A Case Study in Real Estate CFO Strategies for Multi-Entity Portfolios

Client Overview

A Houston-based real estate investment firm managing twelve active assets across eight separate LLCs approached Oak Business Consultant in urgent need of financial clarity. After seven years of organic portfolio growth, the firm’s financial infrastructure had failed to keep pace with its expanding operations.

Each property sat in its own legal entity, a sound liability strategy that had quietly created an operational nightmare. With no consolidated reporting, no forward-looking cash flow visibility, and two refinancing applications stalled with lenders, the client needed more than a bookkeeper. They needed a real estate CFO.

Oak Business Consultant deployed its AI-Powered CFO Methodology across six strategic pillars: Consolidation, Forecasting, Reporting, Lender Packaging, Investor Communication, and Tax Optimization, delivering a complete financial transformation within ninety days.

| Metric | Outcome |

| Portfolio Consolidation | 8 LLCs unified into a single dashboard |

| Cash Flow Forecasting | 12-month rolling forecast with AI anomaly detection |

| Refinancing Status | Both stalled applications closed at favorable terms |

| Investor Reporting | Quarterly, consistent, professional-grade |

| Tax Savings (Year 1) | Exceeded total CFO engagement cost |

| Time Saved | 1 full day/month eliminated from manual consolidation |

Challenges to the Client

The firm’s seven years of active growth had been financially unmanaged at the portfolio level. By the time Oak Business Consultant engaged, the following critical pain points had taken root:

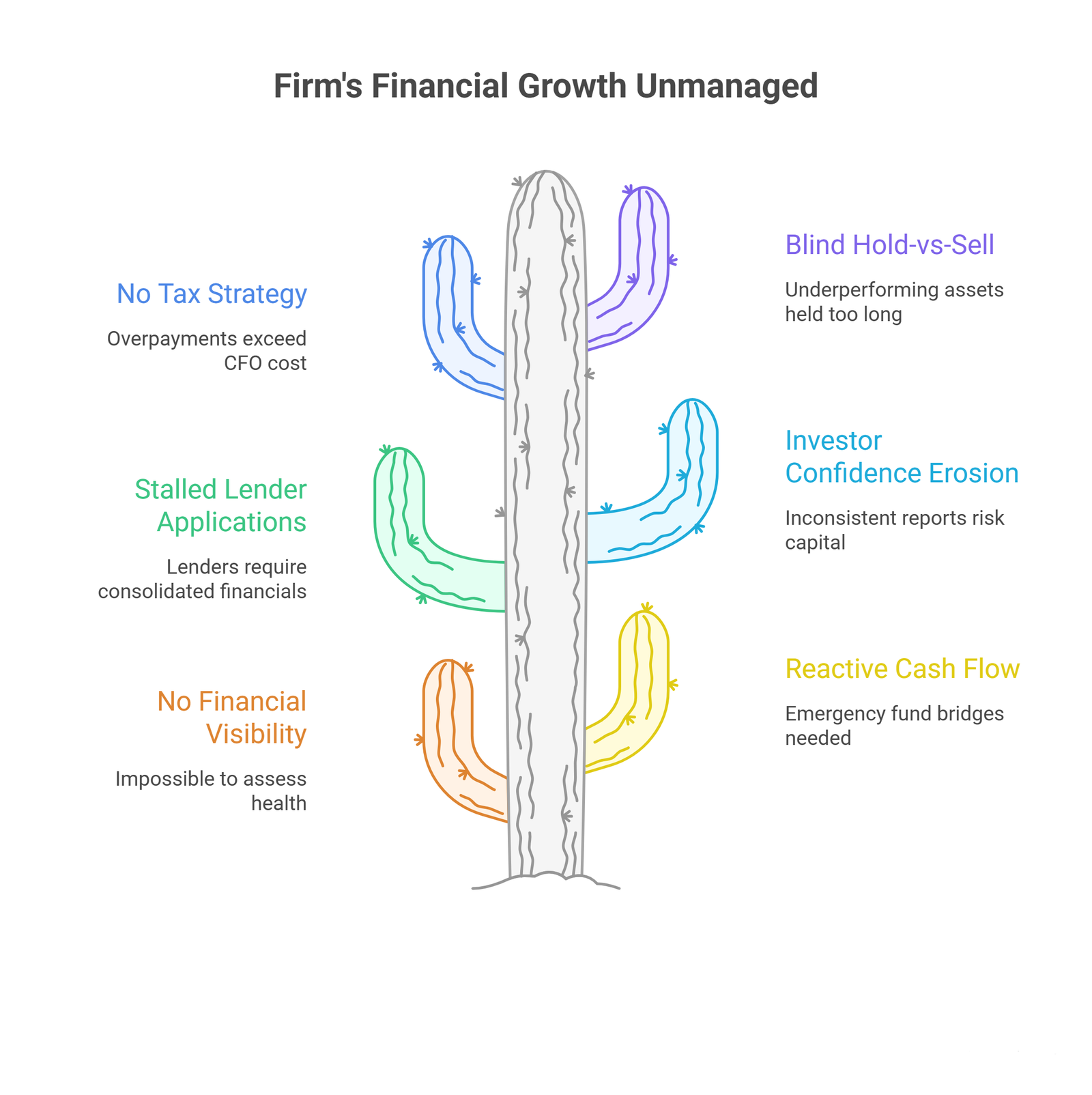

- No Consolidated Financial Visibility: Eight separate QuickBooks Online files, each with a slightly different chart of accounts, made it impossible to assess portfolio health at a glance. Decision-making was based on incomplete, entity-level data.

- Reactive Cash Flow Management: With no forward-looking forecast, the firm had resorted to two emergency personal fund bridges in a single twelve-month period. Capital was consistently tied up, and promising deals were missed.

- Stalled Lender Applications: Two refinancing applications sat unresolved for months. Lenders required consolidated financials, DSCR calculations, and rent rolls the client could not produce quickly or consistently, putting favorable interest terms at risk.

- Investor Confidence Erosion: The same investor received three inconsistently formatted reports within one reporting cycle. Without a standardized communication cadence, follow-on capital was increasingly at risk.

- No Proactive Tax Strategy: Annual tax filings were completed without any strategic planning. Overpayments were estimated to exceed twice the annual cost of a full-time CFO engagement, a leak that had gone undetected for years.

- Blind Hold-vs-Sell Decisions: Without property-level NOI tracking, underperforming assets were held far longer than value justified. There was no data-driven framework for identifying which properties to exit and when.

Features of the Real Estate CFO Solution Provided

Oak Business Consultant deployed its AI-Powered CFO Methodology, a framework combining fractional real estate CFO expertise with AI-powered analytics and automation, tailored specifically to the complexities of multi-entity real estate portfolios.

Unified Multi-Entity Consolidation

A standardized chart of accounts was implemented across all eight LLCs and integrated into a cloud-based general ledger. Property management data feeds were connected to a single reporting environment, eliminating the one-day-per-month manual consolidation process entirely. For the first time, the client could view their entire portfolio, P&L, balance sheet, and cash flow, in a single dashboard.

12-Month Rolling Cash Flow Forecast

A forward-looking cash flow model was built with AI-powered anomaly detection that flags potential shortfalls thirty to sixty days before they materialize. This replaced a reactive, crisis-driven approach to capital management with a proactive planning discipline that is central to any effective real estate CFO engagement.

Lender-Ready Financial Reporting

A lender compliance dashboard was built featuring real-time DSCR calculations, rent rolls, trailing twelve-month (TTM) income summaries, and debt yield ratios, all formatted to institutional lender specifications. Both previously stalled refinancing applications were closed within the ninety-day engagement window.

Standardized Investor Communication

A professional quarterly reporting template was implemented with consistent metrics, transparent methodology, and delivery on a fixed schedule. The upgraded investor communication framework immediately restored confidence and created the conditions for follow-on capital commitments.

Property-Level NOI Tracking and Hold-vs-Sell Analysis

Property-level net operating income (NOI) was tracked and trended for every asset. A data-driven hold-versus-sell decision matrix was introduced, giving the client a clear, evidence-based framework for capital redeployment. Underperforming assets that had previously been invisible were identified, exited, and proceeds redeployed into higher-yield positions.

Proactive Tax Optimization

Reactive annual filing was replaced with a year-round tax strategy. Cost segregation studies were commissioned on two qualifying properties, dramatically accelerating depreciation schedules. Full 1031 exchange documentation was prepared for an upcoming disposition. Real estate professional status compliance was completed and documented to IRS standards, unlocking passive loss deductions previously unavailable to the client.

Outcome

Within ninety days, the Houston firm moved from financial chaos to institutional-grade clarity.

| Metric | Before | After (90 Days) |

| Financial Visibility | 8 separate QuickBooks files | Single consolidated dashboard |

| Reporting Time | 1 full day/month, manual | Real-time, automated |

| Cash Flow Forecast | None — fully reactive | 12-month AI-powered rolling forecast |

| Lender Packages | Incomplete and inconsistent | Lender-ready, real-time DSCR |

| Refinancing Status | 2 applications stalled | Both closed at favorable terms |

| Investor Reporting | Ad-hoc, inconsistent | Quarterly, professional-grade |

| Property-Level NOI | Not tracked | Tracked per asset, trended |

| Tax Strategy | Annual compliance filing only | Cost seg, 1031, professional status |

| Underperforming Assets | Invisible | Identified, sold, and redeployed |

The total estimated hidden cost of the firm’s previous financial infrastructure — spanning manual labor, emergency fund bridges, delayed refinancing, tax overpayments, and underperforming asset drag, exceeded $193,000 annually. The Oak engagement eliminated the majority of these leaks within a single quarter.

What’s in It for You?

Whether you manage five properties or fifty, financial infrastructure that lags behind your portfolio is not a minor inconvenience, it is an active threat to your returns, your lender relationships, and your investor confidence. The challenges this Houston firm faced are not unique. They are the predictable consequence of portfolio growth without a dedicated real estate CFO function.

Does Your Portfolio Have the Same Hidden Leaks?

Run this quick self-diagnostic. If three or more of the following apply to your operation, your financial infrastructure requires professional attention:

- It takes more than two hours to produce a portfolio-wide P&L

- You have been surprised by a cash shortfall in the past twelve months

- A lender has requested financial data you could not produce quickly

- Your investors receive inconsistent or late updates

- You do not know the exact NOI of each individual property

- Your tax strategy is limited to annual compliance filing

- You are unsure which assets to hold and which to sell

- Intercompany transfers between your LLCs are tracked inconsistently

How to Overcome These Challenges

To build a financially resilient, lender-ready real estate portfolio, every multi-entity investor needs to:

- Engage a real estate CFO — fractional or virtual — who understands multi-entity consolidation, property-level reporting, and lender communication at the institutional level.

- Implement a rolling cash flow forecast with proactive anomaly detection, eliminating reactive capital management and emergency fund bridging.

- Standardize investor reporting with consistent metrics, fixed delivery schedules, and professional-grade formatting to protect existing capital relationships and attract new ones.

- Activate proactive tax strategies — cost segregation, 1031 exchanges, and real estate professional status — before the tax year closes, not after.

- Build lender-ready financial packages that travel with your portfolio at all times, so refinancing and acquisition financing move at the speed of opportunity.

Let’s Build Your Financial Foundation. At Oak Business Consultant, we specialize in providing real estate CFO services to multi-entity investors who have outgrown basic bookkeeping and need strategic financial leadership. With our AI-Powered CFO Methodology, we deliver institutional-grade clarity at a fraction of the cost of a full-time hire. Book a free Portfolio Diagnostic today and discover exactly where your financial infrastructure is leaking value.

Frequently Asked Questions

How is a real estate CFO different from a property accountant?

A property accountant handles historical bookkeeping and tax compliance. A real estate CFO interprets that data, builds forward-looking forecasts, advises on capital structure, interfaces with lenders and investors, and drives strategic decisions. The two roles are complementary but serve fundamentally different purposes.

What is multi-entity portfolio consolidation?

Multi-entity consolidation is the process of unifying the financial records of multiple LLCs into a single, standardized reporting environment. For real estate investors, this typically means aligning charts of accounts, integrating property management data feeds, and producing a consolidated P&L, balance sheet, and cash flow statement across the entire portfolio.

How much does a fractional real estate CFO cost?

Fractional real estate CFO engagements vary based on portfolio complexity. However, as this case study demonstrates, the tax savings, refinancing outcomes, and operational efficiencies generated typically exceed the total cost of the engagement — often within the first year.

What is a DSCR calculation and why do lenders require it?

Debt Service Coverage Ratio (DSCR) measures a property’s net operating income relative to its debt obligations. Lenders use it to assess whether a property generates sufficient income to service its debt. A real estate CFO builds real-time DSCR dashboards that keep lender packages current and refinancing applications moving.

Can a real estate CFO help with cost segregation and 1031 exchanges?

Yes. Proactive tax strategy — including cost segregation studies, 1031 exchange structuring, and real estate professional status compliance — is a core function of a strategic real estate CFO engagement. These tools can generate tax savings that alone justify the cost of the engagement.

Conclusion

This engagement demonstrates what becomes possible when a scaling real estate investor pairs portfolio ambition with the right financial infrastructure. By deploying a real estate CFO methodology purpose-built for multi-entity portfolios, Oak Business Consultant delivered consolidated visibility, lender-ready reporting, proactive tax savings, and investor-grade communication — all within ninety days.

The result was not just operational efficiency. It was a fundamental shift in how the client could see, manage, and grow their portfolio. If your real estate business has outgrown its financial infrastructure, the cost of inaction is almost certainly larger than the cost of a solution.

Contact Oak Business Consultant to begin your complimentary Portfolio Diagnostic and take the first step toward financial clarity, lender confidence, and sustainable portfolio growth.