How to Calculate Loan Amortization

Loan Amortization

Results:

A Comprehensive Guide to Understanding Amortization for Entrepreneurs

If you’ve taken out a mortgage loan, a personal loan, or even an auto loan, you’re probably thinking about how to manage monthly payments and track your principal balance over time. Fortunately, there’s an easy way to stay on top of your loan payments: amortization. With the help of an amortization calculator, you can break down your payments into manageable chunks and understand exactly how your loan balance decreases over time.

The Amortization Calculator by Oak Business Consultant enables you to easily analyze your loan payments, track principal reduction, and optimize your financial planning effectively.

What is Amortization?

At its core, amortization refers to the process of paying off a loan over a specific period, with regular payments made to reduce the loan balance. Each payment you make typically covers two main components: interest and principal. Early in the loan term, most of your monthly payment goes toward interest, with the rest covering the principal loan balance. Over time, as you continue to pay down your loan, the proportion of your payment that goes toward principal increases while the amount going toward interest decreases.

If you’re thinking of buying a house, taking out a business loan, or financing a car, understanding how amortization schedules work can save you time and money. Amortization calculators are perfect tools for helping you figure out how long it will take to pay off your loan, the breakdown of loan payments, and how extra payments could impact your mortgage loan or any other secured loans.

How Does an Amortization Calculator Work?

An amortization calculator is a powerful tool designed to help borrowers calculate monthly mortgage payments, understand how payments are distributed between principal payments and interest charges, and see how their loan balance decreases over time. This tool is especially helpful for users who need to calculate mortgage amortization schedules for different loan types, such as fixed-rate loans, student loans, auto loans, and personal loans.

Key Inputs Needed:

To use the amortization calculator, you will need to input the following details:

- Loan amount (also known as the principal balance)

- Annual interest rate (the interest rate charged on the loan)

- Loan term (the number of years or loan term for repayment)

- Payment frequency (typically monthly payments, but could be biweekly or annual payments)

Once you input these factors, the calculator will use the following loan amortization formula to determine your monthly payment and create an amortization schedule:

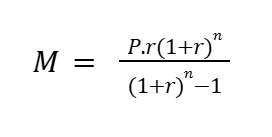

Amortization Formula:

The formula used to calculate the monthly payment for a fixed-rate loan is:

Where:

- M is the monthly payment.

- P is the loan amount (principal balance).

- r is the monthly interest rate (annual interest rate divided by 12).

- n is the loan term in months (loan term in years multiplied by 12).

Amortization Schedule Breakdown:

Once the monthly payment is calculated, the amortization calculator provides a detailed breakdown showing how much of each payment goes toward the principal and how much is allocated to interest. In the early stages of the loan, the interest portion is typically higher, but as you continue to make payments, a greater portion goes toward principal payments and reducing the loan balance.

Example Scenario:

Imagine you take out a $300,000 mortgage loan at a 4% annual interest rate for a 30-year term. The monthly payment calculated by the mortgage amortization calculator would be approximately $1,400. In the first few years, the majority of the payment would go toward covering the interest rate, with only a small portion reducing the principal balance. However, over time, more of the payment will go toward reducing your outstanding balance. If you decide to make extra payments or pay biweekly instead of monthly, you can pay off the loan faster and reduce the total amount of interest paid over the life of the loan.

Why Should You Care About Amortization?

When it comes to managing loans—whether it’s a mortgage loan, personal loan, auto loan, or business loan—understanding amortization is crucial. It’s not just about making your monthly payments on time. Knowing how amortization works can have a huge impact on your financial health, savings, and ability to manage debt over time.

Here’s why you should care about amortization and how it can influence your loan payments, principal balance, and overall financial goals.

1. Helps You Understand Your Monthly Loan Payments

Understanding amortization is essential because it gives you a clear breakdown of your monthly mortgage payments, personal loan payments, or any other loan payments you’re making. Every payment you make is divided into two parts: interest and principal. In the early stages of most loans, the majority of your monthly payment goes toward interest, not the principal balance. Over time, more of your payment goes toward reducing the principal.

By reviewing your amortization schedule, you’ll see exactly how much of your payment is going to interest and how much is chipping away at the loan balance. This is especially helpful for understanding how much interest you’ll pay over the life of the loan.

2. Helps You Plan for the Future and Budget Better

If you’re making a mortgage loan payment or repaying student loans, having a clear understanding of amortization allows you to budget more effectively. Knowing your exact monthly payment allows you to manage other financial responsibilities like property taxes, insurance, and even debt-to-income ratio.

With amortization schedules, you can easily anticipate how your loan will evolve. You’ll know how long it will take to pay off the principal and what portion of your loan payment is earmarked for interest over the term. This clarity can help prevent any surprises in the future and ensure you’re always prepared for upcoming financial commitments.

3. Optimizes Debt Repayment and Saves on Interest

One of the most powerful benefits of understanding amortization is the ability to save money on interest. By making extra payments—whether they’re monthly payments that are higher than your regular amount or periodic extra payments—you can reduce the amount of interest you pay over the life of the loan and shorten the loan term.

For instance, if you make an extra payment toward your mortgage loan or auto loan, the principal balance decreases faster. As a result, less interest is applied to your remaining balance. Over time, you’ll pay off your loan quicker, reducing the total amount of interest you owe. This works particularly well with loans that have fixed rates where the interest is calculated based on the remaining balance.

4. Allows You to Calculate the Total Loan Costs

With an amortization schedule, you can calculate the total loan costs—how much you’ll pay for the loan over its entire term. This gives you the ability to forecast how much interest will be paid at various stages of the loan, whether you’re looking at mortgage amortization or personal loan amortization.

For example, on a 30-year fixed-rate mortgage, you may see that for the first few years, most of your monthly payment goes toward interest. In fact, it may take years before you start to see a significant reduction in your principal balance. Understanding this allows you to make more informed decisions about whether to refinance, adjust your loan payments, or make extra payments to reduce your debt faster.

5. Improves Financial Control and Flexibility

When you have a clear understanding of amortization, you gain better control over your finances. Whether you’re an entrepreneur managing business loans or a homeowner with a mortgage loan, amortization empowers you to make decisions based on solid knowledge. By understanding how your payments are structured, you can assess whether increasing your monthly payment or making extra payments might fit better with your current financial situation.

For example, if you’re able to make an extra $100 per month in your mortgage payment, it can help you pay off your loan years earlier and save a significant amount of interest. Likewise, if you have a variable-rate mortgage or an adjustable-rate loan, understanding amortization can help you evaluate whether refinancing or switching loan types might be a better option as rates change.

6. Prepares You for Future Borrowing

When you’re dealing with student loans, auto loans, or any other form of secured debt, understanding amortization schedules prepares you for future borrowing. By grasping how loan repayments work, you’ll have a better sense of how much principal balance you’ll owe at different points in time, how interest rates impact the overall loan cost, and how to leverage loan calculators to evaluate new loan terms.

For instance, when considering a 30-year fixed-rate mortgage or even a personal loan, knowing how the amortization schedule works will help you weigh whether the loan’s term is too long or too short for your financial needs. Understanding your amortization plan will let you evaluate different options that meet your financial goals, whether that’s paying off a mortgage loan or funding your business loans.

7. Fosters Better Financial Strategy for Entrepreneurs

For entrepreneurs or business owners, understanding loan amortization isn’t just about managing business loans—it’s about financial strategy. By incorporating extra payments into your loan amortization plans, you can lower your outstanding balance faster, which will help improve your business’s debt-to-equity ratio and strengthen its credit profile. This can lead to better lending terms when it comes time to apply for another loan or business financing.

With a clear understanding of amortization, you’re also in a stronger position to manage property taxes, insurance costs, and other essential loan-related expenses. This insight enables you to make data-driven decisions for the growth and longevity of your business.

8. Increases Your Overall Financial Awareness

Amortization isn’t just a number on a page. It’s a key part of understanding your finances. Whether you’re dealing with a mortgage loan, student loan, auto loan, or business loan, you’re better equipped to make smart financial moves when you know how to manage your loan payments and principal balance effectively.

The more you understand how amortization works, the better prepared you’ll be to manage debt, reduce interest costs, and maintain financial flexibility for the future.

Key Terms You Should Know in Amortization

When dealing with amortization, there are a few important terms you need to know. Here’s a breakdown:

1. Principal Balance

This is the total amount you’ve borrowed. It’s the loan balance that is reduced over time with each monthly payment. Early in your loan term, most of your payments are applied to interest, but over time, more of your payments go toward paying down the principal balance.

2. Interest

Interest is the cost you pay for borrowing money. It’s expressed as a percentage (called the annual interest rate) of your loan balance. The higher the interest rate, the more you’ll pay in interest over the life of the loan. As your loan balance decreases, the amount of money you pay toward interest also decreases.

3. Loan Term

This is the duration of your loan—usually expressed in years. Common loan terms are 30-year fixed-rate mortgages or 15-year loans, though the term can vary depending on the type of loan.

4. Extra Payments

Making extra payments toward your loan balance reduces the amount you owe faster. By paying more than your required monthly mortgage payment, you can cut down on the total interest and pay off your loan ahead of schedule. Using an amortization calculator helps you see the impact of extra payments on your loan.

5. Amortization Schedule

An amortization schedule is a detailed breakdown of your loan payments over the entire term. It shows how much of each payment is applied to interest and how much goes toward the principal loan balance. You can use this schedule to track your outstanding balance and to understand how your loan payments change over time.

Different Types of Loans and Their Amortization

When it comes to financing, whether you’re buying a home, funding a business, or making a large purchase, loans come in various shapes and sizes. Each type of loan has its own amortization structure, which impacts how your monthly payments are calculated and how much you’ll pay over the loan term. Understanding the differences between these loans can help you make smarter decisions about loan payments, interest rates, and the overall loan term. Here’s a breakdown of the most common types of loans and how amortization works for each.

1. Mortgage Loans: 30-Year Fixed vs. Adjustable-Rate

Fixed-Rate Mortgages (FRM)

A fixed-rate mortgage is one of the most common types of loans for homebuyers. With a 30-year fixed-rate mortgage, your interest rate remains the same throughout the loan term, and your monthly payment remains consistent. However, how your loan payments are applied changes over time because of amortization.

In the early years, a significant portion of your monthly mortgage payment will go toward paying off interest rather than the principal balance. As the years go by, more of your payment will be applied to the principal, reducing your outstanding balance faster.

Key terms to know:

- Amortization schedule: Shows how much of each payment goes toward interest and how much is applied to the principal balance.

- Fixed-rate loans: The interest rate remains constant for the entire loan term.

Adjustable-Rate Mortgages (ARM)

An adjustable-rate mortgage (ARM) typically has a lower interest rate in the early years compared to a fixed-rate mortgage. However, the interest rate can adjust after an initial period, making your loan payments fluctuate. This affects the amortization schedule, especially if rates increase.

With an ARM, amortization works similarly to a fixed-rate loan in the beginning. But as the interest rate changes, your monthly payments may increase, which can extend your loan term or increase the total interest you’ll pay over time.

Key terms to know:

- Annual percentage rate (APR): The total cost of your loan, including interest, expressed as a yearly rate.

- Amortization calculator: A tool to help you understand how interest rates and monthly payments affect your loan over time.

2. Personal Loans

Personal loans are typically unsecured loans used for various purposes, such as consolidating credit card debt, funding home improvement projects, or covering personal expenses. These loans can have either fixed or variable interest rates.

Fixed-Rate Personal Loans

For a fixed-rate personal loan, the interest rate stays the same throughout the loan term, meaning your monthly payment remains consistent. Similar to a mortgage, a portion of your payment goes toward interest, and the remainder reduces the principal balance.

Key terms to know:

- Loan balance: The amount you still owe on your loan.

- Principal balance: The amount of the loan before interest is added.

Variable-Rate Personal Loans

With a variable-rate personal loan, your interest rate can change over time, which will affect your amortization schedule. When interest rates increase, a larger portion of your monthly payment will go toward interest rather than reducing your principal balance.

3. Auto Loans

Auto loans are used to finance the purchase of a vehicle, and these loans typically have a term of 3 to 7 years. Like mortgages, auto loans come with fixed rates and amortization schedules.

Fixed-Rate Auto Loans

With a fixed-rate auto loan, your interest rate and monthly payments remain the same throughout the loan term. The amortization schedule for auto loans is similar to that of a mortgage loan, where the early payments go mainly toward interest, and the later payments go more toward reducing the principal balance.

Key terms to know:

- Amortization period: The duration over which you’ll repay your loan.

- Secured loans: Auto loans are typically secured by the vehicle itself, meaning the lender can repossess the car if you default.

4. Student Loans

Student loans are designed to help pay for education expenses. They come with amortization schedules that differ based on whether the loan is a federal student loan or a private student loan.

Federal Student Loans

Federal student loans generally offer favorable interest rates and repayment terms. Some loans, like Direct Subsidized Loans, don’t accumulate interest while you’re in school, and the amortization begins once you graduate or drop below half-time enrollment.

The repayment term for federal student loans typically ranges from 10 to 25 years, depending on the type of loan and repayment plan you choose. Understanding your amortization schedule can help you determine when your loan balance will be paid off and how much you’ll owe in interest over time.

Key terms to know:

- Income-driven repayment plans: Adjust your monthly payments based on your income and family size.

- Deferment: Temporarily pauses payments on your loan without adding more interest.

Private Student Loans

Private student loans, offered by banks or other private lenders, often come with variable rates and fixed rates. These loans typically have a set amortization schedule, but the terms can vary widely depending on the lender. Private student loans may also have shorter loan terms, meaning your monthly payments could be higher than those of federal loans.

Key terms to know:

- Private loan terms: The interest rate, loan term, and repayment options can vary from one lender to another.

5. Business Loans

For entrepreneurs, business loans can provide the capital needed to grow or start a business. The amortization of business loans depends on the type of loan and the terms agreed upon with the lender.

SBA Loans

Small Business Administration (SBA) loans are typically long-term loans with low interest rates and favorable amortization schedules. These loans are often repaid over a term of 10 to 25 years, and the loan balance decreases steadily over time.

Key terms to know:

- SBA loan terms: The repayment period for SBA loans typically ranges from 7 to 25 years, depending on the nature of the business and the type of SBA loan.

Traditional Business Loans

Traditional business loans from banks typically have fixed rates and amortization schedules similar to personal loans. Depending on the agreement, these loans may have a short-term repayment structure, or they may extend over a longer period. As with other loans, extra payments can help reduce the total amount of interest paid.

6. Payday Loans and Short-Term Loans

Payday loans are short-term loans typically used to cover immediate, emergency expenses. They usually have high interest rates and don’t follow traditional amortization schedules. Instead, they require full repayment by the borrower’s next payday.

Amortization on Payday Loans

Unlike traditional loans, payday loans often don’t feature an amortization schedule. You must repay the full loan amount, plus interest, by the due date. These loans can be risky due to their high interest rates and fees.

Key terms to know:

- Short-term loans: Loans meant to be paid off quickly, usually in 30 days or less.

- Annual percentage rate (APR): The true cost of borrowing, including fees and interest.

How Extra Payments Can Impact Amortization

One of the most effective ways to save money on your loan is to make extra payments. By paying more than the minimum required, you can reduce your principal balance faster, which means you’ll pay less interest over the life of the loan. Using an amortization calculator, you can see exactly how making extra payments impacts your loan balance and how much you can save.

Example:

Imagine you have a $200,000 mortgage loan with a 4% interest rate and a 30-year term. By making an extra $200 per month, you could shave several years off your loan term and save thousands of dollars in interest. With an amortization calculator, you can test different extra payment scenarios to find the best strategy for paying off your loan.

Frequently Asked Questions

How does an amortization schedule work?

An amortization schedule shows how each payment is split between principal and interest, with the principal portion increasing over time.

What’s the difference between principal and interest payments?

Principal payments reduce the loan balance, while interest payments cover the lender’s cost for the loan.

What is a monthly amortization schedule?

It shows your monthly loan payments, broken down into principal and interest, for the duration of the loan.

What is a fixed-rate loan amortization schedule?

In a fixed-rate loan, monthly payments stay the same, with more of each payment going toward the principal over time.

What are balloon loans in amortization?

A balloon loan has smaller monthly payments with a large final payment due at the end of the term.

What’s the difference between amortized and conventional loans?

Amortized loans reduce the principal over time through regular payments. Conventional loans are not government-backed and can be amortized.

What happens if I make extra payments?

Extra payments reduce your loan balance faster, decreasing interest and shortening the loan term.

Does property tax impact amortization?

Property taxes are not part of the amortization schedule but are often included in monthly mortgage payments.

What is mortgage insurance?

Mortgage insurance protects the lender in case of default and adds to your monthly payment but doesn’t affect amortization directly.

How does loan type affect amortization?

Different loans (e.g., fixed-rate, adjustable-rate, or balloon loans) affect how payments are applied and the loan term.

What factors influence the amortization period?

Factors include loan amount, interest rate, and loan type, which affect your monthly payment and term.

How does the interest rate impact amortization?

A higher interest rate increases monthly payments and total interest paid, while a lower rate reduces both.

Conclusion

Understanding amortization is crucial for anyone managing a loan—whether it’s a mortgage loan, an auto loan, or a personal loan. An amortization calculator helps you break down your loan payments, track your principal balance, and plan your finances more effectively. By using an amortization schedule and making extra payments, you can pay off your loan faster and save money on interest. Take control of your finances today and make smart decisions to reach your financial goals.