Scaling Smart: A Case Study in SaaS CFO Strategies for B2B Software

Client Overview

A fast-growing B2B SaaS company headquartered in Austin, Texas approached Oak Business Consultant at a critical inflection point. The company had grown from $400K to $2.1M in Annual Recurring Revenue (ARR) within three years, an impressive trajectory that had quietly outpaced its financial infrastructure.

The founding team was technically brilliant and commercially driven, but had no dedicated finance function. Revenue reporting was handled in spreadsheets. Churn was calculated inconsistently. Burn rate was tracked reactively. And with a Series A fundraise on the horizon, the company’s investor-ready documentation was nowhere near institutional standard.

They did not need a full-time CFO at $250,000 per year. They needed a SaaS CFO, one who understood subscription economics, SaaS metrics, and the specific financial narrative that growth-stage investors and lenders require.

Oak Business Consultant deployed its AI-Powered CFO Methodology across six strategic pillars, SaaS Metrics Architecture, Revenue Recognition, Cash Runway Forecasting, Investor Readiness, Unit Economics Optimization, and Tax & Equity Strategy, transforming the company’s financial operations within ninety days.

| Metric | Outcome |

| ARR Visibility | Real-time dashboard replacing manual spreadsheets |

| Churn Reporting | Standardized gross and net revenue churn — tracked monthly |

| Cash Runway | Extended from 5 months to 14 months through working capital optimization |

| Fundraising Readiness | Series A data room completed and investor-ready |

| CAC Payback Period | Reduced from 19 months to 11 months after pricing restructure |

| Tax Savings (Year 1) | R&D tax credits identified — exceeded CFO engagement cost |

Challenges to the Client

Three years of compounding growth had left the company’s financial infrastructure increasingly fragile. When Oak Business Consultant conducted its diagnostic assessment, six interconnected problems emerged — each invisible in isolation, but collectively threatening the company’s fundraising timeline and long-term sustainability.

No Reliable SaaS Metrics Framework:

ARR, MRR, churn, expansion revenue, and net revenue retention (NRR) were calculated differently across departments. The sales team, the CEO, and the bookkeeper were each working from different numbers — making board reporting inconsistent and investor conversations difficult to control.

Revenue Recognition Errors:

Multi-year contracts were being booked as lump-sum revenue at signing rather than recognized ratably over the contract term. This inflated short-term revenue figures and created a material accounting risk that would surface immediately under investor or auditor scrutiny.

Dangerously Short Cash Runway:

Without a rolling cash forecast, the team had no forward visibility into their burn rate. At the point of engagement, true runway was five months — far shorter than the founders believed. A fundraise under cash pressure is a fundraise conducted from a position of weakness.

Weak Unit Economics:

Customer Acquisition Cost (CAC) had never been calculated with precision across channels. Lifetime Value (LTV) was based on an assumed churn rate that significantly underestimated actual attrition. The LTV:CAC ratio presented to prospective investors did not reflect economic reality.

Investor Data Room Gaps:

The company had begun informal Series A conversations with three venture firms. All three had requested a standardized data room. Seven weeks later, it remained incomplete — missing a three-statement financial model, a cohort analysis, a capitalization table, and auditable revenue schedules.

No Equity or Tax Strategy:

The founding team held equity informally and had never completed an 83(b) election review. R&D tax credits, a significant benefit for qualifying SaaS companies, had never been claimed. The company was leaving tens of thousands of dollars on the table annually.

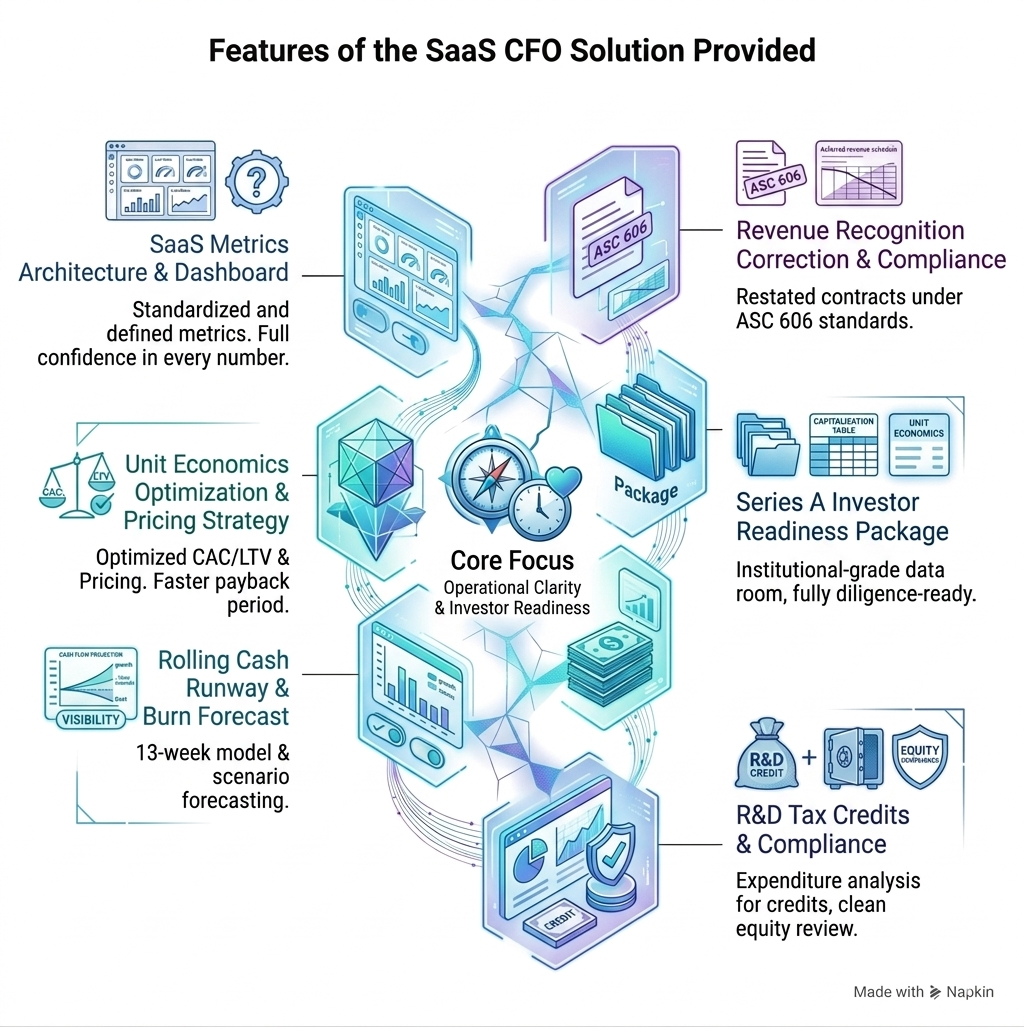

Features of the SaaS CFO Solution Provided

Oak Business Consultant deployed a purpose-built SaaS CFO engagement framework designed for subscription-model businesses at the growth stage. Every component was built with the dual mandate of operational clarity and investor readiness.

SaaS Metrics Architecture and Reporting Dashboard

A single source of truth for SaaS financial metrics was established across the organization. ARR, MRR, gross revenue churn, net revenue retention, expansion MRR, and contraction MRR were formally defined, calculated consistently, and connected to a live reporting dashboard. The board and investor decks were rebuilt around this standardized metrics framework, giving the founding team full confidence in every number they presented.

Revenue Recognition Correction and Compliance

A full revenue recognition audit was conducted across all active and historical contracts. Multi-year and annual prepaid contracts were restated under ASC 606 standards, with deferred revenue schedules built into the balance sheet. This correction eliminated the material accounting risk that had been quietly accumulating and produced financial statements that could withstand investor and auditor review without restatement.

Rolling Cash Runway and Burn Rate Forecasting

A thirteen-week cash flow model and a twelve-month rolling burn rate forecast were implemented with scenario-based sensitivity analysis. Three scenarios, base, downside, and growth acceleration, were modeled against hiring plans, contract close rates, and churn assumptions. The founding team could now see exactly how each operational decision affected their runway, enabling proactive capital management rather than reactive crisis response.

Series A Investor Readiness Package

A complete institutional-grade data room was built from the ground up, including a three-statement integrated financial model, a five-year SaaS revenue forecast with cohort-based assumptions, a full capitalization table, a unit economics summary, an ARR bridge analysis, and auditable revenue and deferred revenue schedules. The package was formatted to the expectations of institutional venture investors and growth equity firms, accelerating due diligence and establishing immediate credibility.

Unit Economics Optimization and Pricing Strategy

CAC was recalculated by channel with full attribution of sales and marketing costs. LTV was rebuilt using actual cohort-level churn data. The resulting LTV:CAC ratio, 2.3x at the point of engagement, was well below the 3x minimum institutional investors expect. A pricing restructure was modeled across three scenarios, and the recommended approach was implemented over sixty days, improving the CAC payback period from nineteen months to eleven months.

R&D Tax Credits, Equity Structuring, and Compliance

A qualifying expenditure analysis was conducted to identify R&D tax credits under Section 41 of the Internal Revenue Code. Credits worth more than the total cost of the engagement were identified in year one alone. Equity documentation was audited for all option holders, vesting schedules were formalized, and the cap table was restructured for clean Series A readiness. 83(b) election compliance was reviewed for all early equity recipients.

Outcome

Within ninety days, the Austin SaaS company moved from financial fragmentation to institutional-grade clarity — with a data room ready for Series A, a metrics framework that would survive investor due diligence, and a cash runway extended by nearly a year.

| Metric | Before | After (90 Days) |

| ARR Tracking | Inconsistent across departments | Standardized, real-time dashboard |

| Revenue Recognition | Lump-sum booking at signing | ASC 606 compliant, ratable recognition |

| Cash Runway | 5 months (undetected) | 14 months after optimization |

| Churn Calculation | Estimated, inconsistently applied | Gross and net churn tracked by cohort |

| LTV:CAC Ratio | 2.3x (unacceptable for Series A) | 4.1x after pricing restructure |

| CAC Payback Period | 19 months | 11 months |

| Investor Data Room | Incomplete, 7 weeks outstanding | Fully built, institutionally formatted |

| Cap Table | Informal, unaudited | Clean, Series A-ready |

| R&D Tax Credits | Never claimed | Identified and filed |

| Board Reporting | Ad-hoc, inconsistent | Monthly, standardized metrics package |

The total estimated value of financial leakage eliminated — spanning tax credits, pricing inefficiency, working capital optimization, and the avoided cost of a distressed fundraise — exceeded $280,000 in year-one impact.

What’s in It for You?

Whether you are approaching your Seed extension, your Series A, or simply trying to build a SaaS business that does not run on guesswork, financial infrastructure is not a back-office function — it is a competitive advantage. The challenges this Austin company faced are the rule, not the exception, among founder-led SaaS businesses in the $500K to $5M ARR range.

A dedicated SaaS CFO function changes the game at every level: with investors, with lenders, with the board, and with the operational decisions that determine whether a SaaS business scales efficiently or hemorrhages capital.

Does Your SaaS Business Have the Same Hidden Risks?

Run this quick self-diagnostic. If three or more of the following apply, your financial infrastructure needs professional attention before your next capital raise or growth decision:

- Your ARR and MRR figures are calculated differently by different people in the business

- You have never conducted a formal revenue recognition review under ASC 606

- You do not have a rolling cash runway forecast updated at least monthly

- Your LTV:CAC ratio has never been calculated with full channel-level attribution

- You have begun investor conversations without a complete, auditable data room

- Your churn rate is estimated rather than tracked by cohort

- You have never claimed R&D tax credits as a qualifying software business

- Your cap table has never been reviewed by a finance professional ahead of a funding round

How to Overcome These Challenges

To build a financially credible, investor-ready SaaS business, every founder approaching the growth stage needs to:

- Establish a standardized SaaS metrics framework so ARR, churn, NRR, and unit economics are calculated consistently and presented with confidence to any investor, board member, or acquirer.

- Implement a rolling cash runway model with scenario analysis that replaces reactive burn management with proactive capital planning — giving the founding team control over their fundraising timeline.

- Build an institutional-grade investor data room before conversations begin, not during them. Investors move faster — and at better terms — when due diligence is frictionless.

- Optimize unit economics proactively through pricing strategy, CAC attribution, and churn reduction — not retrospectively after a failed fundraise.

- Claim every tax advantage available to qualifying software businesses, including R&D tax credits, so non-dilutive capital is captured before every tax year closes.

Let’s Build Your Financial Foundation. At Oak Business Consultant, we specialize in SaaS CFO services for subscription-model businesses from Seed through Series B. Our AI-Powered CFO Methodology delivers institutional-grade financial clarity, investor-ready documentation, and strategic unit economics optimization — all at a fraction of the cost of a full-time CFO hire. Book a free SaaS Financial Diagnostic today and get a clear picture of where your financial infrastructure is limiting your growth.

Frequently Asked Questions

When does a SaaS company need a CFO?

Most SaaS companies benefit from dedicated CFO services once ARR reaches $500K or when a fundraise, board formation, or significant hiring plan is on the horizon. At this stage, financial decisions become too consequential and too complex to manage with bookkeeping software and spreadsheets alone.

What SaaS metrics does a fractional CFO track?

A SaaS CFO will establish and monitor ARR, MRR, gross revenue churn, net revenue retention (NRR), Customer Acquisition Cost (CAC), Lifetime Value (LTV), LTV:CAC ratio, CAC payback period, expansion MRR, contraction MRR, and monthly burn rate — among others. These metrics form the financial language of institutional investors and must be calculated consistently and accurately.

How does a SaaS CFO help with Series A fundraising?

A SaaS CFO builds the complete financial infrastructure required for institutional due diligence — including a three-statement financial model, cohort analysis, ARR bridge, cap table, deferred revenue schedules, and a standardized metrics dashboard. This preparation compresses the due diligence timeline, reduces investor uncertainty, and positions the company to negotiate from a position of financial confidence.

What is ASC 606 and why does it matter for SaaS companies?

ASC 606 is the revenue recognition standard that requires SaaS companies to recognize subscription revenue ratably over the contract term rather than at the point of billing. Failure to comply creates a material accounting risk that surfaces immediately under investor or auditor scrutiny, and can result in financial restatement — a serious credibility issue during any fundraise.

Conclusion

This engagement illustrates what becomes possible when a growth-stage SaaS company pairs commercial momentum with the financial infrastructure to support it. By deploying a SaaS CFO methodology built specifically for subscription-model businesses, Oak Business Consultant delivered standardized metrics, ASC 606-compliant revenue recognition, extended cash runway, institutional investor readiness, and optimized unit economics, all within ninety days.

The impact was not limited to cleaner spreadsheets. It changed how the founding team saw their own business, how they communicated with investors, and how they made decisions about pricing, hiring, and capital allocation. If your SaaS business is growing faster than its financial infrastructure, the cost of inaction compounds with every passing quarter.

Contact Oak Business Consultant to begin your complimentary SaaS Financial Diagnostic and take the first step toward investor confidence, operational clarity, and sustainable ARR growth.