Are Golf Courses Profitable?

The Profitability of Golf Courses: What You Need to Know

Golf carries an image of exclusivity and leisure, but behind every manicured fairway sits a capital-intensive small business with thin margins and a lot of moving parts. So, are golf courses profitable? The honest answer is: some are, many aren’t, and the difference is measurable. Industry benchmarks put average golf course EBITDA at roughly 15% of revenue, which on a typical course’s books works out to a few hundred thousand dollars a year, before accounting for the capital reserves that fairway, green, and irrigation upkeep demand.

Whether you’re evaluating a purchase, operating a course today, or sizing up the golf industry as an investment category, this guide breaks down where the money actually comes from, where it leaks out, and what separates a course that compounds cash flow from one that limps along at breakeven.

The state of the golf industry today

Golf’s participation numbers are genuinely strong. The National Golf Foundation has tracked steady growth in on-course play since the pandemic, with off-course formats like Topgolf and simulator venues pulling in younger, more diverse players who eventually convert to traditional rounds. Utilization at public facilities, which sat below 50% before COVID, has climbed toward roughly 69% today, and pre-pandemic overbuilding has mostly worked itself out: annual course closures fell to around 90 in 2023, down from nearly three times that a decade earlier.

The supply side matters just as much as demand. The U.S. has roughly 15,963 golf courses, and about 70% of them are public. That’s a lot of competing tee sheets in most metro markets, which is exactly why the operators who treat pricing and cost structure as a discipline, not a formality, are the ones pulling ahead of the pack. Demand is there. The question, as it always is in this business, is whether an operator has built a financial model that actually captures it.

Are golf courses profitable? Understanding the business model

No, not by default. A golf course is a capital-intensive, seasonally exposed business with high fixed costs, and roughly 8-14% of courses report real financial struggle in any given year depending on whether they’re public or private. But when it’s run with a clear pricing strategy and disciplined cost control, a golf course can throw off strong, recurring cash flow.

Profitability comes down to three levers: which revenue streams an operator activates, how tightly costs are controlled, and what type of facility it runs.

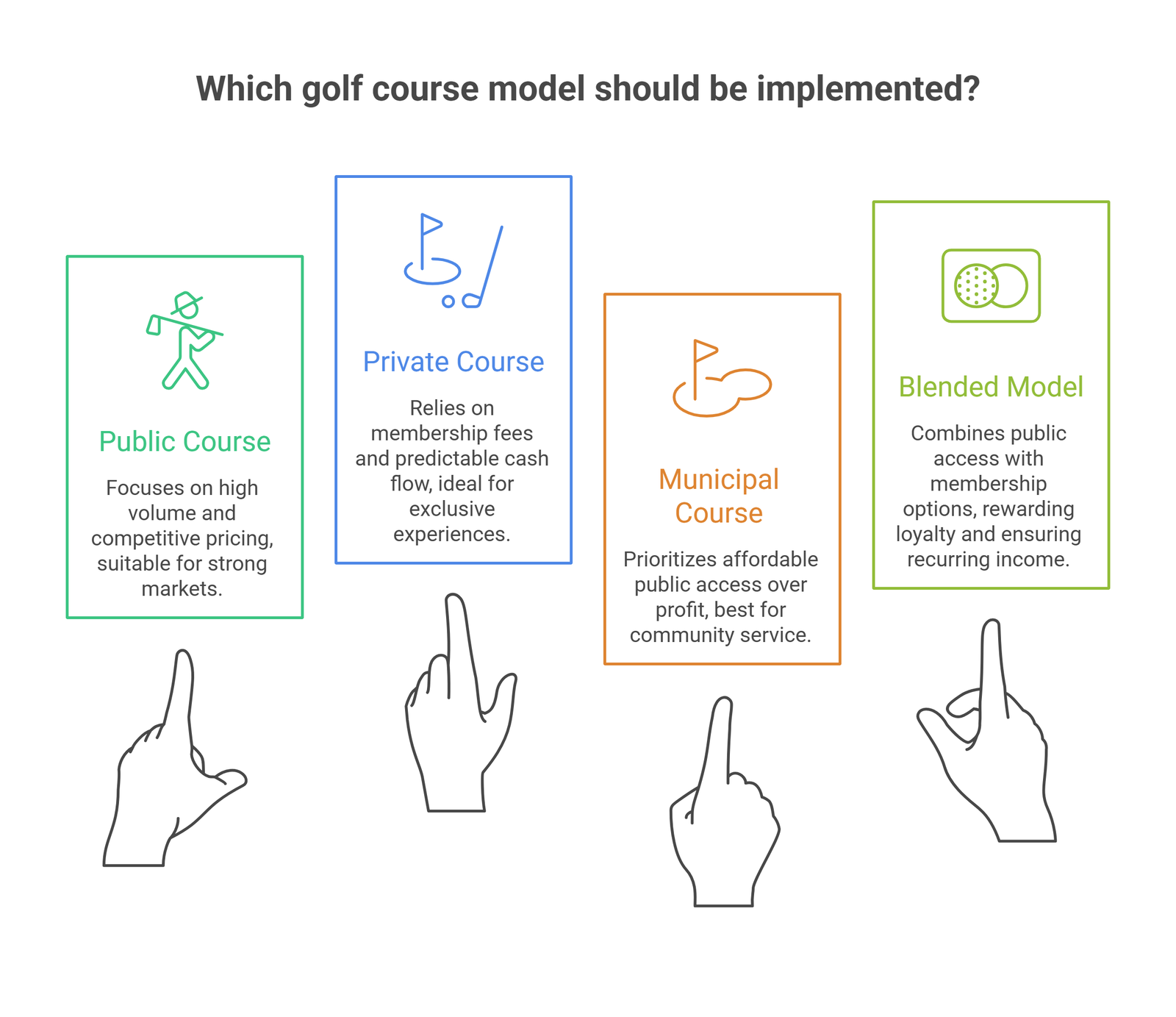

Public, private, and municipal: the bottom-line differences

A public golf course sells no memberships. It earns through green fees, cart fees, food and beverage, and merchandise, and it lives or dies on tee-sheet volume. Margins run thinner here because pricing is competitive and weather-dependent, but a well-positioned public course in a strong market is consistently profitable.

A private golf course runs on membership economics: initiation fees, ongoing dues, and event hosting to a captive base of paying members. Cash flow is more predictable, but member expectations for facility quality push costs up in parallel.

Municipal courses are a distinct third category. Most are financed through enterprise funds designed to cover operating costs from user fees rather than to generate a profit for shareholders, which means their operators are often optimizing for affordable public access, not net income. That mission difference is worth understanding before comparing a municipal course’s numbers to a for-profit daily-fee operation; they’re not playing the same game.

Some of the strongest operations blend models entirely: public access layered with a tiered membership structure that rewards loyalty and locks in recurring income. Industry consultants also classify facilities on a platinum-to-steel spectrum, where platinum properties command the highest fees and steel facilities compete purely on price and access. Knowing which tier a course occupies (or should occupy) shapes every pricing and cost decision that follows.

What golf course profit margins actually look like

This is the number most golf course guides skip, and it’s the one that actually answers “are golf courses profitable”: industry benchmarking puts average golf course EBITDA margin at around 15% of revenue. Applied to average per-course revenue nationally, that works out to roughly $250,000-$260,000 in annual EBITDA for a typical facility, a real number, but one that has to absorb depreciation on equipment, clubhouse repairs, and periodic course renovation before anyone sees a distribution.

That capital reserve requirement is not small. A full golf course renovation can run into eight figures, and industry associations generally recommend an annual capital reserve well into six figures to keep pace with the wear on greens, irrigation, bunkers, and fairways. Skip that reserve and a course can look profitable on an income statement while quietly falling behind on the asset condition that its revenue depends on.

| Profitability driver | What it typically looks like |

| Industry-average EBITDA margin | Roughly 15% of total revenue |

| Facilities reporting financial struggle | ~8% of public courses, ~14% of private clubs in a given year |

| Recommended annual capital reserve | Six figures at minimum, scaling with course size and renovation cycle |

| Public facility utilization (post-COVID) | ~69%, up from under 50% pre-pandemic |

| U.S. course closures (2023) | ~90, roughly one-third of the pre-pandemic annual rate |

The takeaway: golf course economics are closer to a real estate-adjacent operating business than a high-margin service business. The land underneath the course is often the real long-term store of value, while the operating business itself needs disciplined pricing and cost management just to clear a respectable margin.

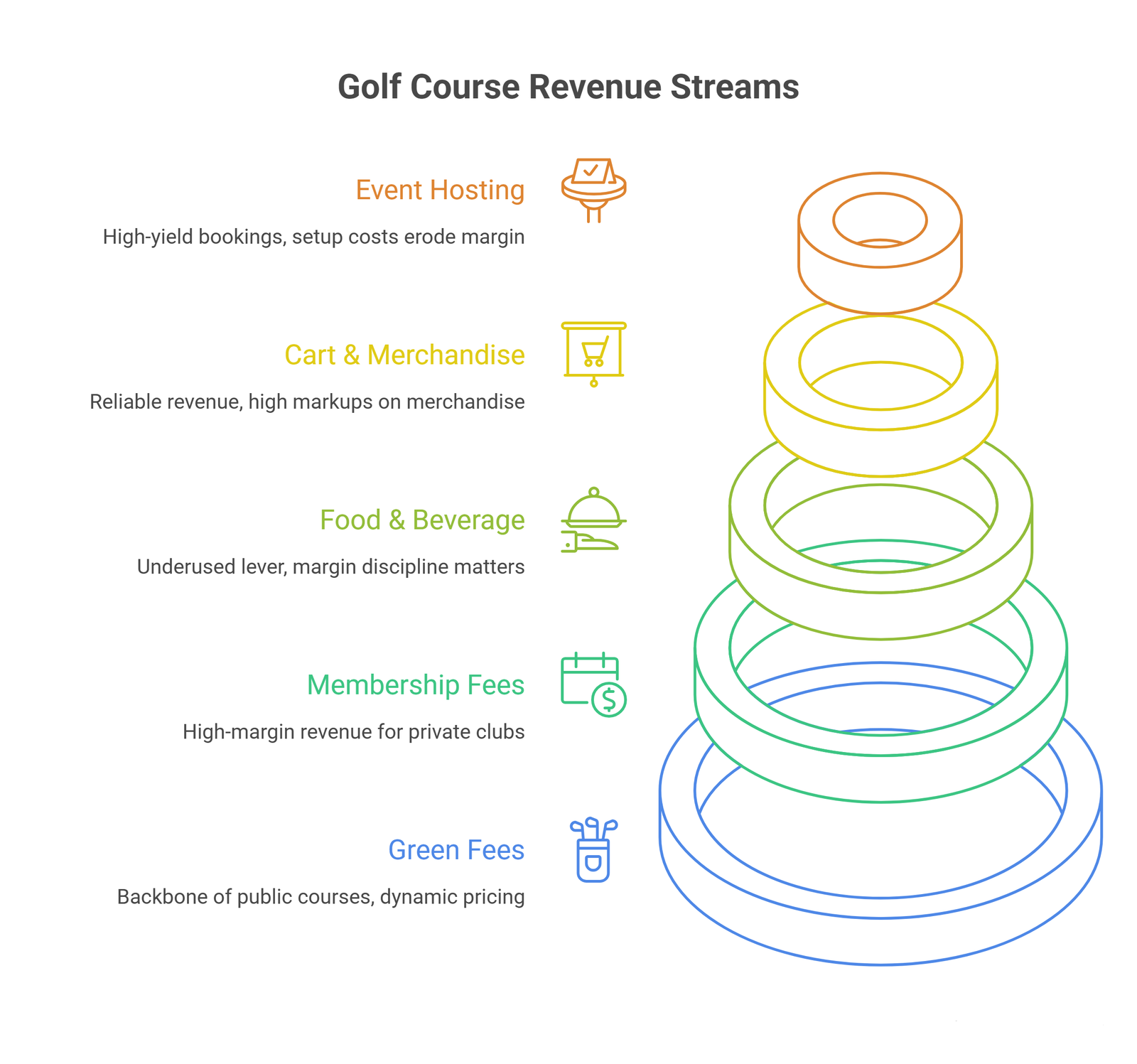

Primary revenue streams for golf courses

Understanding where a golf course actually makes money is essential to answering whether a given course is profitable.

Green fees and tee times

Green fees are the backbone of any public-facing course, and dynamic pricing (charging more for peak slots, less for off-peak) is now standard practice, borrowed directly from airline and hotel revenue management. Platforms like Lightspeed Golf and tee-time marketplaces let operators automate this and capture bookings online instead of leaving inventory to walk-up traffic.

One thing many operators get wrong here: tee time economics aren’t proportional to price. A discounted evening slot can be more profitable per hour than a premium midday round if it fills a gap that would otherwise sit empty, because once fixed costs are covered, an additional player adds almost pure margin. That’s also the logic behind why over-discounting hurts more than it seems to on paper: a golf course with too many overlapping player categories, punch cards, and loyalty tiers ends up leaving significant yield on the table simply because pricing has become too complicated to optimize.

Membership fees and membership dues

For private and semi-private clubs, membership is the highest-margin line on the books. Upfront initiation fees plus recurring dues create a predictable revenue floor that supports year-round operational planning. Structuring tiered packages, from junior memberships to full family access, widens the addressable market, and a loyalty program built around frequency and referrals (not blanket discounting) strengthens retention without eroding yield.

Food and beverage sales

F&B is consistently one of the most underused revenue levers in golf. At well-run courses, food and beverage sales can account for 20-35% of total revenue, but public-facility food and beverage cost of goods sold typically runs around 40%, so the margin discipline here matters as much as the top-line number. Operators who invest in the clubhouse restaurant and halfway house, rather than treating them as an afterthought, consistently see it show up in the bottom line.

Cart fees and merchandise sales

Cart fees add reliable per-round revenue with no incremental staffing cost, particularly when carts are required during peak hours. Pro shop merchandise is its own business within the business: typical markups run 20-30% on hard goods and equipment, at least 52% on apparel, and can exceed 100% on accessories, with average golf shop merchandise sales in the $200,000-$300,000 range for a mid-sized operation. An e-commerce extension of the pro shop turns that into a year-round revenue stream instead of a walk-in-only one.

Event hosting and wedding services

Corporate tournaments, charity fundraisers, and weddings leverage a course’s natural scenery for some of the highest-yield bookings available. Tools like Cvent’s supplier network and event diagramming software help convert inquiries efficiently. A single large corporate outing or wedding can generate the equivalent of several days of green fee revenue in one booking, but events also carry real setup, staffing, and insurance costs that erode the margin if the booking is thin on attendance.

The hidden revenue leak: no-shows

Here’s a cost that rarely makes it into golf course financial planning conversations: no-shows. Research from tee-time technology provider Notefy, conducted jointly with Metolius Golf, found that roughly 9% of public tee times go unused as no-shows, and that this costs the average golf course approximately $142,500 in lost annual revenue. That’s a material chunk of the EBITDA benchmark discussed above, essentially disappearing before a single additional cost is incurred to serve those players.

The fix isn’t complicated: requiring a card on file, charging a modest non-refundable reservation fee, or suspending booking privileges for repeat no-shows all meaningfully close the gap. Courses that have adopted 100% online booking with reservation deposits report meaningfully lower no-show rates than walk-up or phone-booked tee sheets.

The cost side: why many golf courses struggle

If demand is strong and no-shows are fixable, why do so many courses still underperform? The cost side of the ledger is unforgiving.

Maintenance and inputs. Turf management, irrigation, mowing equipment, fertilizer, and water represent the largest fixed costs for most operations. A course in an arid climate can spend dramatically more on irrigation than one in a naturally wet region, which changes the entire financial model for that specific property.

Land, real estate taxes, and capital expenditure. For many courses, the land itself is the most valuable, and most heavily taxed, asset on the balance sheet. Renovating a clubhouse, upgrading irrigation, or reworking fairways all require capital that’s often financed with debt, and that debt service has to be paid whether or not the renovation moves the revenue needle.

Insurance and liability. Property damage, employee injury, and guest liability coverage are easy to underestimate until a course has a claims history or sits in a region prone to floods, hurricanes, or wildfire, at which point premiums climb fast.

Financing friction. Buying a golf course is a real estate transaction wrapped around an operating business, and traditional bank lenders are notably reluctant to finance golf course purchases, particularly for first-time owners. That scarcity of financing options shapes deal structure and timelines more than most first-time buyers expect.

Aging membership bases. Private clubs in particular are exposed to demographic risk: as long-tenured members age out of frequent play or resign outright, revenue erodes unless the club is actively recruiting a younger member pipeline to replace them.

Golf management companies exist precisely because this cost side is where independent owners most often lose control. These firms bring purchasing power, standardized labor models, and the operating systems that make the difference between a profitable course and one that’s perpetually cash-flow negative.

Golf course technology and operational efficiency

Modern operations lean on technology to protect both revenue and margin. Self-service check-in kiosks reduce front-desk staffing without hurting the customer experience. Golf simulators and TopTracer-style range installations extend playable hours into evenings and bad-weather days, capturing revenue that would otherwise be lost to daylight and climate. Course management systems give operators real-time data on utilization and player behavior, which feeds directly into smarter pricing strategies and promotional decisions rather than gut-feel discounting.

Point-of-sale, tee-time, and membership management increasingly live on a single integrated platform, which matters more than it sounds: fragmented systems make it hard to see which revenue streams are actually carrying the business, and that visibility gap is often the real reason underperforming courses stay underperforming.

Buying a golf course: due diligence essentials

For anyone considering a purchase, thorough due diligence is non-negotiable, and it goes well beyond a trailing income statement. Are golf courses profitable as acquisitions? They can be, but purchase price, existing debt, deferred maintenance, and local competitive dynamics determine the outcome far more than the sport’s overall popularity does.

Key due diligence items: review the equipment and plant register for the condition of maintenance assets, investigate any litigation or winding-up history, audit membership contracts and outstanding dues commitments, evaluate the existing financial model alongside at least three trailing years of cash flow, and assess the competitive landscape and remaining useful life of the course’s core infrastructure. Given how difficult conventional financing can be to secure for a golf property, lining up capital early in the process, rather than after a letter of intent, tends to separate deals that close from deals that stall.

A structured SWOT analysis, examining strengths, weaknesses, opportunities, and threats, should accompany any offer, alongside a clear view of the exit strategy: operate long-term, reposition for real estate development, or resell to a golf management company. That endgame shapes every decision made from day one of ownership.

Are golf courses profitable in today’s market?

Returning to the central question: rounds played and total spending at golf facilities remain elevated above pre-pandemic levels, and the courses capturing that demand most effectively share a consistent profile. They diversify revenue across green fees, food and beverage, events, and memberships rather than depending on any single stream. Additionally, they manage no-shows and pricing complexity as actively as they manage turf. They reserve capital for renovation instead of deferring it. And they adopt the technology that turns raw demand into captured revenue rather than leaving it on the tee sheet.

Frequently Asked Questions

What is a good profit margin for a golf course?

Industry benchmarking places average golf course EBITDA margin at roughly 15% of revenue. Well-run, well-positioned courses can exceed that, while courses with weak pricing discipline, high no-show rates, or deferred maintenance often fall well below it, or operate at breakeven once capital reserves are accounted for.

What is the average revenue of a golf course?

Average annual revenue varies widely by type and location. A modest public course might generate $500,000 to $1.5 million per year, while a well-positioned private or resort course can generate $3 million to $10 million or more. National average revenue per course is estimated in the range of $1.5-1.8 million, with green fees, membership dues, food and beverage, and event hosting all contributing.

How many golf courses actually lose money?

Roughly 8% of public courses and 14% of private clubs report financial struggle in a typical year, according to National Golf Foundation data, a meaningfully better picture than a decade ago, though far from universal profitability.

What is the 70/30 rule in golf?

The 70/30 rule is a general guideline that roughly 70% of a golf course’s revenue should come from core golf operations (green fees, cart fees, membership dues) and 30% from ancillary sources (food and beverage, merchandise, event hosting). Courses that successfully grow that ancillary 30% tend to be noticeably more profitable overall.

How do golf courses make a profit?

By maximizing revenue across tee times, memberships, food and beverage, cart fees, merchandise, and events, while controlling fixed costs like labor, maintenance, and water. Dynamic pricing, no-show mitigation, and disciplined membership sales all move the needle materially.

Conclusion

Are golf courses profitable? Yes, when pricing discipline, cost control, and revenue diversification are actually in place, not assumed. The margin math is tighter than golf’s glamorous reputation suggests: a 15% EBITDA benchmark, real capital reserve obligations, and revenue leaks like no-shows all separate the courses that compound value from the ones that quietly bleed cash while looking busy on the tee sheet.

Whether you’re evaluating a purchase, tightening the numbers on an existing operation, or exploring golf-adjacent real estate development, the difference between those two outcomes almost always comes down to who’s actually running the financial side of the business.

Our team at Oak Business Consultant works with golf course owners, operators, and investors on the financial modeling, business valuation, and accounting and bookkeeping work that underpins a genuinely profitable golf operation, from acquisition due diligence through ongoing cash flow management. If you’re weighing a purchase, our guide on when it makes sense to sell a business is a useful companion read for the other side of that decision. Talk to our Fractional CFO team about building the financial foundation your golf business needs to thrive.