How to Calculate Fixed and Variable Costs?

Calculating Fixed vs. Variable Costs: A Practical Approach

Understanding how to calculate fixed and variable costs is one of the most practical skills in business finance. Whether you run a small startup or manage a large operation, knowing where your money goes each month changes how you make decisions. This guide breaks it all down in plain terms.

What Are Fixed Costs?

Fixed costs are expenses that stay the same no matter how much you produce or sell. They do not change with your production volume or sales volume. You pay them every month whether you serve ten customers or ten thousand.

Common examples of fixed costs include:

- Rent and lease payments

- Insurance premiums

- Property tax

- Salaries for permanent staff

- Business loan repayments

- Equipment rental fees

- Software subscriptions

These are sometimes called fixed expenses or overhead costs. They show up on your income statement as a consistent line item. Even when your production output drops to zero, these costs remain.

Fixed costs matter because they set your baseline. You must cover them before you earn a single dollar of profit.

What Are Variable Costs?

Variable costs change in direct proportion to your business activity. As you produce more, they go up. As production slows, they fall. They move with your production process.

Common variable expenses include:

- Raw materials and direct materials

- Direct labor and labor costs

- Sales commissions

- Shipping supplies and packaging

- Food costs (for food businesses)

- Energy prices tied to production

- Raw material purchases

Variable costs are closely tied to your production units. If it costs you $5 in raw materials to make one product and you make 1,000 units, your total variable costs for materials are $5,000. Double production, and you double that cost.

Fixed vs. Variable: Why the Distinction Matters

When you know how to calculate fixed and variable costs separately, you can:

- Find your break-even point

- Set smarter prices using cost-plus pricing

- Understand your contribution margin

- Forecast cash flow more accurately

- Manage profit margins when sales fluctuate

- Make better decisions about scaling up or down

This separation is the foundation of managerial accounting. It feeds into your income statement, your cost of goods sold, and your cost of goods manufactured. Without it, cost management becomes guesswork.

How to Calculate Fixed Costs

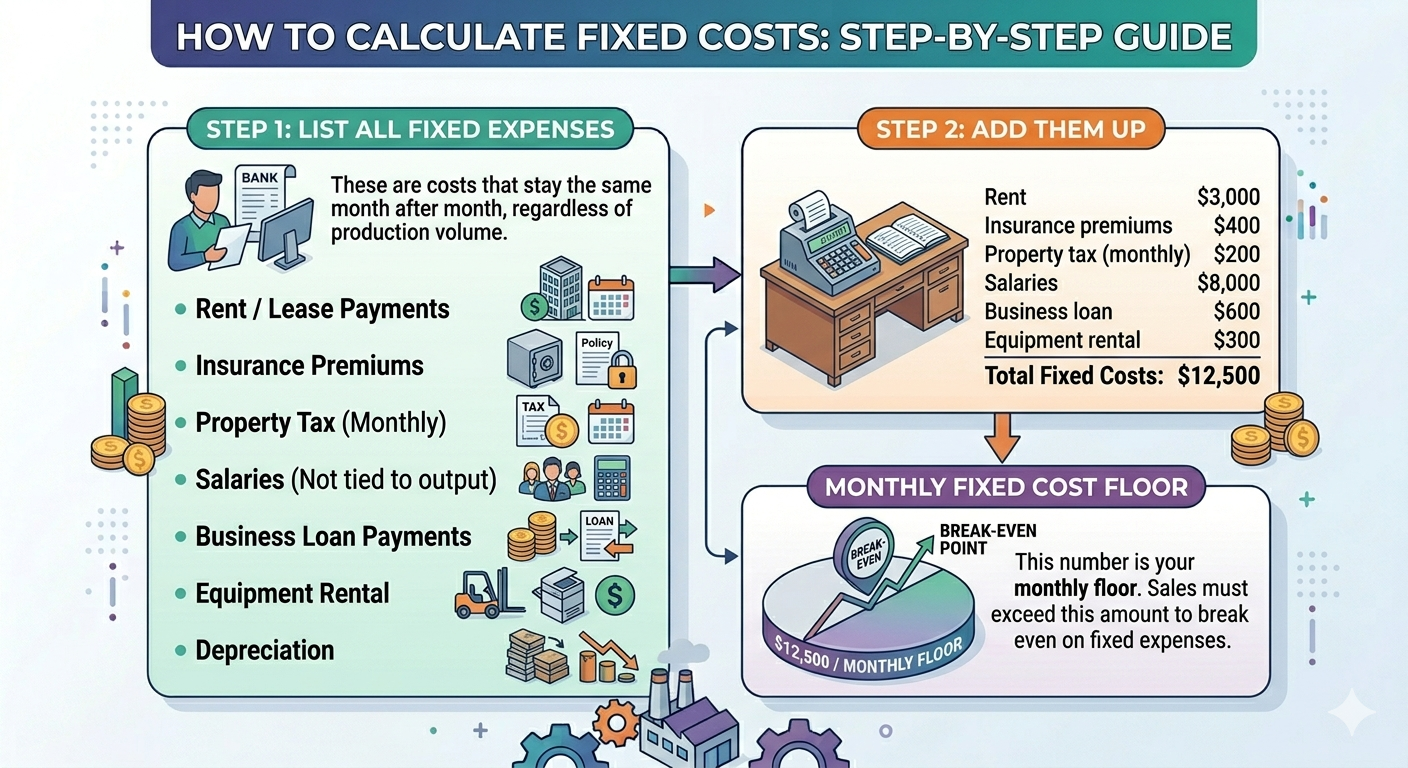

Step 1: List All Fixed Expenses

Go through your bank statements, accounting software, or ERP system. Write down every cost that stays the same month after month.

This typically includes:

- Monthly rent or lease and rent payments

- Insurance premiums

- Property tax (annual amount divided by 12)

- Salaries (not hourly wages tied to output)

- Business loan monthly payments

- Equipment rental

- Depreciation on owned equipment

Step 2: Add Them Up

Total fixed costs formula:

Total Fixed Costs = Sum of All Fixed Expenses in a Period

Example:

| Expense | Monthly Amount |

| Rent | $3,000 |

| Insurance premiums | $400 |

| Property tax (monthly) | $200 |

| Salaries | $8,000 |

| Business loan | $600 |

| Equipment rental | $300 |

| Total Fixed Costs | $12,500 |

This number becomes your monthly floor. Your business must generate at least this much in sales revenue just to break even on fixed expenses alone.

How to Calculate Variable Costs

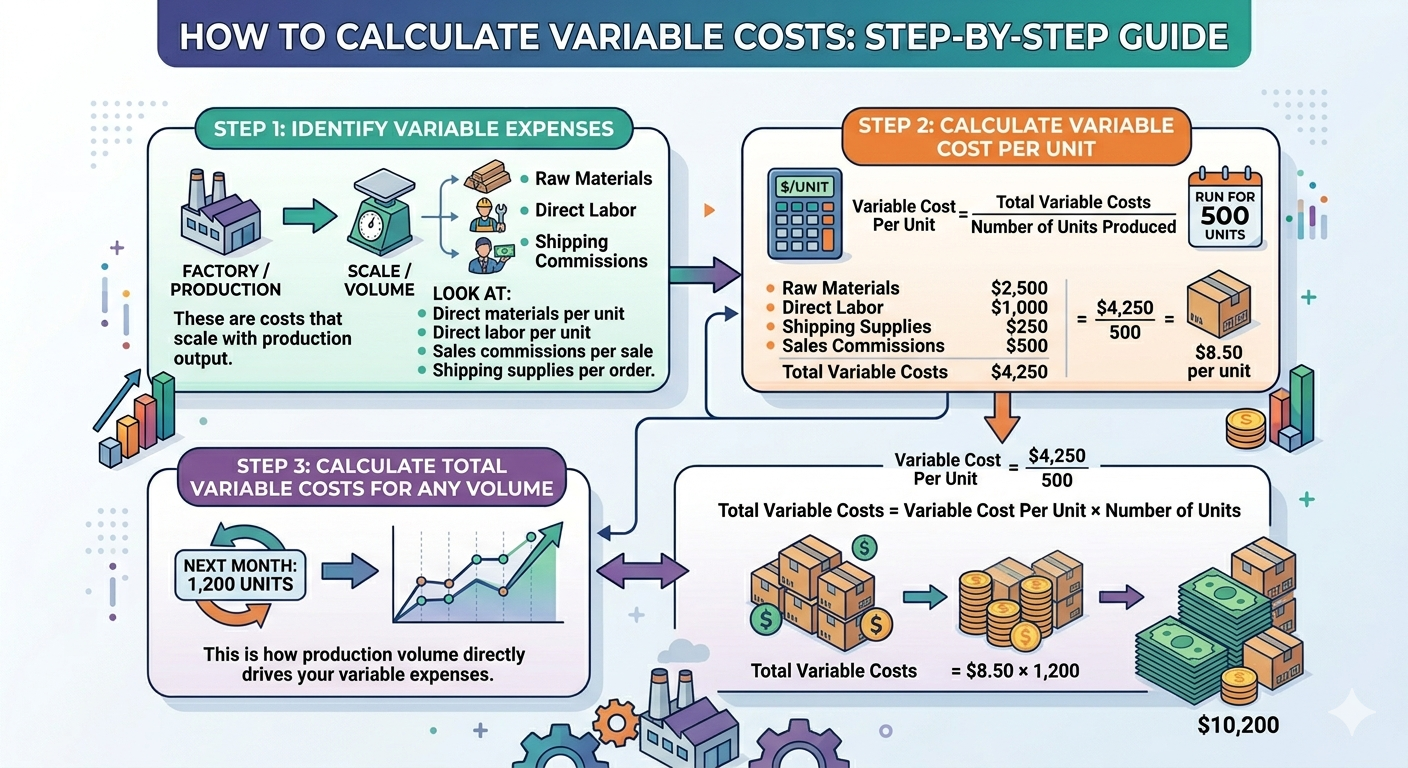

Step 1: Identify Variable Expenses

These are costs that appear in your production process and scale with output. Look at:

- Cost of direct materials per unit

- Direct labor per unit produced

- Sales commissions per sale

- Shipping supplies per order

- Any cost that rises when you produce or sell more

Step 2: Calculate Variable Cost Per Unit

Variable Cost Per Unit = Total Variable Costs / Number of Units Produced

Example: You produce 500 units. Your costs for that run are:

| Variable Expense | Amount |

| Raw materials | $2,500 |

| Direct labor | $1,000 |

| Shipping supplies | $250 |

| Sales commissions | $500 |

| Total Variable Costs | $4,250 |

Variable Cost Per Unit = $4,250 / 500 = $8.50 per unit

Step 3: Calculate Total Variable Costs for Any Volume

Total Variable Costs = Variable Cost Per Unit × Number of Units

If you plan to produce 1,200 units next month:

Total Variable Costs = $8.50 × 1,200 = $10,200

This is how production volume directly drives your variable expenses.

How to Calculate Total Cost

Once you have both figures, total cost is straightforward.

Total Cost = Total Fixed Costs + Total Variable Costs

Using the examples above, for 1,200 units:

Total Cost = $12,500 + $10,200 = $22,700

This is your complete production cost for that period. It feeds directly into your income statement and helps you calculate your cost of goods manufactured.

The Break-Even Point

The break-even point is where your total revenue equals your total cost. Below it, you lose money. Above it, you profit.

Break-Even Point (Units) = Total Fixed Costs / (Selling Price Per Unit – Variable Cost Per Unit)

The denominator here is your contribution margin per unit.

Example:

- Total fixed costs: $12,500

- Selling price per unit: $20

- Variable cost per unit: $8.50

- Contribution margin: $20 – $8.50 = $11.50

Break-Even Point = $12,500 / $11.50 = 1,087 units

You need to sell 1,087 units to cover all costs. Every unit sold above that contributes to profit.

This calculation is central to financial analysis, pricing strategy, and understanding your operating leverage.

Methods for Separating Mixed Costs

Some costs are semi-variable costs. They have a fixed base and a variable component. A utility bill is a classic example. You pay a base monthly fee regardless of usage, and then more on top depending on how much you consume.

These mixed costs need to be split before you can use them in your cost model formula. Two common methods exist.

The High-Low Method

This approach uses your highest and lowest activity levels to estimate the variable rate.

Variable Cost Rate = (Cost at High Activity – Cost at Low Activity) / (High Units – Low Units)

Then:

Fixed Component = Total Cost at Either Level – (Variable Rate × Units at That Level)

It is simple and fast but less accurate than statistical methods.

The Least-Squares Regression Method

This is a statistical technique that fits a line through all your cost data points. It uses your full cost data set to find the best estimate of both fixed and variable components. It is more precise than the high-low method, especially over longer periods with varied activity levels.

Most ERP systems and spreadsheet tools can run this automatically.

Semi-Variable Costs: A Closer Look

Semi-variable costs sit between the two categories. Examples include:

- Phone bills with a base plan plus usage charges

- Electricity with a standing charge plus per-unit energy prices

- Salesperson salaries with a base plus sales commissions

For accurate cost management, always decompose semi-variable costs into their fixed and variable parts before doing your full analysis.

Cost Separation in Practice

Here is a practical workflow for how to calculate fixed and variable costs in your business:

- Pull your expense data from your ERP system or accounting software

- List every operating expense from the past three to six months

- Categorize each as fixed, variable, or semi-variable

- Use the high-low method or least-squares regression method to split mixed costs

- Calculate your total fixed costs and total variable costs separately

- Run your break-even analysis

- Compare actual costs to your budget using variance analysis, including fixed overhead volume variance

This process is part of activity-based costing and supports broader costing methods like job order costing and process costing.

Using Cost Data for Business Decisions

Once you know how to calculate fixed and variable costs reliably, you unlock a range of strategic tools.

Pricing Decisions

Cost-plus pricing starts with your total cost per unit. Add your desired margin on top. If your total cost is $22.00 per unit and you want a 30% margin, you price at around $28.60.

Scaling Decisions

If your fixed costs are high and variable costs are low, you have high operating leverage. Profit grows fast when sales volume rises but falls sharply when it drops. Understanding this helps you decide whether to grow aggressively or stay lean.

Expense Management

Tracking variable expenses over time reveals patterns. If your direct materials cost is climbing, it may signal waste in your production process, supplier price hikes, or inefficiencies in inventory management.

Contribution Margin Analysis

Contribution margin tells you how much each sale contributes to covering fixed costs and then generating profit. Products with high contribution margins deserve more attention in your sales activity and marketing spend.

Common Mistakes to Avoid

Many businesses make errors when learning how to calculate fixed and variable costs. The most common ones include:

- Treating all labor as fixed. Direct labor tied directly to production output is variable. Only salaried staff with no link to production volume are fixed.

- Forgetting semi-variable costs. Ignoring the mixed nature of some expenses inflates your fixed cost total and throws off your break-even analysis.

- Using outdated cost data. Costs change. Raw material purchases, energy prices, and labor costs shift with the market. Refresh your cost data regularly.

- Skipping the income statement check. Always reconcile your cost breakdown against your income statement to make sure nothing is missed.

Fixed and Variable Costs in Different Industries

The split between fixed and variable costs looks different depending on the business type.

A manufacturing firm has high variable costs from raw materials, direct materials, and direct labour. Fixed costs include factory rent, insurance premiums, and equipment depreciation.

A software company has mostly fixed costs. Developer salaries, infrastructure, and property tax dominate. Variable costs are minimal since production volume for digital goods barely changes per unit.

A retail business has a mix. Rent and insurance premiums are fixed. Inventory, shipping supplies, and sales commissions vary with sales volume.

A restaurant deals with high variable costs through food costs and direct labor. Fixed costs include rent, insurance, and management salaries.

Understanding the cost structure of your specific industry shapes how you approach pricing, staffing, and growth planning.

Tracking Tools That Help

To stay on top of how to calculate fixed and variable costs in real time, the right tools matter.

ERP systems automatically categorize transactions. They help you track production costs, inventory levels, and labor costs without manual data entry.

Accounting software can generate cost reports that separate fixed expenses from variable expenses. These feed into your income statement and help with financial analysis.

Activity-based costing software assigns costs to specific activities and products, giving you more granular insight than traditional costing methods.

Spreadsheets with regression formulas work well for smaller businesses using the least-squares regression method to separate mixed costs.

Mileage tracking apps help if your variable expenses include employee-owned fleet or company-owned fleet costs that change with miles driven.

Frequently Asked Questions

What is the difference between fixed costs and variable costs?

Fixed costs stay the same regardless of how much you produce or sell. Variable costs change in direct proportion to your production volume or sales activity. Rent is fixed. Raw materials are variable.

How do I calculate total variable costs?

Multiply your variable cost per unit by the number of units produced or sold. If each unit costs $8.50 to produce and you make 1,200 units, your total variable costs are $10,200.

What are examples of fixed expenses for a small business?

Common fixed expenses include rent, insurance premiums, property tax, business loan repayments, equipment rental, and salaried staff wages.

What is a semi-variable cost?

A semi-variable cost has both a fixed base and a variable component that changes with activity level. Utility bills and phone plans are typical examples.

How does the break-even point relate to fixed and variable costs?

The break-even point is where total revenue equals total cost. It depends on your total fixed costs and your contribution margin, which is the difference between your selling price and variable cost per unit.

Why is it important to separate costs for the income statement?

Separating fixed and variable costs on your income statement gives you cleaner data on gross profit margins, contribution margin, and operating leverage. This helps with better pricing, cost management, and financial analysis.

What role do fixed costs play in operating leverage?

Businesses with high fixed costs and low variable costs have high operating leverage. Their profits grow faster when sales rise but also fall sharply when sales decline.

Can variable costs ever become fixed?

In some situations, yes. For example, management bonuses tied to profits are variable, but a committed minimum bonus becomes a fixed obligation. This is why reviewing cost classification annually matters.

Conclusion

Knowing how to calculate fixed and variable costs is not just an accounting exercise. It is a decision-making tool that touches pricing, hiring, investment, and growth strategy. When you understand what costs are fixed and what costs move with your production output, you see your business more clearly.

If you want to take this further with professional financial oversight, working with an experienced CFO can transform how you use cost data. Oak Business Consultant offers fractional CFO services designed to help businesses build tighter financial controls, sharper pricing strategies, and more confident forecasting. Reach out to explore how their CFO services can support your business goals.