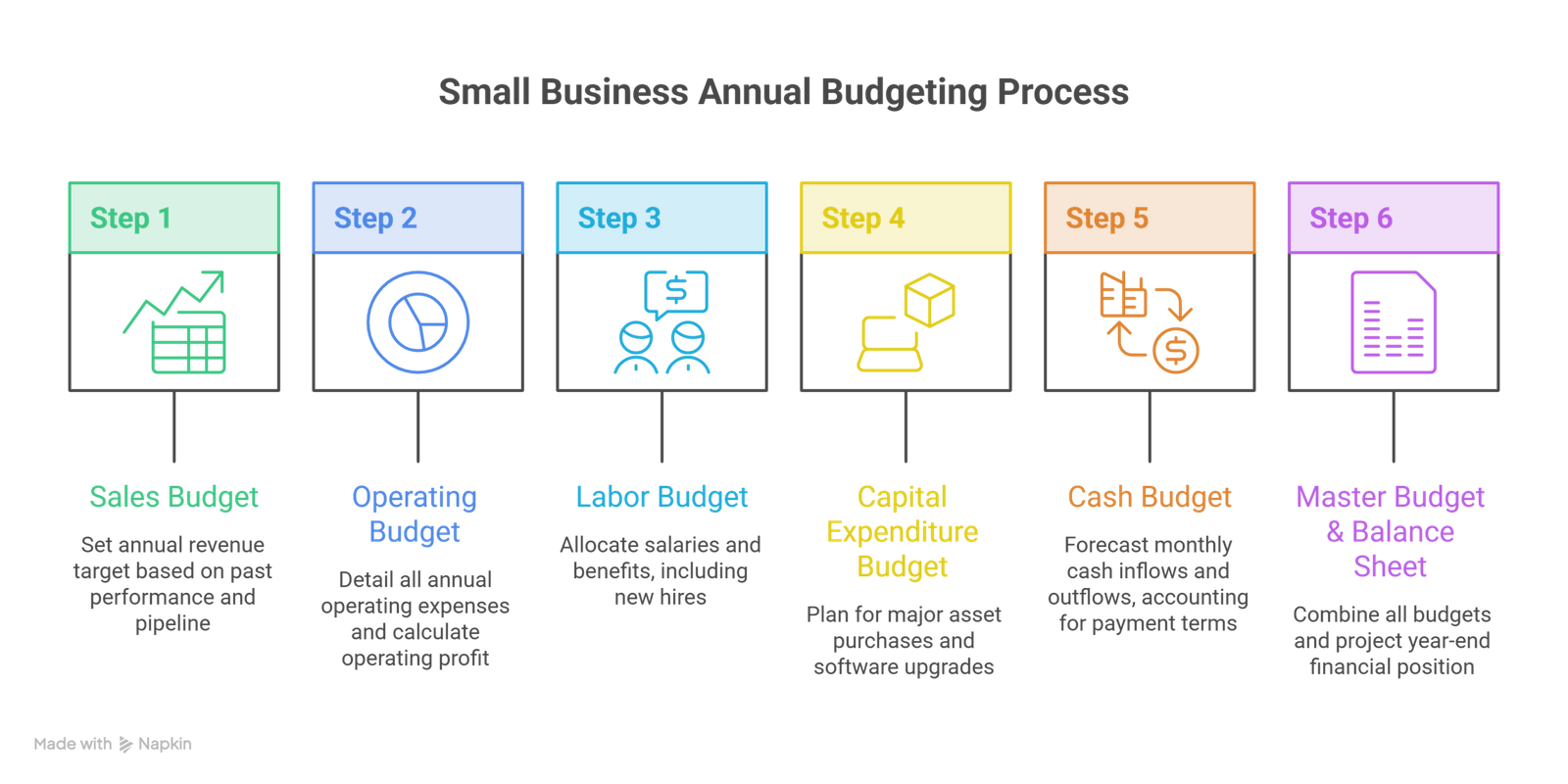

A full worked example: small business annual budget

Here’s how these pieces come together for a hypothetical small business, a 12-person marketing agency planning its budget for the year ahead.

Step 1: Build the sales budget.

Based on last year’s revenue of $850,000 and a signed pipeline suggesting 12% growth, the agency sets a sales budget target of $952,000 for the year.

Step 2: Build the operating budget.

| Line item | Annual amount |

| Revenue | $952,000 |

| Salaries and benefits | $480,000 |

| Rent and utilities | $84,000 |

| Software and tools | $36,000 |

| Marketing and business development | $45,000 |

| Insurance and professional fees | $28,000 |

| Miscellaneous operating expenses | $22,000 |

| Total operating expenses | $695,000 |

| Operating profit | $257,000 |

Step 3: Build the labor budget.

Of the $480,000 salary line, the agency budgets for one new hire mid-year, adding roughly $35,000 in incremental cost for the back half of the year, already reflected in the total above.

Step 4: Build the capital expenditure budget.

The agency plans to replace aging laptops and upgrade its project management software licensing, budgeting $18,000 for the year in capital spending.

Step 5: Build the cash budget.

This is where profit on paper and actual cash available can diverge. Even with $257,000 in operating profit, the agency’s clients pay on 45-day terms, so the cash budget needs to account for that lag. Assuming a starting cash balance of $50,000:

| Month | Cash in | Cash out | Net cash flow | Ending cash balance |

| January | $70,000 | $58,000 | $12,000 | $62,000 |

| February | $65,000 | $60,000 | $5,000 | $67,000 |

| March | $90,000 | $58,000 | $32,000 | $99,000 |

| April | $78,000 | $60,000 | $18,000 | $117,000 |

| May | $82,000 | $60,000 | $22,000 | $139,000 |

| June | $74,000 | $76,000 | -$2,000 | $137,000 |

| July | $88,000 | $61,000 | $27,000 | $164,000 |

| August | $92,000 | $62,000 | $30,000 | $194,000 |

| September | $80,000 | $62,000 | $18,000 | $212,000 |

| October | $95,000 | $63,000 | $32,000 | $244,000 |

| November | $86,000 | $63,000 | $23,000 | $267,000 |

| December | $72,000 | $78,000 | -$6,000 | $261,000 |

June’s dip lines up with the mid-year hire adding roughly $35,000 in incremental annual cost, and December reflects year-end bonus payouts, both cash-out items layered on top of the regular operating spend shown in the table above. Catching a pattern like that in the cash budget, ahead of time, is the difference between a planned dip and a scramble. Note that the cash-out totals here run somewhat above the $695,000 operating expense figure, since the cash budget also captures the timing of the $18,000 CapEx spend and payroll tax deposits that aren’t broken out as separate lines in the operating budget.

Step 6: Roll it into the master budget and budgeted balance sheet.

The master budget combines the operating budget, labor budget, CapEx budget, and cash budget into one document, and the budgeted balance sheet shows projected assets, liabilities, and equity at year-end based on all of the above.

Common mistakes when building these budgets

- Skipping the sales budget as the starting point. Every other budget depends on a realistic sales forecast; build one on hope instead of pipeline data and everything downstream is wrong too.

- Treating a static budget as the only option. For cost lines that genuinely move with revenue (commissions, materials, shipping), a static budget hides the real story until the year is already over.

- Ignoring payment timing in the cash budget. Revenue and expenses recognized this month aren’t the same as cash landing this month. This gap is exactly what a cash budget exists to catch, and it’s also why a cash budget shouldn’t be skipped even when the operating budget looks healthy.

- No CapEx line for known replacement costs. Equipment, software licenses, and office assets need replacing on a predictable cycle. Leaving that out of the budget means it hits as a surprise expense instead of a planned one.

- Not updating the budget against actuals. A budget built once in January and never revisited loses its usefulness by mid-year. Comparing actuals against budget monthly or quarterly is what makes it a management tool rather than a one-time exercise.

Frequently Asked Questions

What’s the difference between an operating budget and a financial budget?

An operating budget covers day-to-day revenue and expenses. A financial budget is built afterward and focuses on capital expenditures and cash flow, using figures the operating budget produces.

Do small businesses need all of these budget types?

Not necessarily all at once. A small business with minimal capital spending and steady, quick-paying clients might not need a detailed CapEx budget or an aggressive cash budget. As a business scales or takes on clients with longer payment terms, cash and capital budgeting typically become more important.

How often should a business budget be updated?

Most businesses set the budget annually and review it monthly or quarterly against actuals, adjusting the flexible components (like commissions or variable costs) as real numbers come in.

What’s the starting point for building a master budget?

The sales budget comes first, since production, labor, and cash forecasts all depend on an accurate revenue projection.

Can a small business build these budgets without dedicated finance staff?

Yes, with a solid template and a clear understanding of the sequence (sales, operating, labor, capital, cash, then master budget). Where businesses most often get stuck is the cash budget, since it requires realistic assumptions about payment timing rather than just revenue and expense totals. This is a common point where businesses bring in outside financial support to get the model built correctly from the start.

Conclusion

The real value in these budget types isn’t in memorizing definitions, it’s in seeing how they connect: a sales forecast drives the operating budget, the operating budget informs labor and capital planning, and the cash budget translates all of it into a week-by-week or month-by-month view of what’s actually available in the bank. For a deeper look at the two core components of a financial budget, capital expenditures and cash flow, see our guide on what a financial budget actually includes. If your business is weighing a major purchase against its budget, our guide to capital budgeting and the distinction between operating and capital budgets covers that decision in more depth. We also have a breakdown of financial budget templates if you’re looking to build one of these out yourself.

If building and maintaining a full budgeting and forecasting process isn’t realistic in-house right now, that’s exactly the kind of work a fractional CFO is built to take on, from setting up the initial model through the ongoing discipline of tracking actuals against it.