Total Variable Cost Formula: A Guide for Business Owners

Total Variable Cost Formula Explained for Better Cost Control

Every business owner needs to know where money goes. Whether you run a small shop or a growing company, understanding how costs behave is the foundation of smart financial decisions. One of the most useful tools in cost accounting is the total variable cost formula. It helps you see exactly how much your spending changes as your production volume changes. And when you understand that, everything else gets clearer.

What Is Total Variable Cost?

Total variable cost refers to all the costs that change directly with your level of production. When you produce more units, these costs go up. When you produce less, they go down. This is what separates them from fixed costs, which stay the same no matter how much you produce.

Think of it this way. Your rent is a fixed cost. You pay the same amount whether you make 10 products or 10,000. But your raw materials change every time. If you need more wood to make more chairs, your material spending goes up with every additional unit. That is a variable expense.

Common examples of variable expenses include:

- Raw materials used in production

- Direct labor paid per unit or per hour worked

- Packaging costs for each item shipped

- Sales commissions earned when a sale is made

- Utility costs that spike with production activity

- Credit card processing fees based on transaction volume

The Total Variable Cost Formula

The total variable cost formula is straightforward:

Total Variable Cost = Variable Cost Per Unit x Units Produced

That is the core equation. If each unit you produce costs $12 in variable expenses, and you produce 500 units, your total variable cost is $6,000.

You can also break it down by cost type to see where spending is concentrated:

Total Variable Cost = Total Cost of Materials + Total Cost of Labor + Other Variable Expenses

This second version is helpful when you want to identify which category is eating up the most budget. It gives you a detailed view of your cost structure rather than just a single number.

Variable Cost Per Unit Formula

Before you can use the total variable cost formula, you need to know the variable cost per unit. Here is how you calculate it:

Variable Cost Per Unit = Total Variable Cost / Units Produced

This works in reverse too. If you know your total spending on variable inputs and how many units came out of that process, you can find the average cost per item. This number is critical for pricing decisions and understanding your profit margins.

Variable Cost Calculation Example

Let us walk through a simple example to make this concrete.

Imagine a small manufacturer that produces handmade candles. In one month, the company produces 2,000 candles. Here is a breakdown of their variable expenses for that period:

- Raw materials (wax, wicks, fragrance): $4,000

- Direct labor (production wages paid per candle): $2,000

- Packaging costs: $600

- Energy costs tied to production equipment: $400

Total variable cost = $4,000 + $2,000 + $600 + $400 = $7,000

Variable cost per unit = $7,000 / 2,000 = $3.50 per candle

Now the owner knows that every candle costs $3.50 in variable expenses to produce. This number feeds into pricing, contribution margin calculations, and break-even analysis.

Average Variable Cost

Average variable cost (AVC) is closely related to variable cost per unit. The formula is:

Average Variable Cost = Total Variable Cost / Production Output

This metric shows how your per-unit costs behave as you scale. In many businesses, the average variable cost drops as production volume increases. This is because you negotiate better material prices, workers get faster with practice, and processes become more efficient. This is one reason why scaling production can improve profit margins.

However, at some point, pushing production too hard can cause average variable cost to rise again. Equipment wears out faster, overtime kicks in, or quality problems create rework costs. Understanding where this inflection point sits in your operation is valuable.

Total Cost Formula

To see the full picture, combine variable and fixed costs:

Total Cost = Total Fixed Costs + Total Variable Cost

Total fixed costs include things like rent, insurance, salaried employee salaries, and equipment depreciation. These do not change with activity levels.

Total variable cost, as discussed, moves with production levels.

Adding them together gives you total cost, which you need to calculate the cost of goods sold, set prices, and project cash flow at different production levels. This figure flows directly into your income statement and forms the backbone of your profitability tracking.

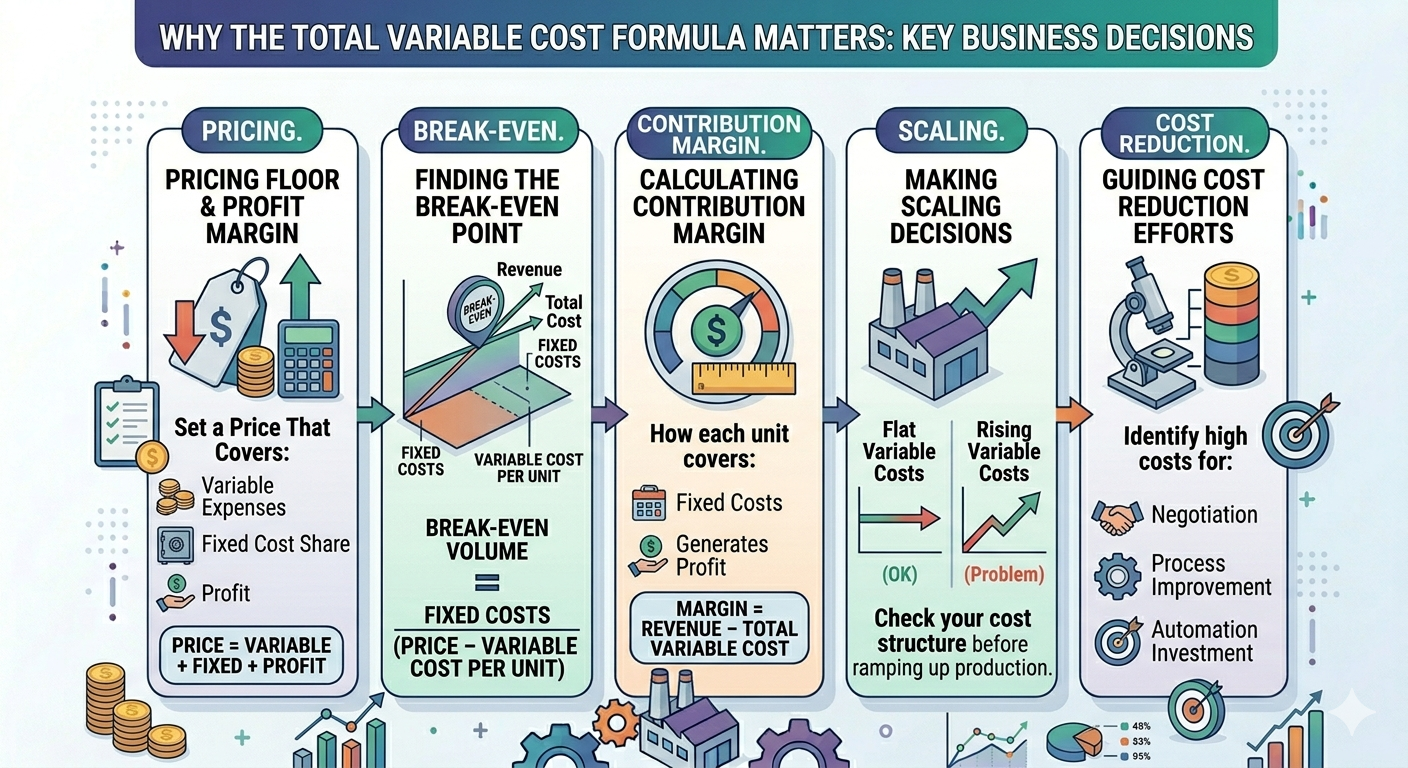

Why the Total Variable Cost Formula Matters

Knowing your total variable cost is not just an accounting exercise. It drives real decisions.

Pricing. If you do not know what each unit costs to produce, you cannot price it correctly. The total variable cost formula gives you the floor. Your price has to cover variable expenses plus a share of fixed costs plus your desired profit.

Break-even point. The break-even point is where total revenue equals total cost. To calculate it, you need to know both your fixed costs and your variable cost per unit. The formula is: Break-Even Volume = Total Fixed Costs / (Price Per Unit minus Variable Cost Per Unit). Without the variable cost piece, you cannot find this number.

Contribution margin. Contribution margin = Revenue minus Total Variable Cost. This tells you how much each unit of production contributes to covering fixed costs and generating profit. It is one of the most watched numbers in business planning.

Scaling decisions. Before you ramp up production, you want to know what happens to your cost structure. If variable costs per unit stay flat, scaling is attractive. If they creep up, you have a problem to solve first.

Cost reduction efforts. When you break total variable cost into its parts, you can see where the largest costs sit. That is where you focus negotiation with suppliers, process improvement, or automation investment. Effective cost management at this level is what separates lean operators from those constantly under margin pressure.

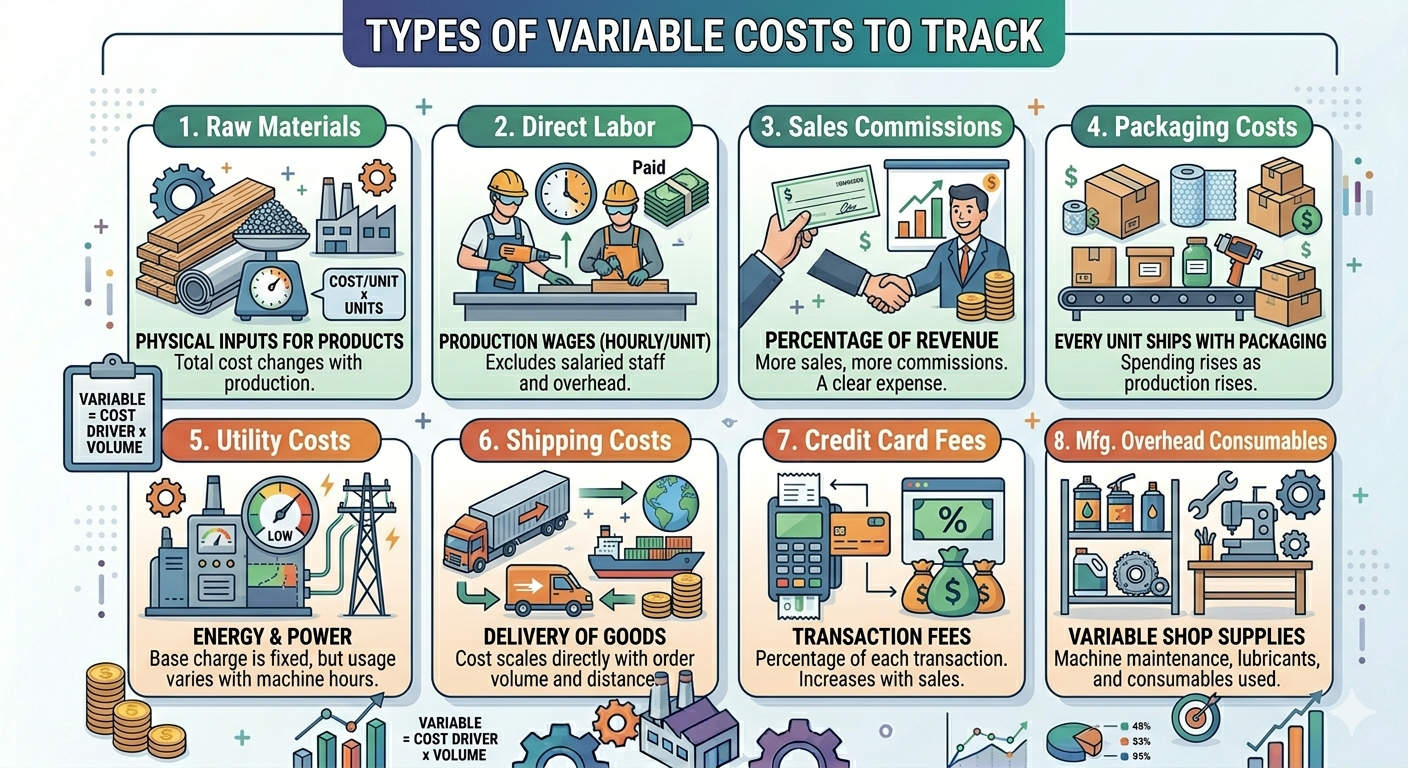

Types of Variable Costs to Track

Not all variable costs are obvious. Here is a more complete list of items that often belong in the total variable cost formula:

Raw materials. These are the physical inputs that become your product. The total cost of materials changes directly with units produced.

Direct labor. This includes production wages paid per hour or per unit. It does not include salaried managers or other overhead staff.

Sales commissions. These are paid as a percentage of revenue. More sales means more commissions. They are a clear variable expense.

Packaging costs. Every unit that ships needs packaging. As production output rises, so does spending here.

Utility costs. Some energy and utility spending is fixed (you pay a base charge no matter what), but a large portion is variable. Running machines longer burns more electricity.

Shipping costs. The cost to deliver goods often scales with volume.

Credit card processing fees. These are charged as a percentage of each transaction. They go up as sales go up.

Manufacturing overhead costs that vary with production. This includes things like machine maintenance supplies, lubricants, and other consumables.

Fixed Cost vs Variable Cost: The Key Difference

Understanding cost behavior starts with separating fixed from variable.

Fixed costs do not change with production volume. Rent, insurance, most employee salaries, loan payments, and software subscriptions are fixed. You owe them regardless of how many units you make or sell.

Variable costs do change with production volume. Raw materials, direct labor on a per-unit basis, packaging and shipping, and sales commissions all fall here.

Some costs are semi-variable costs, meaning they have both a fixed and a variable component. A phone plan with a base monthly fee plus per-minute charges is one example. In cost accounting, you split these into their fixed and variable parts before plugging them into your formulas.

Getting this separation right matters because it directly affects every calculation that follows, from cost per unit to break-even point to profit projections at different production levels.

Cost Structure and Business Strategy

Your cost structure, meaning the mix of fixed and variable costs in your business, affects how you compete and how much risk you carry.

A business with high fixed costs and low variable costs has high operating leverage. When revenue is high, profits are strong because variable expenses are small. But when revenue drops, the fixed cost burden remains, and losses can mount quickly.

A business with low fixed costs and high variable costs is more flexible. Costs fall naturally when production drops, which protects cash flow during slow periods. The trade-off is that margins may be tighter when volume is high.

Understanding your cost structure also affects decisions about outsourcing versus building in-house, hiring full-time staff versus contractors, and investing in automation. These choices all shift costs between the fixed and variable categories.

Using the Total Variable Cost Formula in Financial Planning

Good financial planning depends on accurate cost equations. When you model different production scenarios, you need to know which costs will scale and which will not.

For example, if you are building a budget for next year and you expect to grow units produced by 30 percent, you can apply that percentage directly to your total variable cost. Your fixed costs stay the same. This gives you a fast, reliable way to project total expenses at different activity levels.

It also helps with cash flow planning. Variable costs are often paid quickly, tied to purchase orders and payroll cycles. Knowing how much cash you need at different production levels helps you avoid shortfalls.

Financial modeling tools allow you to stress-test your cost assumptions across multiple scenarios, giving you a clearer picture of risk before you commit to major decisions.

Common Mistakes When Calculating Variable Costs

Misclassifying costs is the most common error. A salary paid to a production worker might feel variable, but if it is a fixed annual salary, it is a fixed cost. On the other hand, hourly production wages that depend on output are genuinely variable.

Forgetting indirect variable costs is another mistake. Packaging costs, credit card processing fees, and some utility costs are easy to miss when you are focused on raw materials and direct labor. They can add up quickly.

Using the wrong time period is also a problem. If your production levels vary seasonally, your variable cost per unit might shift throughout the year. Using an annual average hides these swings and can lead to pricing or planning errors.

Frequently Asked Questions

What is the total variable cost formula?

The total variable cost formula is: Total Variable Cost = Variable Cost Per Unit x Units Produced. It can also be calculated by adding together all the individual variable cost categories such as raw materials, direct labor, and packaging costs.

How is variable cost different from fixed cost?

Variable costs change with the level of production or sales activity. Fixed costs stay the same regardless of production volume. Rent and insurance are fixed. Raw materials and sales commissions are variable.

What is average variable cost?

Average variable cost is total variable cost divided by production output. It tells you the variable cost per unit at a given level of production. It is useful for comparing efficiency across different production levels.

Why does the total variable cost formula matter for break-even analysis?

The break-even point is calculated using both fixed costs and variable cost per unit. Without knowing the variable cost per unit, you cannot determine the contribution margin, and without the contribution margin, you cannot find break-even volume.

Can variable costs ever decrease as production increases?

Yes. Average variable cost often falls as production volume increases, due to bulk discounts on raw materials, improved worker efficiency, and better utilization of equipment. This is called economies of scale.

Are employee salaries a variable cost?

It depends. Hourly wages paid to production workers that fluctuate with output are variable. Fixed annual salaries paid to salaried staff are fixed costs, even if those employees work in production roles.

What is the difference between total cost and total variable cost?

Total cost includes both fixed and variable costs. Variable cost includes only the costs that change with production activity. Total Cost = Total Fixed Costs + Total Variable Cost.

Conclusion

Mastering the total variable cost formula is not just for accountants. It is one of the most practical skills any business owner or manager can develop. Additionally, it tells you what it really costs to produce your product or deliver your service. It feeds into pricing, break-even analysis, contribution margin, and cash flow planning. And when you know your numbers with this level of clarity, you make better decisions.

Make sure your accounting and bookkeeping processes are capturing every variable cost accurately — from raw materials to packaging to commissions, so your formula always reflects reality. And if your business needs deeper support with financial modeling, cost structure analysis, or building reliable projections, professional fractional CFO services can make a real difference. A fractional CFO brings the expertise to build these frameworks for your specific business, turning raw cost data into strategic insight. Explore how we can support your business with expert CFO services tailored to your goals.

{kind=link}