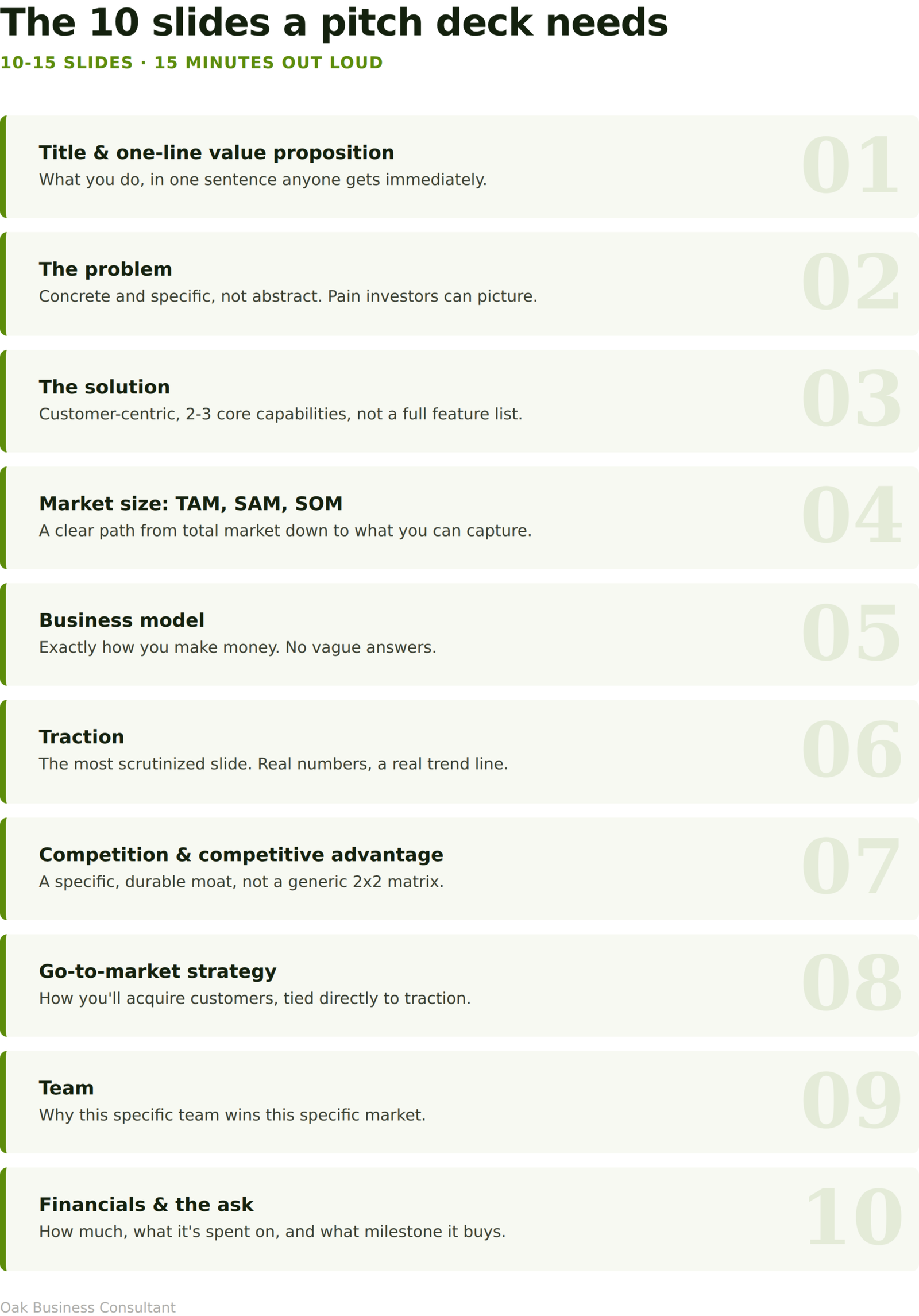

Pitch Deck Slides that every VC looks for

Important Components of Pitch Deck

Investors spend roughly three minutes and forty-four seconds reading the average pitch deck before deciding whether a founder gets a meeting. That’s not a typo. Three minutes and forty-four seconds to judge a business you’ve spent years building.

That number changes how you should think about a pitch deck. It’s not a place to explain everything about your company. It’s a filter that needs to pass a very fast first read, then hold up under questions in the room. This guide walks through the slides that consistently show up in decks that raised real money, why each one earns its place, and the mistakes that get decks closed before slide five.

What a pitch deck actually needs to do

A pitch deck is not your business plan condensed into slides. It’s closer to a movie trailer. The job is to generate enough interest that the investor wants the full story, not to tell them everything up front.

Most VCs and accelerators land in the same range: somewhere between 10 and 15 core slides, deliverable out loud in 15 minutes or less, with a 5-minute version ready if someone cuts you off. Y Combinator and Guy Kawasaki both push toward the lower end of that range. If you’re routinely needing more than 20 slides to explain your business, the problem usually isn’t the deck, it’s that the story underneath it isn’t clear yet.

The slides that earn their place

1. Title and one-line value proposition

Open with what your company does in one sentence, simple enough that someone unfamiliar with your industry gets it immediately. A common shortcut is positioning by comparison to something familiar, “the McKinsey of X” or “Airbnb for Y.” Use this technique carefully. It works when the comparison is genuinely accurate and falls flat fast when it’s a stretch.

2. The problem

State the problem you’re solving in concrete, specific terms, not abstract ones. “Small businesses waste 40 hours a month on manual invoice reconciliation” lands harder than “financial processes are inefficient.” If you can tell a short, real story that illustrates the problem, that’s stronger than a bullet list. Investors fund pain they can picture, not pain they have to take your word for.

3. The solution

This is where you show how your product actually addresses the problem you just laid out. Keep this customer-centric rather than feature-centric. A common mistake here is listing every capability the product has instead of focusing on the two or three that solve the core problem. If a screenshot or short demo clip can replace a paragraph of text, use it.

4. Market size: TAM, SAM, SOM

Investors need to see that a real, sizeable market exists, not just that your problem is real for a handful of customers. Break this into three layers: Total Addressable Market (the full revenue opportunity if you captured the whole market), Serviceable Addressable Market (the portion you could realistically serve given your business model), and Serviceable Obtainable Market (what you can realistically capture in the near term given your resources and competition).

A common red flag for VCs is a TAM number with no clear path from SAM down to SOM, which signals the founder pulled a big number from a market research report without thinking through how their specific business actually captures it.

5. Business model

How does the company make money, specifically? Subscription, transaction fees, licensing, advertising, something else? This needs to be unambiguous. Vague answers here are one of the fastest ways to lose investor confidence, since unclear revenue logic usually means the founder hasn’t fully thought through unit economics yet. If your numbers support it, this is a good place to reference your financial modeling work, since a credible model behind your revenue assumptions carries more weight than a slide of round numbers.

6. Traction

For most VCs, this is the single most scrutinized slide in the deck, arguably more important than the idea itself. Traction is concrete evidence that the business already works at some scale, not just that it could work in theory. Depending on your stage, this might be revenue growth, user growth, retention numbers, signed pilots, letters of intent, or waitlist size. Whatever you show, make sure the numbers are real and the trend line, not just a single snapshot, is visible. A flat or declining trend dressed up with a single good month rarely survives a follow-up question.

7. Competition and competitive advantage

Show where you sit relative to alternatives, and be specific about what makes you defensible, not just different. Investors are wary of generic 2×2 competitive matrices where the pitching company conveniently lands in the upper right corner. Every competitor’s deck claims the same spot. What actually matters here is naming the real, durable advantage: proprietary data, network effects, regulatory position, a technical moat, or a team with domain expertise others can’t easily replicate.

8. Go-to-market and marketing strategy

How will you actually acquire customers, and what does that cost? This slide should connect directly to your traction slide rather than existing as a separate, abstract plan. If you’ve already proven a channel works at small scale, say so and show the numbers. If you haven’t, be honest about which channels you intend to test and why you believe they’ll work for this specific customer.

9. Team

Investors back people as much as ideas, especially at early stages where the product will inevitably pivot but the team won’t. Highlight relevant experience, prior exits, domain expertise, or anything that signals this specific group is positioned to execute on this specific problem. Skip generic LinkedIn-style bios. Focus on what’s directly relevant to why this team can win in this market.

10. Financials and the ask

Close with a clear, specific funding ask: how much you’re raising, what you’ll spend it on, and what milestones that money gets you to before the next round. Vague asks (“we’re raising to fuel growth”) read as a founder who hasn’t done the underlying math. A financial model that ties the ask to a believable runway and a believable next milestone makes this slide far more credible than a number pulled out of thin air.

Mistakes that get decks closed early

A few patterns show up again and again in decks that don’t get a second meeting.

Overloading slides with text is the most common one. If a VC has to read a paragraph to understand a slide, the slide has already failed, since most investors skim rather than read in that first pass. Aim for one core idea per slide, with the title alone carrying most of the meaning. A useful test: if someone read only the titles of every slide in your deck, in order, would that read like a coherent executive summary of your pitch? If not, your slide order or framing needs work.

Inflated or unsupported market numbers are another fast way to lose credibility. A massive TAM with no believable path to capturing any meaningful slice of it tells an investor you haven’t done the work, even if the idea itself is good.

Skipping or burying the ask is a surprisingly frequent mistake. Founders get so focused on building the case for their business that they forget to clearly state how much they want and why. Don’t make an investor dig for this.

An out-of-date deck is its own problem. Fundraising takes time, sometimes dozens of investor meetings before a close, and presenting stale numbers or an outdated roadmap mid-process signals disorganization more than anything else.

How long should a pitch deck actually be

There’s no single magic number, but the range that keeps showing up across VC commentary and successful raises is 10 to 15 core slides, deliverable verbally in 15 minutes, with appendix slides held in reserve for detail an investor might ask about afterward. Put financial detail, technical architecture, and case studies in an appendix rather than the core deck. That keeps the main narrative tight while still giving you backup material if someone wants to dig deeper.

Frequently Asked Questions

What’s the single most important slide in a pitch deck?

Traction tends to carry the most weight for most investors, since it’s tangible proof the business already works at some level rather than a promise that it might. Early pre-revenue startups without much traction yet should lean harder on team strength and market size to compensate.

Should I include financial projections in the main deck or an appendix?

Keep a simplified, high-level financial summary in the main deck, tied directly to your funding ask, and move the detailed monthly or annual breakdown into an appendix. Investors who want the granular numbers will ask, and having a solid model ready to share signals preparedness.

How do I figure out my TAM, SAM, and SOM if I don’t have market research data?

Start with publicly available industry reports for your broad TAM, then narrow based on your actual business model and geography for SAM, and finally apply a realistic capture rate based on your sales capacity and competitive position for SOM. If the numbers feel uncertain, a business valuation or market analysis exercise can sanity-check your assumptions before they go in front of investors.

Do I need a different pitch deck for each investor?

Not a different deck for each one, but you should tailor emphasis based on what you know about that investor’s thesis and stage focus. The core slides and numbers should stay consistent. What changes is which parts you spend more time on in the room.

Final thoughts

A pitch deck that works isn’t the one with the most polished design or the longest list of features. It’s the one that tells a clear, evidence-backed story in the time an investor is actually willing to give it, and that holds up when the questions start. Get the problem, the market size, the traction, and the ask right, and the rest of the deck mostly exists to support those four pillars.

If you want a pitch deck built around numbers that will actually survive investor scrutiny, Oak Business Consultant’s investor-ready pitch deck services and financial modeling work go hand in hand, since the strongest decks are built on a credible financial story, not just good slide design. Book a call and we’ll help you put together a deck that’s ready for the room.